Fact-checked by the Smart Insurance 101 editorial team

The Verdict

An occurrence policy is usually the better choice for small businesses buying commercial general liability, because it covers incidents during the policy period with no future tail purchase required. A claims-made policy makes sense for professional liability or E&O coverage, where occurrence forms are rarely available. The critical threshold: if tail coverage costs 100–200% of your annual premium, claims-made savings evaporate fast unless you qualify for a free retirement tail.

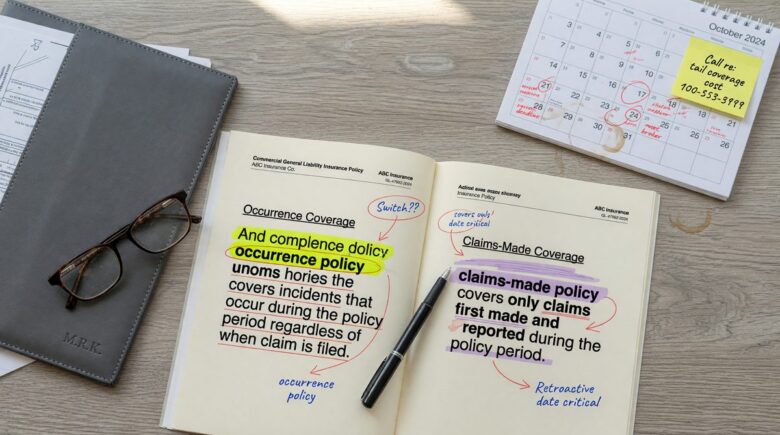

The single factor that swings the occurrence vs claims-made policy decision is not price, it is the policy trigger. Occurrence policies respond to incidents that happen during the policy period, regardless of when the lawsuit is filed. Claims-made policies respond only to claims reported while the policy is active. That timing difference can mean the difference between full coverage and a complete gap, especially for small businesses where lawsuits sometimes arrive years after the triggering event. As the Insurance Information Institute explains, occurrence policies cover incidents during the policy period regardless of when the claim is filed, while claims-made policies cover only claims made during the policy period itself.

This choice matters more now because litigation timelines are stretching and liability lawsuits are quietly getting more expensive. A policy decision made at startup can haunt a business owner at retirement if the wrong form was chosen.

| Factor | Reasons to Choose Occurrence | Reasons to Choose Claims-Made |

|---|---|---|

| Coverage trigger | Incident during policy period; claim can come years later | Lower if you plan to buy tail or switch carriers soon |

| Long-term cost | Higher upfront premium, but no tail purchase ever needed | Lower initial premium; tail can cost 100–200% of annual premium at exit |

| Business exit protection | Coverage stays in force after policy ends for prior incidents | Coverage ends at cancellation unless tail is purchased |

| Availability for GL | Standard form; most insurers offer it on ISO CG 00 01 | Less common for general liability; sometimes unavailable |

| Availability for E&O/Professional | Rare; most carriers do not offer occurrence for professional liability | Standard form for E&O, D&O, and cyber liability lines |

| Step-rating risk | None; premium reflects full exposure from day one | Premiums rise over first 4–5 years before stabilizing near occurrence pricing |

| Switching carriers | No retroactive date or nose coverage needed | Requires matching retroactive dates or purchasing nose coverage to avoid gaps |

| Retirement or sale | No action needed; prior incidents remain covered | Must purchase tail or negotiate extended reporting period before closing |

Key Takeaways

- Your coverage is commercial general liability (CGL), occurrence is almost always the right default, and the ISO CG 00 01 form is the standard.

- You are buying professional liability, E&O, D&O, or cyber, claims-made is likely your only option, so budgeting for tail coverage is essential from day one.

- You plan to close, sell, or retire within 5 years, occurrence eliminates the tail purchase obligation that can equal 100–200% of your final annual premium.

