Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

Insurance coverage gaps are exclusions, sublimits, and policy mismatches that leave policyholders with denied claims or partial payouts. The most common surprises involve flood damage, sewer backup, underinsured auto liability, and out-of-network medical bills., home replacement costs have risen 20–40% since 2020, meaning millions of existing policies are already underinsured before any claim occurs.

Insurance coverage gaps are the specific holes in your policy where the coverage you assumed you had simply does not exist. Most policyholders discover these gaps at the worst possible moment: after a flood, a serious accident, a cancer diagnosis, or a house fire. According to KFF’s 2024 population data, 26.7 million Americans under age 65 had no health coverage at all, and millions more carry policies with exclusions that function like no coverage in a crisis.

What follows is a direct look at where real policyholders got blindsided, why standard policies are built with these holes, and which gaps are most likely to affect you right now. Understanding these failure points before a claim is the only time it actually does any good.

Key Takeaways

- Home replacement costs have risen 20–40% since 2020 due to construction inflation, meaning policies renewed without a coverage adjustment are likely underinsured today (Insurance Information Institute, 2025).

- 21% of U.S. working-age adults with private insurance reported that they or a family member experienced a denial of coverage for doctor-recommended care in the past year, according to the Commonwealth Fund’s 2025 Affordability Survey.

- Flood damage from ground seepage or sewer backup is excluded in more than 95% of standard HO-3 homeowners policies, requiring a separate NFIP or private flood policy.

- An estimated 1.4 million people fall into the Medicaid coverage gap in states that have not expanded Medicaid, earning too much for Medicaid but too little for Marketplace tax credits (KFF via healthinsurance.org, 2025).

- State minimum auto liability limits in many states remain at $25,000 per person / $50,000 per accident, far below average jury awards exceeding $100,000 for serious injury cases.

In This Guide

- Real Policyholder Stories: When the Claim Revealed the Gap

- Why Standard Policies Leave These Holes by Design

- Homeowners Insurance Surprises That Hit After the Storm

- Auto and Liability Gaps That Escalate After an Accident

- Health and Life Coverage Shocks at the Worst Possible Time

- Business and Side-Hustle Overlaps That Policies Explicitly Exclude

Real Policyholder Stories: When the Claim Revealed the Gap

The claim denial is usually the first time a policyholder actually reads their policy. That is not an exaggeration. Homeowners in flood-adjacent areas routinely carry standard HO-3 policies, pay premiums for years, and then discover after a storm surge or heavy rain event that water entering from the ground up is categorically excluded. The policy covered wind damage to the roof. The insurance company paid for that. The $80,000 in water damage that entered through the foundation? Denied.

A similar pattern shows up in auto claims. A driver gets rear-ended by someone carrying only the state minimum liability of $25,000. Their medical bills reach $90,000. The at-fault driver’s insurer pays the policy limit and stops. If the victim did not carry adequate uninsured/underinsured motorist (UIM) coverage, the remaining $65,000 comes out of their own pocket. This scenario plays out thousands of times a year across states where minimum liability limits were set decades ago and never updated for modern medical costs.

The Delayed Reporting Trap

Another category of surprise involves timing. Most policies contain a prompt notification clause requiring policyholders to report a loss within a defined window, sometimes as short as 14 to 30 days. Homeowners who discover mold weeks after a slow leak, or business owners who notice water damage during a later renovation, often find their claim rejected not because the damage isn’t real, but because they waited too long to report it. The gap here is not in coverage language, it is in policyholder behavior colliding with policy conditions that insurers enforce strictly.

Why Standard Policies Leave These Holes by Design

Standard policies are not accidentally incomplete. They are priced and structured around named-peril or open-peril language that defines risk in ways that keep premiums manageable for insurers. Named-peril policies (like the HO-1 and HO-2 forms) only cover losses explicitly listed. Open-peril or “all-risk” policies like the HO-3 cover everything except what is explicitly excluded. The distinction sounds favorable to the consumer until you read the exclusions list, which routinely runs to several pages.

