Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

Dog bite liability homeowners insurance covers dog-related injuries under your policy’s personal liability section, but insurers can restrict or exclude coverage based on your dog’s breed. In 2025, U.S. homeowners insurers paid out $1,862 million on 28,450 dog bite claims, with the average claim costing $65,450. Breed restrictions, bite-history underwriting, and state laws all determine what your policy actually covers.

Dog bite liability homeowners insurance sits at the intersection of pet ownership and property coverage, and the stakes are higher than most policyholders realize. According to the Insurance Information Institute’s 2025 dog bite liability data, the average cost per claim reached $65,450 last year, nearly double what it was in 2016. That figure reflects rising medical costs, increased litigation, and more aggressive plaintiff-side legal strategies.

What makes this coverage especially tricky is the breed question. Your insurer may cover your Labrador without a second glance, then deny coverage or exclude liability entirely because you own a Rottweiler. This guide explains how breed restrictions work, which states limit insurers’ ability to use them, how the largest carriers are evolving their underwriting, and what you can do to stay covered no matter what breed you own.

Key Takeaways

- U.S. homeowners insurers paid $1,862 million on dog bite and dog-related injury claims in 2025, according to Insurance Information Institute and State Farm data.

- The average dog bite claim cost $65,450 in 2025, a 97% increase from 2016 levels, per Triple-I’s 2025 analysis.

- There were 28,450 dog bite claims filed nationally in 2025, with 2,830 in California alone, the highest of any single state (Insurance Information Institute, 2025).

- The National Association of Insurance Commissioners (NAIC) has noted a lack of conclusive data linking specific breeds to higher claims risk when controlling for individual history (NAIC, breed-specific legislation).

- An estimated 68 million U.S. households own dogs, meaning a large share of homeowners policies carry some level of dog bite exposure (American Pet Products Association 2024-2025 survey, via Triple-I).

In This Guide

- How Dog Bites Drive Homeowners Insurance Claims and Costs

- Which Breeds Trigger Restrictions and Why

- What Happens to Your Policy When You Own a Restricted Breed

- Do State Laws Protect You from Breed-Based Denials?

- How Leading Insurers Evaluate Dogs Beyond Breed

- Practical Steps to Secure or Maintain Coverage With Any Dog

- Long-Term Trends Every Dog Owner Should Watch

How Dog Bites Drive Homeowners Insurance Claims and Costs

Dog bites are one of the most expensive and consistent sources of homeowners liability claims in the country. The numbers make the case plainly: 28,450 claims were filed nationwide in 2025, and insurers paid out a combined $1,862 million to cover them, according to the Insurance Information Institute’s 2025 dog bite spotlight report. Dog-related incidents now account for more than one-third of all homeowners liability claim dollars.

The cost trajectory is just as striking. From 2016 to 2025, the average payout per claim climbed 97%, reaching $65,450. That increase reflects two compounding pressures: medical costs (reconstructive surgery, infection treatment, and long-term care) and legal costs, as more victims retain attorneys and pursue larger settlements. A single serious bite on a neighbor’s child can easily push past six figures once emergency room bills, lost wages, and pain-and-suffering damages are factored in.

In 2025, 2,830 dog bite claims were filed in California alone, more than any other state. With an average claim cost of $65,450, California’s total exposure from dog bites exceeded $185 million in a single year (2,830 x $65,450 = $185,223,500).

Why Breed Perceptions Shape Insurer Pricing

Insurers price risk using historical claims data, and certain breeds appear disproportionately in that data. Whether that overrepresentation reflects genuine behavioral differences or factors like ownership patterns, training quality, and reporting bias is genuinely contested. What is not contested is that the financial exposure is real, and insurers have strong incentive to act on whatever signals their actuarial models surface. For a deeper look at how rising claim costs are affecting premiums across the board, see our analysis of why insurance premiums are exploding.

Which Breeds Trigger Restrictions and Why

The breeds that appear most often on insurer restriction lists include Pit Bull Terriers, Rottweilers, Doberman Pinschers, German Shepherds, Akitas, Chow Chows, Siberian Huskies, and Wolf Hybrids. Carriers like State Farm, Allstate, Farmers, and Liberty Mutual have historically maintained some version of these lists, though their current approaches differ significantly.

