Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

Retirees on fixed incomes can reduce homeowners insurance premiums by 10–25% through mature homeowner discounts, bundling home and auto policies, raising deductibles strategically, and installing qualifying security upgrades, without dropping replacement cost coverage or key liability protection. State insurance departments confirm savings of 5–20% from bundling alone.

Homeowners insurance for retirees is one of the most manageable fixed expenses in a retirement budget, but only if you know which levers actually move the needle. The U.S. Census Bureau’s 2025 property insurance report found that 5.3 million U.S. households paid more than $4,000 a year for property insurance in 2023, a figure that lands especially hard when your income is fixed and no longer growing with inflation. The problem is real, and it compounds every renewal cycle.

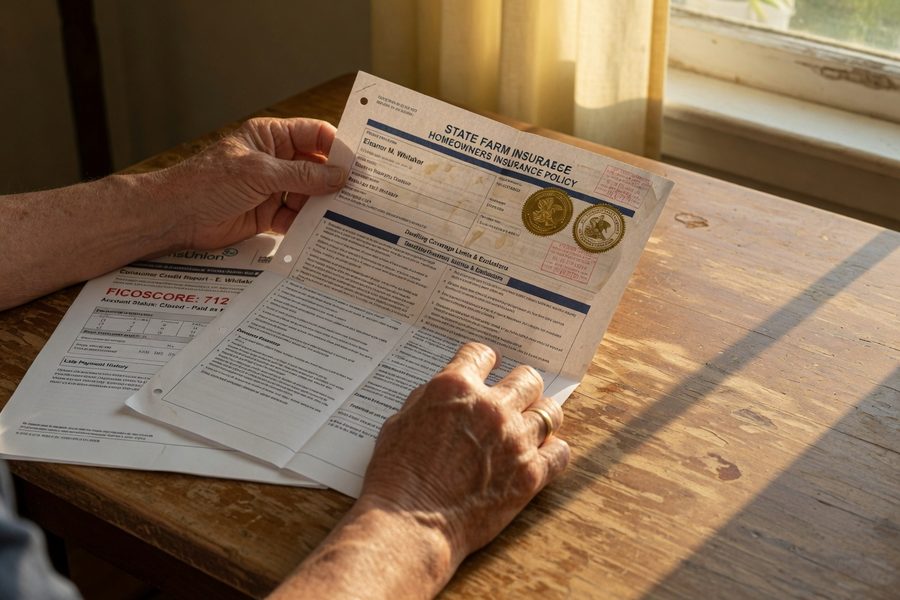

Age is not a rating factor for homeowners insurance. Your premium is driven by your credit-based insurance score, claims record, home features, and location. That means many retirees with clean records can pay less than younger neighbors with poor credit. This guide covers which discounts you genuinely qualify for, which coverage changes protect you and which ones leave you exposed, and how to shop without accidentally gutting the policy you spent decades building.

Key Takeaways

- Mature homeowner discounts (typically age 55+, fully retired) can reduce premiums by 10–25%, according to multiple carrier programs including those cited by the New York State Department of Financial Services.

- Bundling home and auto insurance saves an average of $963 per year for AARP members using The Hartford’s program, with home-specific savings around $366 annually.

- Florida homeowners paid a median of $2,273 per year for property insurance in 2023, the highest of any state, according to U.S. Census Bureau data.

- The California Department of Insurance confirms that shopping around, raising deductibles, and bundling can save seniors 5–20% on premiums.

- Claims-free discounts commonly reach up to 20%, and loyalty programs reward continuous coverage, two categories where long-term homeowners have a clear advantage.

In This Guide

- Why Homeowners Insurance Costs Hit Retirees on Fixed Incomes Hardest

- What Coverage Do You Actually Need in Retirement?

- Retiree Discounts That Don’t Require Cutting Protection

- Home Changes and Habits That Lower Your Premium

- How to Shop and Compare Quotes Without Losing Key Protections

- Other Proven Ways to Reduce Costs on a Fixed Income

Why Homeowners Insurance Costs Hit Retirees on Fixed Incomes Hardest

Premiums have climbed sharply in high-risk states over the past three years, and retirees absorb those increases differently than working households. In Texas, the average annual homeowners insurance premium reached $3,506 in 2025, according to preliminary data from the Texas Department of Insurance. When Social Security is your primary income source and that check doesn’t move much, a $400-per-year premium increase is genuinely disruptive.