Flood, earthquake, sewer backup, mold, and ordinance-or-law upgrades are among the most common exclusions on HO-3 policies. Each of these represents a category where the risk is either highly concentrated geographically (flood, earthquake) or difficult to verify causation (mold, water intrusion). Insurers exclude them to avoid adverse selection and correlated losses, not as an oversight.

The Actual Cash Value Problem in 2026

One underappreciated gap is the difference between actual cash value (ACV) and replacement cost value (RCV) settlements. ACV pays what your property is worth today, after depreciation. A 10-year-old HVAC system worth $3,000 in ACV terms might cost $9,000 to replace in 2026. Unless your policy specifies replacement cost coverage for personal property and structures, you receive the depreciated amount. This gap has widened substantially since 2020, as Insurance Information Institute data shows construction material and labor costs rising 20–40% over that period without a corresponding automatic adjustment to most policy limits.

Ownership structure adds another layer of exposure that rarely gets discussed. If you hold your home in a trust or LLC for estate-planning purposes, your homeowners policy may list the individual as the named insured while the legal owner is the entity. Some insurers have denied claims outright on this basis, arguing the named insured has no insurable interest as an individual. Reviewing your declarations page against your deed is not optional if your ownership structure has changed.

The U.S. Government Accountability Office has documented how homeowners face coverage gaps when hurricane damage is split between multiple policies covering different perils. Wind damage goes to the homeowners policy; flood goes to the NFIP. Disputes over which caused which damage can delay or reduce payouts for years.

Homeowners Insurance Surprises That Hit After the Storm

Sewer backup is one of the most common and most underpurchased endorsements in homeowners insurance. Standard HO-3 policies exclude damage caused by water that backs up through sewers or drains. A single sewer backup event can cause $10,000 to $50,000 in structural and contents damage. The endorsement to add this coverage typically costs $50 to $150 per year. Most policyholders have never been told it exists.

Personal property sublimits create a similar problem for jewelry, art, collectibles, and electronics. Many HO-3 policies cap jewelry losses at $1,500 to $2,500, regardless of the item’s actual value. A $15,000 engagement ring stolen during a burglary is paid out at the sublimit unless the owner purchased a separate scheduled personal property endorsement. For a full breakdown of what your homeowners policy does and does not cover, the coverage review guide at Smart Insurance 101 walks through each coverage layer in plain terms.

Auto and Liability Gaps That Escalate After an Accident

State minimum liability limits are dangerously low relative to actual accident costs in 2026. Many states still mandate only $25,000 per person / $50,000 per accident in bodily injury liability. The average verdict in a serious auto injury case routinely exceeds $100,000, and catastrophic cases can reach seven figures. Carrying only the state minimum means your insurer pays out, stops, and you are personally liable for the remainder. This is not a rare edge case; it is the standard outcome for drivers who select minimum coverage to reduce their premium.

Rental and Rideshare Coverage Holes

Rental car coverage is another gap that surprises drivers. Most personal auto policies provide liability coverage in a rental under certain conditions, but collision and comprehensive coverage on the rental vehicle depends on whether you carry those coverages on your own vehicle. If you drive an older car and have dropped collision to save money, you have no collision coverage on a rental either. The NAIC’s white paper on ridesharing insurance specifically addresses the gap that exists when a driver is in “Period 1”, the app is on, but no passenger has been accepted, during which personal auto policies typically do not apply and the TNC’s commercial policy has not yet activated.

Umbrella liability policies address several of these shortfalls at once. A personal umbrella policy typically provides $1 million or more in excess liability coverage above your auto and homeowners limits, and it costs $150 to $300 per year for the first million. For a realistic look at how lawsuit costs have climbed and why standard limits fall short, see this analysis of why liability insurance costs keep rising.

According to the Commonwealth Fund’s 2025 survey, 21% of U.S. working-age adults with private insurance reported a denial of coverage for doctor-recommended care in the past year. That is roughly one in five insured adults encountering a gap they paid premiums to avoid.

Health and Life Coverage Shocks at the Worst Possible Time

Out-of-network billing is the most common health insurance gap and the one most people misunderstand until they receive the explanation of benefits. Even when you choose an in-network hospital, the anesthesiologist, radiologist, or specialist brought in during your procedure may be out-of-network. The No Surprises Act, effective January 2022, limited this practice for emergency care and some non-emergency situations, but gaps remain for ground ambulance services, which the law does not fully address.