Here’s the thing: the breed identification problem is significant. Mixed-breed dogs account for a large portion of the U.S. dog population, and visual breed identification, even by professionals, carries a high error rate. A dog that looks like a Pit Bull may have little or no Pit Bull genetics. Carriers that use appearance-based standards expose themselves to inconsistent underwriting, and owners of misidentified dogs face denials they have legitimate grounds to dispute. This gap between stated breed policy and practical enforcement is one of the least-discussed complications in this space.

What Happens to Your Policy When You Own a Restricted Breed?

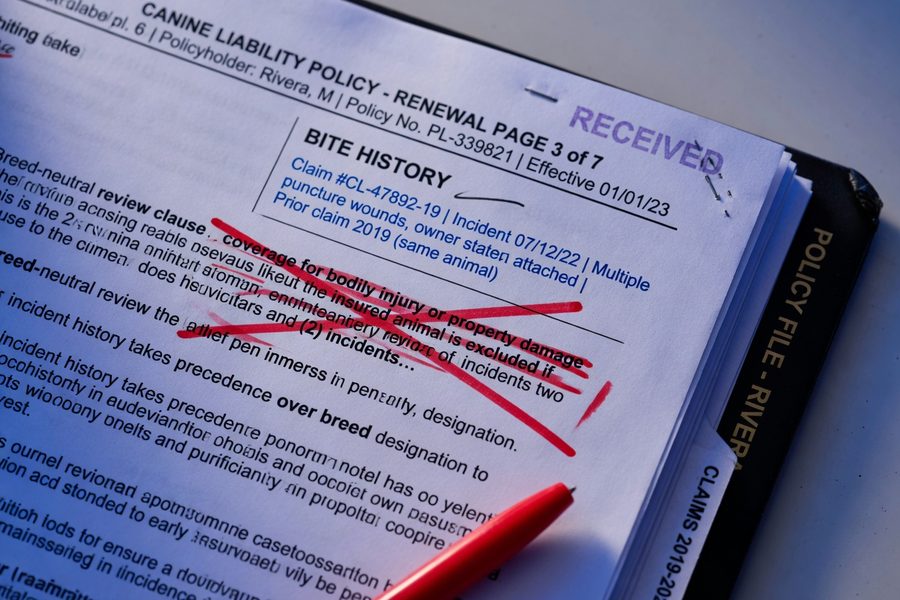

Three distinct outcomes are possible, and they are not equally bad. First, an insurer may deny your application outright. Second, they may issue a policy with a breed-specific liability exclusion, meaning your home is covered for fire, theft, and other perils, but any dog bite claim involving that animal will be denied. Third, they may apply a premium surcharge and cover the dog under standard terms.

The exclusion scenario is the most dangerous for homeowners because it creates a false sense of security. Your policy documents exist, your premium gets paid, and you assume you are covered. Then a bite claim arrives and the exclusion clause surfaces. The Texas Department of Insurance advises policyholders directly: “Homeowners insurance might cover dog bite costs, but some policies exclude certain breeds, so policyholders should check their policy or contact their insurer.” That advice applies equally in every state.

Conditions and Documentation Requirements

Some carriers will cover restricted breeds under added conditions. Common requirements include: proof of obedience training from an accredited program, a fenced yard meeting specific height requirements, written confirmation the dog has no prior bite history, and in some cases a signed liability waiver. Fulfilling these conditions does not guarantee coverage renewal if a bite occurs. Some policies include language that allows the insurer to non-renew at the next policy anniversary following any dog-related incident, regardless of who was at fault.

A breed-specific liability exclusion in your homeowners policy can leave you personally responsible for $65,450 or more out of pocket if your dog bites someone. The exclusion does not appear on your declarations page; it is buried in the endorsements section of your policy documents.

| Policy Outcome | Coverage Status | Owner Risk | Typical Trigger |

|---|---|---|---|

| Full Coverage | Dog included under liability section | Low, insurer pays claims up to policy limits | No restricted breed, no prior bite history |

| Breed Exclusion Endorsement | Home covered; dog liability excluded | High, owner pays 100% of bite claim costs | Restricted breed identified at application |

| Premium Surcharge | Full coverage with added cost | Moderate, covered but higher annual premium | Restricted breed with clean bite history |

| Application Denial | No policy issued | Very High, must find specialty insurer | Prior bite claim or highest-risk breed list |

| Non-Renewal Notice | Coverage ends at policy term | High, must requalify elsewhere | Bite incident occurs during policy period |

Do State Laws Protect You from Breed-Based Denials?