There’s a structural reason this stings more for retirees: once the mortgage is paid off, no lender is requiring you to maintain any particular coverage level. That freedom sounds appealing, but it creates a real temptation to underinsure. Dropping to actual cash value (ACV) coverage or slashing liability limits to shave $30 a month can leave you with a six-figure shortfall after a major loss. The math works against you when you have fewer working years ahead to rebuild savings.

Age Doesn’t Raise Your Rate, But Other Factors Do

Insurers in most states are prohibited from using age as a direct rating factor for homeowners insurance. What they do use is your credit-based insurance score (distinct from a standard FICO Score, though the two are related), claims history, and the physical characteristics of your home. A retiree with a 30-year claim-free record and strong credit often pays less than a 35-year-old first-time buyer in a newer home. The problem is that older homes tend to have older roofs, outdated electrical panels, and aging plumbing, all of which raise rates regardless of who lives there.

Climate risk is making the market harder in specific regions. Insurers have pulled back from high-risk states, reduced coverage options, and raised wind and flood deductibles to levels that can catch retirees off guard. The retiree who bought a policy in coastal Florida a decade ago may find the renewal today looks nothing like the original contract.

What Coverage Do You Actually Need in Retirement?

Replacement cost coverage is the right choice for most retirees, full stop, unless you have a documented plan for what happens if your home is a total loss. Replacement cost pays what it actually costs to rebuild your home at today’s material and labor prices. Actual cash value pays that amount minus depreciation, which on a 25-year-old roof can mean receiving a fraction of what you need. For a retiree on a fixed income, that gap rarely gets filled from savings.

The Replacement Cost vs. ACV Trade-Off Specific to Retirement

Some retirees argue they wouldn’t rebuild after a total loss anyway, they’d sell the lot or move to assisted living. That’s a legitimate consideration. If you have a clear, documented exit strategy and meaningful assets elsewhere, switching to ACV coverage could be a rational financial decision, not just a cost-cutting shortcut. The trade-off is real: ACV premiums can run noticeably lower, but you’re self-insuring the depreciation gap. Most financial planners recommend staying with replacement cost unless your liquid assets can comfortably cover that gap.

Liability coverage deserves its own review. Retirees often host grandchildren, employ household help, or have guests at a higher rate than working households. Liability claims from slip-and-fall incidents or dog bites don’t shrink in retirement. The cost of liability claims has risen sharply in recent years. Maintain at least $300,000 in liability coverage, and consider a personal umbrella policy if you have substantial assets to protect.

Personal property limits are worth trimming if your lifestyle has genuinely simplified. If you’ve downsized and your home has fewer valuables, reducing personal property coverage to match actual inventory is a legitimate and honest savings move. Schedule an annual inventory to verify your limits still reflect what you own.

A standard homeowners policy covers personal property at 50–70% of your dwelling coverage by default. If you’ve downsized significantly, you may be paying to insure belongings you no longer own. Adjusting this limit to match a current home inventory is one of the cleanest ways to reduce premiums without sacrificing protection where it counts.

Retiree Discounts That Don’t Require Cutting Protection

Mature homeowner discounts are real, and they’re broader than most people realize. Many carriers offer credits ranging from 10–25% specifically for policyholders who are 55 or older and fully retired with the insured home as their primary residence. The eligibility rules matter: most programs require that you are fully retired, not just age-eligible, and that the home is your principal dwelling rather than a vacation or investment property.

What Qualifies, and What Disqualifies, You for Senior Discounts

The New York State Department of Financial Services confirms that many insurers offer discounts to senior citizens or retirees on homeowners insurance, but availability varies by carrier and state. The most common disqualifiers are partial employment income (some carriers require full retirement), using the home as a rental or short-term rental even occasionally, and having a recent claims history that offsets the credit.

AARP members bundling home and auto with The Hartford save an average of $963 per year total, with the home-specific component around $366 annually. That’s a meaningful number on a fixed income without any reduction in coverage. Travelers, Allstate, and Nationwide all offer comparable senior or mature homeowner programs, though the exact discount percentage varies by state and policy structure.

Claims-free discounts stack on top of age-related credits. Policyholders with no claims in the past three to five years commonly qualify for discounts reaching up to 20%. Loyalty discounts for staying with a single carrier long-term add another layer. Retirees who have held the same policy for a decade or more are often sitting on unredeemed loyalty credits they’ve never been told to ask for, which is why a direct conversation with your agent matters.

