Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

Insurance companies use your claims history at renewal by pulling CLUE or A-PLUS reports covering up to 7 years of past claims, then applying rate surcharges, stripping no-claims discounts, reclassifying you into higher-risk tiers, adding policy exclusions, or declining to renew altogether. A single claim on a homeowners policy can raise your annual premium by more than $260, and the effects typically persist across 3 to 5 renewal cycles.

Your claims history at renewal is one of the most powerful pricing inputs an insurer has, and most policyholders don’t realize how much detail carriers can access or how long those records follow them. A claim you filed three years ago can still push your premium higher today, reset discounts you spent years earning, or quietly move you into a more expensive risk tier without any direct explanation from your insurer. According to the Texas Department of Insurance, insurers use claims history to decide both whether to sell you a policy and what to charge you.

This matters more right now because insurers across the country are tightening underwriting standards. As detailed in our article on why insurance premiums are exploding, carriers are using every available data point to manage rising loss costs. Claims history has become a sharper input in that process, especially as databases like CLUE grow more detailed and renewal algorithms grow more automated.

This guide breaks down exactly what insurers do with your claims record at each renewal, why even small or not-at-fault claims count, and what you can do to limit the damage. If you’re reviewing a renewal notice or thinking through a claim you haven’t filed yet, understanding these mechanics puts you in a much stronger position.

Key Takeaways

- Insurers access your claims record through CLUE or A-PLUS reports containing up to 7 years of personal auto and property claims history, according to the Washington State Office of the Insurance Commissioner.

- A single homeowners claim raises the average annual premium from $2,490 to $2,750, a difference of $260 per year, according to NerdWallet’s 2026 homeowners insurance data.

- Claims history is a key factor insurers consider when setting premiums for auto and home coverage, according to the National Association of Insurance Commissioners (NAIC).

- Even not-at-fault claims are factored into renewal pricing because insurers’ own data shows they correlate with higher overall risk profiles across future policy periods.

- Multiple small claims, for example, three $5,000 claims in a single year, commonly trigger non-renewal or major premium spikes, while a single catastrophic weather event often does not.

- The CLUE database maintained by LexisNexis tracks up to 5 to 7 years of claims data, and you are entitled to one free report per year to check for errors that may be inflating your renewal rate, per the Utah Insurance Department.