Yes, but with meaningful limits. A growing number of states have enacted laws that restrict or prohibit insurers from making coverage decisions based solely on breed. As of early 2026, states including New York, Nevada, Pennsylvania, Michigan, and Colorado have passed legislation requiring insurers to evaluate dogs on individual bite history rather than breed alone. The specific protections vary: some states ban outright denials based on breed, others prohibit premium surcharges, and a few require that any breed-based decision be supported by actuarial data.

The National Association of Insurance Commissioners has noted a lack of conclusive data linking specific breeds to higher claims risk, and has been in active discussions about model legislation that would standardize how states handle breed-based underwriting. The National Council on Insurance Legislators (NCOIL) has also developed model language that several states are now using as a template.

What Protections Don’t Cover

These laws address breed-only discrimination. An insurer in a protected state can still deny or surcharge coverage if your dog has an actual bite history on record. The distinction matters: breed protection does not equal unconditional coverage. Owners in states with strong protections still need to disclose a dog’s individual history honestly, because misrepresentation at application is grounds for claim denial in every jurisdiction. As the Maryland Insurance Administration has clarified: “Insurers may make the business decision to exclude from liability coverage losses caused by specific breeds or specific mixed breeds of dogs in homeowners or renters policies.” Even in states with moderate protections, a liability exclusion is often still permissible.

How Leading Insurers Evaluate Dogs Beyond Breed

State Farm and Allstate, two of the largest homeowners insurers in the country, have publicly moved toward bite-history underwriting rather than fixed breed lists. Under this model, a dog with no bite incidents on record may qualify for coverage regardless of breed, while a dog with a documented bite history faces restrictions regardless of breed. This shift is meaningful because it aligns underwriting with actual risk evidence rather than breed stereotypes.

The practical catch is documentation. Bite-history underwriting requires insurers to verify what they are being told. Owners should be prepared to provide veterinary records confirming behavioral health, documentation of any training certifications, and a written statement about the dog’s prior incidents. If a dog bit someone and that claim was paid under a previous policy, that record will surface during underwriting. Honesty upfront costs less than a denied claim later.

If your insurer is switching to bite-history underwriting, get your dog enrolled in a recognized obedience program and keep the certificate. Several carriers reduce liability surcharges or remove breed restrictions entirely for dogs with documented training from an American Kennel Club Canine Good Citizen program or equivalent. Ask your agent whether your specific carrier has a formal credit for this.

Umbrella Policies and Specialty Dog Liability Coverage

Standard homeowners liability limits typically run from $100,000 to $300,000. Given that a serious dog bite case can reach or exceed those limits after medical expenses, legal fees, and damages, a personal umbrella policy is worth serious consideration. Umbrella policies extend liability coverage by $1 million or more and often include dog bite claims, unless your homeowners policy already excludes the specific dog. If it does, the umbrella exclusion usually follows. Separate dog liability insurance is available from specialty carriers for this scenario.

Practical Steps to Secure or Maintain Coverage With Any Dog

Disclosure is non-negotiable. Every insurer application asks about dog ownership, and omitting a dog that later bites someone gives the carrier grounds to deny the claim and potentially rescind the policy. Beyond disclosure, the steps below give you the best chance of securing favorable terms.

- Shop multiple carriers before assuming you are uninsurable. Underwriting standards differ significantly across State Farm, Allstate, USAA, Nationwide, and regional insurers.

- Use an independent agent who has access to carriers beyond the standard market, including specialty insurers who cover restricted breeds.

- Obtain and keep copies of your dog’s obedience training certificates, vaccination records, and behavioral assessments from a licensed veterinarian.

- If your application is denied, request the specific reason in writing. In states with breed-neutral laws, a denial based solely on breed may be challengeable with your state’s insurance department.

- Review the liability section of your current policy annually. Breed lists and exclusion language can change at renewal without prominent notice.

For owners who are shopping for a new homeowners policy while also managing dog bite liability concerns, our homeowners insurance beginner’s overview covers the full structure of a standard policy, including how personal liability works and where exclusions typically appear.