- Your insurer offers a free tail for death, disability, or retirement, that benefit can tip the math in favor of claims-made even for longer-tenured professionals.

- Your state’s statute of limitations for your industry runs longer than 3 years, the longer the window, the more expensive it becomes to go without tail on a claims-made form.

- You are switching carriers or policy forms, you need either a matching retroactive date from the new carrier or nose coverage purchased from the old one before the transition is complete.

- Your annual premium on a mature claims-made policy exceeds $5,000, at that level, tail cost becomes a material exit liability worth comparing to an occurrence policy’s lifetime premium.

Why the Policy Trigger Changes Everything

The trigger is the single most important concept in this comparison. An occurrence policy is triggered when the injury or damage happens, full stop. A claims-made policy is triggered only when the claim is reported, and only if the policy is still active at that moment.

For small businesses, this distinction hits hardest in three scenarios: slip-and-fall injuries where the plaintiff delays filing, product liability cases where harm appears months after purchase, and professional services disputes where clients wait years before suing. Under an occurrence form, none of that delay creates a coverage problem. Under a claims-made form, a policy that lapsed six months ago provides no protection at all, even if the incident occurred while it was active.

The New York State Office of General Services defines occurrence policies as covering claims occurring during the policy period irrespective of when the claim is made, and explicitly contrasts them with claims-made policies, which cover only claims reported during the policy period. That is not legalese, it is the real-world gap that catches business owners off guard. For a deeper look at why liability costs are rising alongside these timing risks, understanding why small businesses need liability insurance is a useful starting point.

Claims-Made Cost Savings Are Real, Until They Are Not

Claims-made policies start cheaper. That is not a myth. In the early years of a new claims-made policy, premiums can run roughly 35% or more below the equivalent occurrence premium, because the insurer’s exposure is limited to claims filed against a policy with a short history. That gap narrows as the policy matures and step-rating kicks in.

Step-rating is the mechanism most brokers underexplain. Over the first four to five years of a claims-made policy, the insurer raises the premium each year as the “mature” rate is approached. By year five, the premium typically levels out near, and sometimes above, what an occurrence policy would have cost all along. The initial savings are real but temporary.