The Texas Department of Insurance advises homeowners to ask their carrier directly about every discount they may qualify for, including credits for home security systems, smoke detectors, and bundling policies. Those discounts are not always applied automatically, and carriers are not required to volunteer them at renewal.

| Discount Type | Typical Savings | Common Eligibility Requirement | Representative Carriers |

|---|---|---|---|

| Mature/Senior Homeowner | 10–25% | Age 55+, fully retired, primary residence | The Hartford, Travelers, Allstate, Nationwide |

| Claims-Free | Up to 20% | No claims in prior 3–5 years | Most major carriers |

| Home + Auto Bundle | $366–$963/yr (home component ~$366) | Both policies with same insurer | The Hartford (AARP), Allstate, Travelers |

| Monitored Security System | 5–20% | Central-station monitored alarm installed | Most major carriers |

| Smoke Detectors / Deadbolts | 2–5% (stackable) | Qualifying devices installed and disclosed | Most major carriers |

| Annual Premium Payment | 3–5% (eliminates installment fees) | Full-year premium paid upfront | Most major carriers |

| Higher Deductible ($500 → $1,000) | 5–10% | Policyholder accepts higher out-of-pocket on claims | Most major carriers |

Home Changes and Habits That Lower Your Premium

Security and safety upgrades are among the most cost-effective investments for premium reduction. A monitored alarm system typically earns a discount of 5–20% depending on the carrier, while smoke detectors, deadbolt locks, and carbon monoxide detectors qualify for smaller but stackable credits. The Illinois Department of Insurance specifically recommends asking your agent about discounts for installing security devices as a straightforward way to lower premiums without reducing coverage.

Why Being Home More Often Is an Actual Advantage

Retirees who are home during the day present a measurably lower risk profile: small fires, water leaks, and break-ins are caught sooner. Several major carriers, including Travelers, explicitly factor occupancy into their pricing models for mature homeowner discounts. A house that is occupied most of the day is statistically less likely to suffer a total loss from a slow-developing hazard. This is one area where retirement genuinely works in your favor on a premium, rather than against it.

If you live in a gated community or an age-restricted development, ask your insurer whether those features qualify for a community security discount. Not every carrier advertises this, but many will apply it when asked directly.

A Texas retiree paying the state average of $3,506 per year who qualifies for a 15% mature homeowner discount, a 10% claims-free credit, and a 5% security system discount could reduce their annual premium by approximately $1,052 (30% of $3,506), bringing the new annual cost to roughly $2,454, or about $87.75 per month less, without reducing any coverage limits.

How to Shop and Compare Quotes Without Losing Key Protections

Getting multiple quotes is the single most reliable way to find a better rate on identical coverage. The Utah Insurance Department recommends shopping around, and the California Department of Insurance estimates that comparison shopping, combined with raising deductibles and bundling, can save seniors 5–20% on premiums. The critical discipline is comparing policies at the same coverage level: same dwelling limit, same liability limit, same deductible, so you’re evaluating price rather than quietly trading protection for savings.

The trap most retirees fall into when switching carriers is accepting a lower quote that comes with reduced limits or an ACV endorsement buried in the fine print. Read the declarations page of any competing quote before you sign. If an agent can’t explain why the premium is lower, that’s a red flag, not a deal.

For guidance on what to look for before you compare quotes, our homeowners insurance guide for beginners walks through the key policy components worth verifying. Reviewing that framework before you contact carriers will help you ask the right questions. An annual review, ideally 60 days before renewal, gives you time to shop without pressure and apply any discount updates from home improvements made during the year.

One underused resource: your state’s insurance department. The New York State Department of Financial Services, the California Department of Insurance, and the Texas Department of Insurance all publish free consumer guides listing common discounts and carrier complaint data. Checking an insurer’s complaint ratio through your state department or through the National Association of Insurance Commissioners (NAIC) takes ten minutes and can save you from switching to a carrier with a poor claims-paying record.

When requesting quotes, ask each insurer to itemize every discount applied to the quoted premium. Then ask what you would need to do to qualify for any discounts not currently applied. This single question often surfaces credits for security upgrades, claims-free status, or retirement occupancy that agents don’t volunteer automatically.

Other Proven Ways to Reduce Costs on a Fixed Income

Bundling home and auto coverage with a single carrier is the most straightforward savings move available to retirees who still own a vehicle. The California Department of Insurance lists bundling as one of its top recommendations for senior homeowners, and the average savings figures support the advice. If you’re also reviewing your auto coverage, strategies for saving on homeowners insurance pair well with concurrent auto policy reviews to maximize the bundle discount.