One honest caveat: even with all the right documentation, some carriers in some states will still decline to cover certain breeds. That is not necessarily illegal where no protective statute exists, and it is not always negotiable. Knowing this ahead of time means you can plan for a specialty policy rather than discovering the gap after a claim.

The liability exposure from dog bites is also worth reviewing in context of broader personal liability risk. Our coverage of why lawsuits are quietly getting more expensive explains the litigation trends driving claim severity upward across personal liability lines, including dog bite cases.

Long-Term Trends Every Dog Owner Should Watch

The legislative momentum toward breed-neutral insurance laws is accelerating. Several additional states have active bills in 2025-2026 that would require actuarial justification before any breed-based underwriting decision can be made. If those bills pass, insurers will need to rely on individual bite records, not breed classifications, to justify exclusions or surcharges. That is a significant operational shift for carriers whose current systems flag breeds at the application stage.

At the same time, claims data will increasingly drive the debate. With 68 million dog-owning households generating data points, insurers and regulators will have more statistical power to test whether breed is actually a meaningful predictor of claim severity once individual history, training status, and owner behavior are controlled for. The evidence so far, as reflected in the NAIC’s own analysis, suggests breed alone is a poor predictor. If the data continues in that direction, the breed restriction model may become both legally and actuarially untenable in most states.

New dog owners and anyone relocating to a different state should treat insurance review as a first step, not an afterthought. Your policy’s dog liability terms can change when you move, because insurer filings and state regulations vary by location. For a fuller picture of how these changes fit into your overall homeowners coverage, the section on important homeowners insurance policies is a useful reference. And if premium increases from any source are straining your budget, our guide on how to save money on your homeowners insurance covers practical reduction strategies that do not require sacrificing coverage quality.

Frequently Asked Questions

Does homeowners insurance automatically cover dog bites?

Most standard homeowners policies include personal liability coverage that pays for dog bite claims, but coverage is not automatic if your dog is on the insurer’s restricted breed list. The Texas Department of Insurance advises all policyholders to check their policy terms or contact their insurer directly, since breed exclusions may apply even when a policy is otherwise in force.

Can an insurer deny my application because of my dog’s breed?

Yes, in most states. Insurers have broad underwriting discretion to decline applications based on breed unless a state law specifically prohibits it. As of early 2026, states including New York, Nevada, Pennsylvania, and Michigan have laws limiting or banning breed-only denials, but coverage decisions based on bite history remain permissible everywhere.

What happens if my dog bites someone and my policy has a breed exclusion?

Your insurer will deny the claim. The breed exclusion endorsement removes dog bite liability for the named breed from your policy entirely, leaving you personally responsible for all costs. With the national average claim running at $65,450, that exposure is substantial and could result in a lawsuit, wage garnishment, or asset seizure if the judgment exceeds what you can pay.

Is renters insurance affected by breed restrictions the same way homeowners insurance is?

Yes. Renters insurance includes personal liability coverage that behaves similarly to a homeowners policy’s liability section, and insurers apply the same breed restriction logic to both products. The Maryland Insurance Administration has confirmed that insurers may exclude liability coverage for specific breeds under homeowners or renters policies. If you rent and own a restricted breed, verifying your renters policy’s liability terms is just as important as it would be for a homeowner.

Can I appeal a breed-based coverage denial?

You can, and in states with breed-neutral laws, a formal complaint to the state insurance department is a legitimate next step. Outside those states, internal appeals rarely succeed, but requesting the insurer’s written reasoning puts you in a better position to shop alternatives. Some owners have had exclusions removed by providing behavioral assessments, training records, and evidence of the dog’s individual history at the time of underwriting review.

Sources

- Insurance Information Institute, Spotlight on Dog Bite Liability (2025)

- National Association of Insurance Commissioners, Breed-Specific Legislation and Insurance

- Texas Department of Insurance, Home Insurance Might Cover Dog Bites

- Maryland Insurance Administration, Bulletin 15-25: Homeowners and Renters Insurance Dog Bite Liability

- American Pet Products Association 2024-2025 Pet Owners Survey (via Insurance Information Institute)

- Smart Insurance 101, Liability Insurance: Why Lawsuits Are Quietly Getting More Expensive