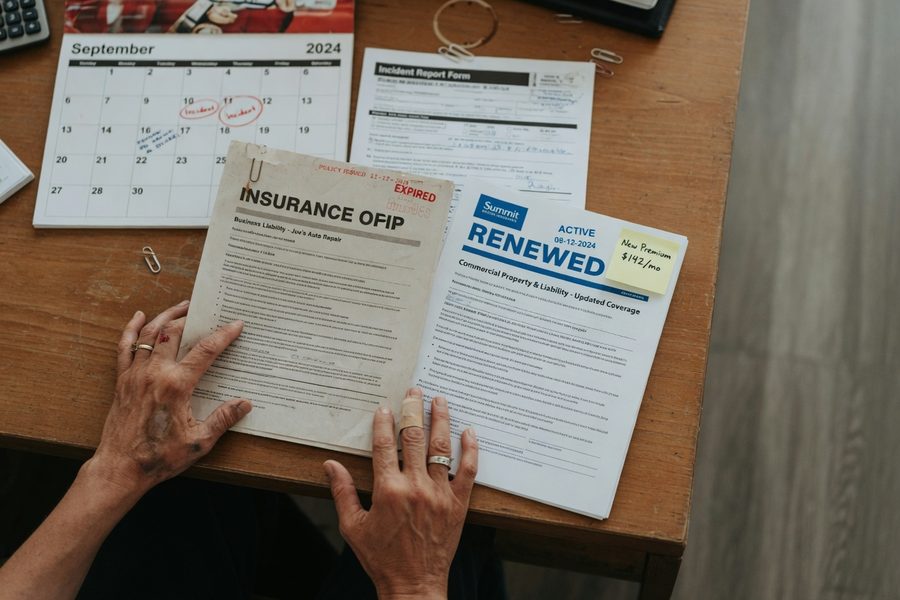

The exit cost is where the math turns ugly. When a business owner cancels a claims-made policy without purchasing tail coverage, all prior incidents become uninsured the moment a claim arrives. Tail coverage, formally called an Extended Reporting Period, or ERP, typically costs 100% to 200% of the final annual premium as a one-time payment. A business paying $8,000 per year for a mature professional liability policy could face a $16,000 tail bill at retirement. An occurrence policy holder faces a $0 tail bill. That comparison belongs in every small business financial plan. If you are already paying attention to rising insurance costs, the trends described in why insurance premiums are exploding add useful context to the step-rating reality.

One honest exception: many professional liability insurers offer a free tail for death, disability, or retirement after a minimum number of policy years. If your carrier includes that benefit and you plan to retire rather than sell, the claims-made cost equation looks much more favorable.

Which Policy Form Applies to Which Coverage Line?

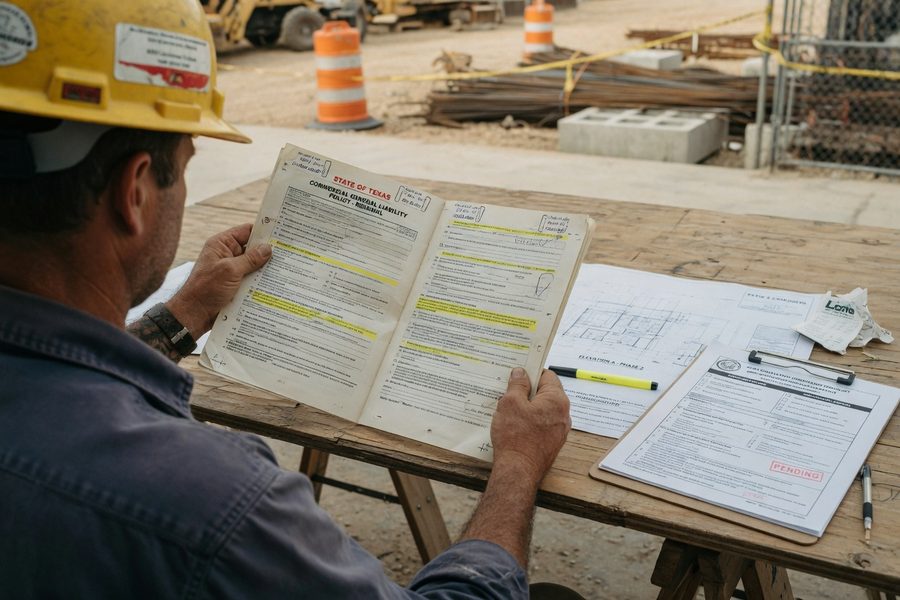

For commercial general liability, occurrence is the standard. Most state and federal contracting agencies require it explicitly. The Louisiana Division of Administration requires commercial general liability coverage on an occurrence basis using the ISO CG 00 01 form and states that claims-made forms are unacceptable in contract insurance requirements. Louisiana is not unique, the Washington State Department of Enterprise Services similarly recommends occurrence-basis CGL in its minimum insurance requirements for contracts. If your business holds government or municipal contracts, an occurrence CGL policy may not just be preferable, it may be mandatory.

Professional liability, E&O, D&O, and cyber liability are a different story. Occurrence forms are rare to nonexistent for these lines. Insurers have avoided offering occurrence-based professional liability because the long-tail exposure, claims filed a decade after a negligent act, makes pricing nearly impossible. If you are an architect, accountant, consultant, or technology firm, claims-made is almost certainly your only option. The practical implication: budget for tail coverage from the start, and ask your broker about free tail provisions before you bind the policy.

Cyber liability deserves a separate note. Cyber policies are almost universally written on a claims-made basis, and the retroactive date is critical. A retroactive date that does not reach back far enough can leave a business uninsured for a breach that started months before the current policy period. That is a gap worth negotiating with your insurer before renewal.