In This Guide

- Step 1: How Insurers Track and Access Your Claims History at Renewal

- Step 2: Rate Surcharges and Premium Hikes Tied Directly to Claims

- Step 3: Loss of No-Claims Discounts

- Step 4: Reclassification into Higher-Risk Pricing Tiers

- Step 5: Policy Restrictions, Exclusions, or Higher Deductibles at Renewal

- Step 6: Non-Renewal or Conditional Renewal Decisions

- Frequently Asked Questions

Step 1: How Insurers Track and Access Your Claims History at Renewal

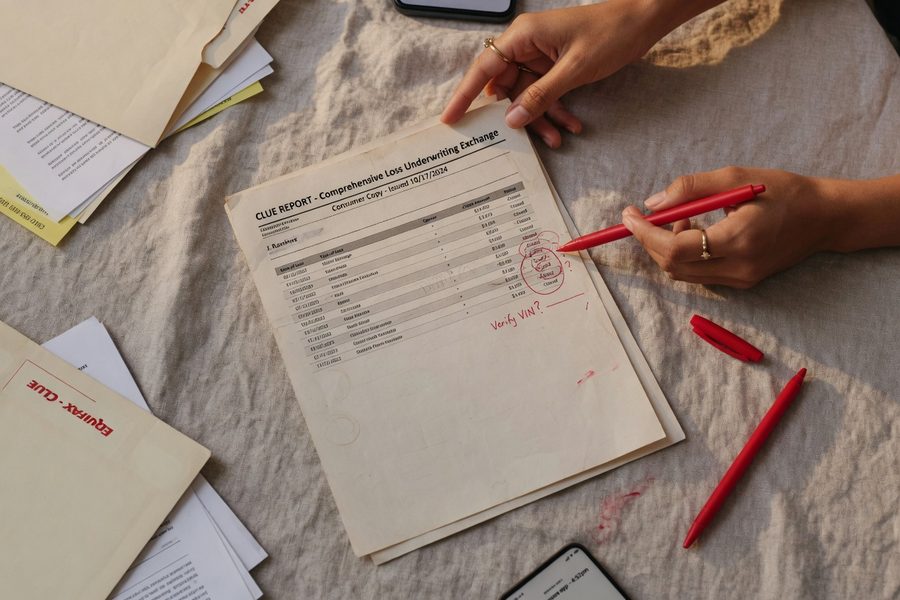

Before an insurer quotes your renewal, it pulls your claims record from at least one centralized database, and that record is far more detailed than most people expect. The two dominant systems are the CLUE report (Comprehensive Loss Underwriting Exchange), maintained by LexisNexis, and the A-PLUS report (Automated Property Loss Underwriting System), maintained by Verisk Analytics. Both aggregate claims data submitted by carriers and make it available to other insurers during underwriting. LexisNexis and Verisk function as the credit bureaus of the insurance world, except that, unlike Experian or Equifax, they operate almost entirely outside the average policyholder’s awareness.

What These Reports Actually Contain

A CLUE report includes the date of each claim, the type of loss, the amount paid, and whether the claim was closed or still open. For homeowners coverage, the Utah Insurance Department confirms the database retains up to five years of personal property claims history, while the Washington State Office of the Insurance Commissioner notes that auto claims can persist in CLUE for up to seven years. A-PLUS covers commercial and personal lines property claims on a similar timeline.

Insurers also maintain their own internal claims records. So even if a claim ages out of CLUE, your current carrier may still have it on file from prior renewal cycles. During the renewal underwriting review, the carrier’s system typically runs an automatic data pull, often 30 to 60 days before your policy’s expiration date, and re-scores your risk profile before issuing the renewal offer.

Your Right to Review and Correct These Records

Under the federal Fair Credit Reporting Act (FCRA), you are entitled to request one free CLUE report per year from LexisNexis. The FCRA gives consumers dispute rights over any consumer reporting agency, and LexisNexis qualifies as one under that definition. If you find an error, a claim incorrectly attributed to your property, an inflated payout amount, or a claim that belongs to a prior owner, you can file a dispute directly with LexisNexis. Confirmed errors must be corrected, and an updated report can directly lower a renewal quote. The process typically takes 30 days.

One limitation worth naming: the FCRA dispute process is designed for clear factual errors, not subjective disagreements about how a claim was categorized. If LexisNexis accurately recorded a claim your carrier submitted, disputing it will not succeed. The tool works best when the data itself is wrong, not merely unflattering.

Request your free CLUE report before your renewal date, not after. If you spot an error and dispute it successfully, you may be able to ask your insurer to re-rate your policy with the corrected data before the new premium takes effect.

Step 2: How Does Your Insurance Claims History Affect Renewal Rates?

Filing a claim almost always costs you more at renewal, even when the claim isn’t your fault. The surcharge is actuarial, not punitive. Insurers, using historical loss data from sources like the NAIC and proprietary modeling from Verisk, have established that policyholders who file at least one claim are statistically more likely to file another, regardless of what caused the first loss.

The Dollar Impact of a Single Claim

The math is concrete. A sample homeowners policy with no claims costs an average of $2,490 per year. After a single claim, that same policy averages $2,750 per year, a difference of $260 annually, according to NerdWallet’s 2026 homeowners insurance cost data. That’s a roughly 10% increase for one claim. Over three renewal cycles, the most common window before claims effects start to diminish, that single claim could cost you $780 in extra premiums before the surcharge fades.

For auto insurance, surcharges are typically steeper and directly tied to fault. An at-fault accident routinely adds 20% to 40% to the renewal premium in most states, while a not-at-fault claim may still add 5% to 15% depending on the carrier and state regulations. California prohibits surcharges for not-at-fault claims under rules enforced by the California Department of Insurance, but most states do not impose that restriction.

Why Small Claims Often Hurt Disproportionately

A $900 water damage claim and a $15,000 roof replacement claim may trigger the same tier reassignment in your insurer’s renewal model. What matters most is claim frequency, not just severity. Two claims in three years often triggers a larger surcharge than one large claim, because frequency signals habitual risk in the actuarial models carriers buy from firms like Verisk and ISO (Insurance Services Office). This is a genuine trap: a policyholder who files for two small losses in quick succession can face a bigger renewal penalty than someone who had one major covered event.

The average homeowners insurance premium jumps from $2,490 to $2,750 after a single claim, a $260 annual surcharge that typically persists for 3 to 5 renewal cycles. Source: NerdWallet, 2026.