The deeper gap in health coverage is structural., the KFF reports that 9.8% of Americans under age 65 were uninsured, with 1.4 million people falling into the Medicaid coverage gap in non-expansion states. These individuals earn too much to qualify for Medicaid but too little to receive meaningful Marketplace tax credits. For them, the coverage gap is not a policy exclusion, it is an income threshold set by law. Understanding how deductibles compare to out-of-pocket maximums is critical for anyone pricing coverage near this income boundary.

Life Insurance Underinsurance

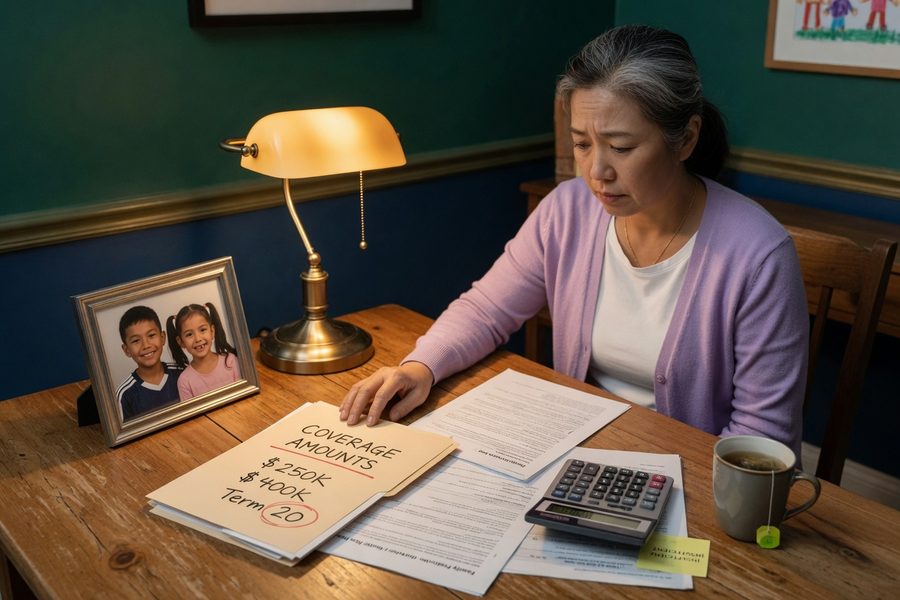

Life insurance carries its own version of underinsurance. LIMRA data shows 47% of families with children report insufficient coverage relative to income replacement needs. The standard rule of thumb is 10 to 12 times annual income, but many policyholders buy a flat $250,000 or $500,000 policy and never revisit it after a raise, a mortgage increase, or the birth of a child. A $250,000 policy on a household earning $100,000 per year covers two and a half years of income, nowhere near enough for a surviving spouse with dependent children. Reviewing your current coverage against current term life options in 2026 can identify whether your existing policy still fits your actual exposure.

Request your policy’s declarations page and endorsements list together, not just the summary brochure. The declarations page states your actual limits and deductibles; the endorsements either add or subtract coverages from the base form. If your agent cannot produce both documents within 24 hours, treat that as a signal to review your coverage placement.

Business and Side-Hustle Overlaps That Policies Explicitly Exclude

Personal auto and homeowners policies contain explicit exclusions for business use. A photographer who shoots weddings from their personal vehicle, a freelance consultant whose laptop is stolen from their home office, a delivery driver using their personal car, each of these individuals has a claim that their personal insurer can and likely will deny. The exclusion language typically reads that losses “arising out of or in connection with a business activity” are not covered under the personal policy. No ambiguity, no gray area.