Who Should and Who Should Not

Good candidates for an occurrence policy

Occurrence coverage fits best when the business faces physical liability risks and has a long or uncertain operating horizon.

- A retail shop, restaurant, or contractor with genuine slip-and-fall or property damage exposure, incidents happen fast and claims sometimes follow years later.

- A business owner within 5–10 years of a planned sale or retirement who cannot predict their exit cost or does not want the tail obligation.

- Any business required by contract, municipal, state, or federal, to carry occurrence-basis commercial general liability on the ISO CG 00 01 form.

- A startup with tight cash flow that can absorb a higher upfront premium in exchange for zero future tail liability, particularly if the business is expected to run for many years.

Who should skip occurrence and accept claims-made

Claims-made is the practical reality for professional service providers and any business buying specialized liability lines.

- A licensed professional, attorney, accountant, architect, engineer, or consultant, where professional liability occurrence forms simply are not offered by the market.

- A technology company or SaaS business buying cyber liability or tech E&O, where claims-made is the only structure available.

- A business owner whose carrier offers a free extended reporting period for retirement, death, or disability, making the claims-made total cost competitive over a full career.

- A newer business with very limited cash flow that genuinely cannot afford occurrence premiums in year one, provided the owner understands step-rating and builds in future tail reserves.

Frequently Asked Questions

What is the main difference between an occurrence and a claims-made policy?

The trigger. An occurrence policy covers incidents that happen during the policy period, no matter when the claim is filed. A claims-made policy covers only claims reported while the policy is active. If you cancel a claims-made policy without tail coverage and a lawsuit arrives the following year, you have no protection, even if the underlying incident happened when the policy was in force.

Is occurrence or claims-made cheaper for a small business?

Claims-made is cheaper early on, often by 35% or more in the first year. That gap closes over 4–5 years as premiums step-rate toward maturity. Over a full business lifetime, occurrence is frequently the lower total cost when you factor in the tail purchase that claims-made requires at exit. For more on how different business insurance costs compare, this overview of commercial insurance breaks down the major policy types.

Do I need tail coverage if I cancel a claims-made policy?

Yes, if you have any past incidents that could still generate a lawsuit. Without tail coverage, an Extended Reporting Period, a claims-made policy provides zero protection the moment it lapses. Tail coverage typically costs 100–200% of the final annual premium as a one-time charge. Some professional liability insurers offer a free tail for retirement or disability; ask your broker before you bind any claims-made policy.

Can I switch from a claims-made policy to an occurrence policy without creating a gap?

You can, but it requires deliberate action. When moving from claims-made to occurrence, you either need nose coverage purchased from your old carrier, which extends the claims-made reporting period forward, or you need the new occurrence carrier to accept a retroactive date that reaches back to your original claims-made policy start date. Missing this step leaves all prior acts uninsured. Talk to your broker before initiating any carrier change; the transition mechanics are where most coverage gaps occur.

Which form do government contracts usually require?

Occurrence, almost universally. State and federal agencies routinely specify occurrence-basis commercial general liability, often requiring the ISO CG 00 01 form explicitly, and reject claims-made forms as unacceptable for contract compliance. If your business works with government clients, verify the insurance requirements in the contract before renewal season, a claims-made CGL policy could disqualify you from work you are already doing. The U.S. Department of Housing and Urban Development’s guidance on professional liability outlines exactly how both forms function in a government contracting context.

Sources

- Insurance Information Institute, Types of Commercial Insurance Policies

- U.S. Department of Housing and Urban Development, Professional Liability Insurance Requirements

- Louisiana Division of Administration, Insurance and Indemnification Language in Contracts

- New York State Office of General Services, Insurance Requirements in Contracts

- Washington State Department of Enterprise Services, Insurance Requirements in Contracts Manual