Raising your deductible is the other lever with immediate premium impact. Moving from a $500 deductible to a $1,000 deductible typically reduces the annual premium by 5–10%, according to guidance from the Utah Insurance Department. The honest trade-off: you absorb more out-of-pocket cost on smaller claims. This strategy makes sense if you have an accessible emergency fund that could cover the higher deductible without financial strain, and if you have a strong claims-free history, meaning you’re unlikely to need it often. It’s the wrong move if a $1,000 unexpected expense would create real hardship.

Paying your premium annually rather than monthly eliminates installment fees that typically add 3–5% to the effective annual cost. If cash flow allows a lump-sum payment, this is one of the lowest-effort savings available. Some carriers also offer a small discount for setting up automatic payments, which is worth asking about directly.

Your credit-based insurance score is another factor worth monitoring. Unlike a standard FICO Score used for mortgage or auto lending, a credit-based insurance score is calculated specifically for underwriting purposes, but the underlying credit data from bureaus like Experian, Equifax, and TransUnion feeds both. Paying down revolving balances, avoiding late payments, and correcting errors on your credit report can meaningfully improve your insurance score over time. Retirees who have paid off major debts and carry no credit card balances often have strong profiles here without realizing it. Ask your carrier how your credit-based insurance score affects your current rate.

For retirees in states where standard coverage has become difficult to obtain or afford due to climate risk, state FAIR Plans (Fair Access to Insurance Requirements) provide a last-resort option. These are state-backed programs designed to cover homes that private insurers won’t insure, and they exist in most states. Coverage is typically more limited and more expensive than a standard policy, so FAIR Plans should be a fallback, not a first choice. Check with your state insurance department for eligibility rules specific to your location.

Frequently Asked Questions

Do retirees automatically qualify for lower homeowners insurance rates?

No discount is automatic, you have to ask for it. Many carriers offer mature homeowner or senior credits for policyholders who are typically 55 or older and fully retired with the home as their primary residence, but these discounts are not applied unless you request them or an agent proactively reviews your file. Call your carrier and ask specifically which discounts are currently applied to your policy and which ones you might qualify for that aren’t.

Does paying off my mortgage change what homeowners insurance I need?

Paying off your mortgage removes the lender’s coverage requirements, but it doesn’t change what protection you actually need. Without a lender mandate, you could legally drop down to minimal coverage, but if your home is your largest asset, that’s a significant financial risk. Most financial advisors recommend maintaining replacement cost dwelling coverage and adequate liability limits regardless of mortgage status.

Is it worth raising my deductible to lower my premium?

It depends on your emergency fund. Raising your deductible from $500 to $1,000 typically reduces premiums by 5–10%, which on a $2,500 annual premium saves roughly $125–$250 per year. If you can comfortably cover the higher deductible from savings without stress, that trade-off usually works in your favor over time, unless you file a claim in the first year or two after switching.

What is the difference between replacement cost and actual cash value for retirees?

Replacement cost pays to rebuild or repair your home at current prices. Actual cash value pays that amount minus depreciation, so a 20-year-old roof that costs $15,000 to replace might only pay out $6,000 under ACV. For most retirees who plan to stay in their home, replacement cost coverage is worth the higher premium. ACV may be a rational choice only for retirees with a clear plan to relocate after a total loss and enough liquid assets to bridge any payout gap.

Can retirees get homeowners insurance through AARP?

AARP partners with The Hartford to offer homeowners insurance to members age 50 and older. Members who bundle home and auto with The Hartford save an average of $963 per year. Coverage terms and availability vary by state, so eligibility should be confirmed directly with The Hartford or through the AARP insurance portal.

What should I do if my insurer raises my premium significantly at renewal?

Request a written explanation for the increase, then shop competing quotes at the identical coverage level before renewing. Also ask your current carrier whether any new discounts apply, home improvements, an extended claims-free period, or a better credit score can all shift your rate. If standard market options become unaffordable in your area due to climate risk, contact your state insurance department about the FAIR Plan as a last-resort alternative.

Sources

- U.S. Census Bureau, Property Insurance Costs in the United States (2025)

- Texas Department of Insurance, Texas Homeowners Insurance Market Overview (2025)

- Texas Department of Insurance, Lower Your Home Insurance by Asking for Discounts

- California Department of Insurance, Shopping for Residential Insurance: Seniors

- Utah Insurance Department, Saving on Homeowners Insurance

- New York State Department of Financial Services, Consumer Insurance Discounts and Savings

- Illinois Department of Insurance, Homeowner and Renter Insurance Shopping Tips

- Smart Insurance 101, Homeowners Insurance Guide: A Beginner’s Overview

- Smart Insurance 101, How to Save Money on Your Homeowners Insurance