The fix varies by situation. Home-based business owners can often add a home business endorsement for $25 to $75 per year that extends coverage to business equipment. Drivers who regularly use their vehicle for paid deliveries or rideshare need a commercial endorsement or a separate commercial auto policy. The commercial insurance overview at Smart Insurance 101 outlines which endorsements are available and when a standalone policy is necessary. The NAIC’s Cannabis Insurance Working Group has similarly identified that smaller cannabis businesses face coverage gaps because many standard commercial carriers decline to write the coverage, pushing these businesses into the non-admitted market with fewer consumer protections.

| Coverage Gap | Standard Policy Status | Estimated Annual Fix Cost |

|---|---|---|

| Sewer Backup | Excluded on HO-3 | $50–$150 endorsement |

| Flood Damage | Excluded on HO-3 | $700–$2,500+ (NFIP or private) |

| Jewelry / Valuables | Sublimited ($1,500–$2,500) | $100–$300 scheduled endorsement |

| Underinsured Motorist | Optional in most states | $50–$200 added to auto policy |

| Personal Umbrella | Not included in any base policy | $150–$300 for $1M coverage |

| Home Business Equipment | Excluded (business use clause) | $25–$75 endorsement |

| Rideshare Period 1 Gap | Personal policy excludes; TNC policy not yet active | $15–$40/month (rideshare endorsement) |

A household earning $80,000 per year with a $250,000 life insurance policy has effectively covered 3.1 years of income replacement. At a recommended 10x multiplier, that same household needs $800,000 in coverage, more than three times what a typical “starter” life policy provides. The dollar gap is $550,000, which is the difference between a surviving spouse maintaining their standard of living and not.

Frequently Asked Questions

What are the most common insurance coverage gaps homeowners miss?

Flood damage, sewer backup, and mold remediation top the list. Standard HO-3 policies exclude all three, yet most homeowners are unaware until after a claim. Personal property sublimits on jewelry and electronics are a close fourth, with caps as low as $1,500 on items worth many times that amount.

Does renters insurance cover everything in my apartment?

No. Renters insurance covers personal property against named or open perils and provides liability coverage, but it excludes flood, earthquake, and high-value items above sublimits. If your laptop costs $2,000 and your policy has a $1,500 electronics sublimit, you absorb the difference. Scheduled endorsements for high-value items are available on most renters policies for a modest additional premium.

Can an insurer deny a claim just because I was using my car for deliveries?

Yes, and they do. Personal auto policies contain explicit business-use exclusions. If you were driving for a paid delivery service or rideshare platform at the time of the accident, your personal insurer can deny the claim entirely. A rideshare endorsement or commercial auto policy is required to close this gap.

What is the Medicaid coverage gap and who does it affect?

The Medicaid coverage gap affects low-income adults in states that have not expanded Medicaid under the Affordable Care Act. These individuals earn too much to qualify for their state’s Medicaid program but too little to receive Marketplace premium tax credits, which begin at 100% of the federal poverty level., an estimated 1.4 million people remain in this gap.

Does my homeowners policy automatically update coverage as home values increase?

Most do not, unless you have an inflation guard endorsement that adjusts limits annually. Without it, your coverage limit stays flat while rebuild costs rise. Since 2020, construction costs have increased 20–40% in many markets, which means a policy written in 2020 could leave you significantly underinsured for a total loss today.

Is an umbrella policy worth buying if I already have good auto and homeowners coverage?

For most homeowners and drivers with assets to protect, yes. A personal umbrella policy adds $1 million or more in excess liability coverage above your existing auto and homeowners limits for $150 to $300 per year. Given that serious auto injury verdicts regularly exceed $100,000 and premises liability cases can reach far higher, the cost-to-coverage ratio is difficult to argue against. The one honest limitation: umbrella policies do not cover professional liability or business activities, so they do not replace commercial coverage.

Sources

- KFF, Key Facts About the Uninsured Population (2024)

- Commonwealth Fund, How Health Insurance Coverage Denials Affect Americans: 2025 Affordability Survey

- U.S. Government Accountability Office, Hurricane Insurance Coverage Gaps and Claims Uncertainties

- National Association of Insurance Commissioners, Commercial Ride-Sharing Insurance Principles

- National Association of Insurance Commissioners, Cannabis and Insurance Coverage Gaps

- healthinsurance.org (citing KFF), What Is the Medicaid Coverage Gap and Who Does It Affect? (2025)

- California Department of Insurance, NAIC Adoption of Ridesharing Insurance White Paper

- Insurance Information Institute, Home Construction Cost and Replacement Value Data