Step 3: Loss of No-Claims Discounts

A claims-free discount isn’t just a reward for clean history, it’s a pricing tier you lose the moment a claim appears on your record. Most insurers offer discounts ranging from 5% to 20% for consecutive claim-free years, and some programs grant progressively larger credits after three, five, or even ten years without a loss. One filed claim resets that counter to zero.

The compounding effect is what catches most policyholders off guard. Suppose you’ve accumulated a 15% claims-free discount after five years. A small water leak claim doesn’t just add a surcharge to your renewal, it also strips that 15% discount simultaneously. The net swing on your premium can easily exceed 25% in a single renewal cycle, combining the surcharge addition with the discount removal. Reinstatement timelines vary by carrier, but most require two to three consecutive claim-free years before any discount credit begins rebuilding.

Some carriers advertise “claim forgiveness” programs that protect your discount after a first claim, but read the fine print carefully. Many of these programs only apply to your first claim ever with that specific carrier, and eligibility often requires three or more prior claim-free years on the same policy.

Step 4: Reclassification into Higher-Risk Pricing Tiers

Rate surcharges and discount losses operate on top of your existing pricing tier. Tier reclassification is a separate, often more damaging consequence, one that many policyholders miss because it doesn’t show up as a line-item explanation on the renewal declaration page.

Preferred, Standard, and Non-Standard Markets

Most personal lines insurers segment their book of business into three broad pricing tiers: preferred (lowest rates, best risk profiles), standard (average rates, moderate risk), and non-standard (highest rates, higher-risk policyholders). A clean history keeps you in the preferred tier. Multiple claims, or sometimes even a single severe loss, can move you from preferred to standard, or from standard to non-standard. The non-standard market, often served by specialty carriers rather than mainstream names like State Farm or Allstate, can run 30% to 50% more expensive than standard-market equivalents for the same coverage.

This is also where your FICO Score can interact with claims history in ways that amplify the damage. Many states permit insurers to use credit-based insurance scores, derived partly from FICO data, alongside claims history in renewal pricing. A policyholder who has both a claims event and a recent credit deterioration may face compounding tier pressure. The National Association of Insurance Commissioners (NAIC) has documented this practice, and several state insurance departments are actively reviewing its fairness under consumer protection frameworks.

The Role of Experience Modification Factors in Commercial Lines

For small business owners, the stakes are even higher. Commercial auto and general liability policies use an experience modification factor (EMR) that adjusts your premium up or down based on actual claims versus expected claims for your industry class, as defined by ISO classification codes. A high-claims year can push your EMR above 1.0, triggering surcharges that follow you for three years. If you’re a business owner reviewing your commercial policy, our guide on what commercial insurance covers walks through how EMRs work in more detail.

LexisNexis Active Insights: Post-Binding Monitoring

One detail most competitors miss: LexisNexis offers insurers a product called Active Insights, which flags newly reported claims on existing policyholders between renewal cycles. Your insurer doesn’t have to wait until renewal to learn about a claim you filed. Some carriers use this monitoring to initiate mid-term rating reviews or to flag accounts for more aggressive renewal scrutiny. You may receive a renewal offer that looks pre-decided, because, in a sense, it was.

Not-at-fault auto claims are factored into renewal pricing by many carriers because actuarial data consistently shows they predict higher overall loss frequency. The reasoning: drivers who are struck repeatedly may have driving patterns or locations that increase exposure, regardless of legal fault.

Step 5: What Kinds of Policy Restrictions Can Insurers Add at Renewal?

Beyond rate increases, insurers have a second lever at renewal: they can change what the policy covers. A claim on a specific peril is often used as justification for excluding or limiting that peril going forward.

Claim-Specific Exclusions and Reduced Limits

Filed a claim for water backup damage? Your renewal may include a new exclusion for that exact cause of loss, or your water backup sublimit may be cut from $10,000 to $5,000. Filed a dog bite liability claim? Some carriers add a specific-breed exclusion or remove animal liability coverage entirely at renewal. These changes are disclosed in the renewal offer documents, but the language is dense enough that many policyholders miss them until they need to file again.

Multiple claims within a short window accelerate this process. A policyholder with three claims in two years may find their renewal offer comes with a significantly higher deductible, say, $2,500 instead of $1,000, as the carrier’s way of reducing exposure while technically keeping the policy in force. Higher deductibles reduce the insurer’s frequency risk without requiring a formal non-renewal notice, which in many states demands advance written notice and more regulatory documentation.

How to Spot These Changes Before Accepting Renewal

Always compare the renewal declarations page and policy endorsements side-by-side with your current documents. Look specifically for new exclusion endorsements, changes to sublimits, and deductible modifications. If coverage has been materially reduced, you are effectively paying a similar premium for less protection, and shopping for a new carrier makes financial sense. Our guide to saving money on homeowners insurance covers how to evaluate competing renewal offers efficiently.

Ask your insurer directly whether any new exclusions or endorsements were added to your renewal. Agents are required to explain material coverage changes. If you got a form-letter renewal packet without explanation, call and ask, you may uncover a restriction the carrier hoped would go unnoticed.

Step 6: Non-Renewal or Conditional Renewal Decisions

Non-renewal is the most drastic tool in the insurer’s kit. Most carriers will not non-renew a policy after a single claim, but thresholds vary significantly by company, coverage type, and state.

What Triggers Non-Renewal

In personal lines, two or three claims within a 36-month window is a common threshold for non-renewal review. The mix matters. Three small claims in one year often draws more scrutiny than two larger claims spread over several years, for the same frequency-signals-risk logic described in Step 2. As the National Association of Insurance Commissioners (NAIC) notes, claims history is a primary factor in both renewal pricing and renewal decisions.

State regulations add important constraints. Most states require insurers to provide written notice of non-renewal 30 to 60 days before the policy expires. California and Florida place additional restrictions on non-renewals in high-wildfire or high-hurricane-risk areas, with the California Department of Insurance and Florida’s Office of Insurance Regulation each enforcing specific notice and justification requirements. Even so, carriers have found ways to work around these limits, for example, by declining to offer renewal in an entire ZIP code rather than selecting individual policyholders, which triggers different regulatory scrutiny thresholds.

Options When You’re Facing Non-Renewal

If your carrier declines to renew, your first move should be to request the specific reason in writing. You have the right to this explanation in most states, and it tells you what a new carrier will also see. From there, independent brokers who work with multiple carriers are your best resource, they can match your risk profile to carriers that specialize in accounts with claims history. Usage-based programs and telematics for auto insurance can also help rebuild a favorable record. And for a broader sense of where to start rebuilding coverage, our overview of working with an insurance broker is worth reading before you start calling around.

One honest concession worth making: not all non-renewals stem from abuse or excessive claims. A single large weather-related loss that is demonstrably catastrophic and regional, a tornado, a wildfire, a named storm, often carries less renewal stigma than a pattern of smaller attritional losses. Insurers distinguish between correlated catastrophe losses (which affect everyone in the area) and idiosyncratic losses (which reflect individual risk patterns). If your claims history involves one major weather event, you have more negotiating room than the raw claim count suggests.

There is also a harder truth for policyholders in very high-risk geographies. If you are in a coastal Florida ZIP code or a high-wildfire-probability area in California, claims history may be almost beside the point. Carriers like Citizens Property Insurance Corporation in Florida exist precisely because the standard market has withdrawn from those areas regardless of individual claims records. No amount of clean history fully insulates you when a carrier decides a geography itself is uninsurable at a viable premium.

| Insurer Action at Renewal | Typical Trigger | Estimated Cost Impact | How Long It Lasts |

|---|---|---|---|

| Rate Surcharge | 1 or more claims in the lookback window | 5%–40% premium increase | 3–5 renewal cycles |

| No-Claims Discount Removal | Any claim filed, regardless of fault | 5%–20% discount loss | 2–3 years to rebuild |

| Tier Reclassification | Multiple claims or severe single loss | 30%–50% above standard rates | 3–7 years depending on carrier |

| Coverage Exclusion or Deductible Increase | Claim on a specific peril, or 2+ claims | Reduced coverage value; higher out-of-pocket | Varies; may be permanent unless renegotiated |

| Non-Renewal | 3+ claims in 36 months; or pattern of high-cost losses | Forced to surplus/non-standard market | Until claims age off CLUE (up to 7 years) |

The table above summarizes the five mechanisms in order of severity. In practice, insurers rarely skip to non-renewal without first cycling through surcharges and coverage restrictions. The exceptions are fraud investigations and cases where a single catastrophic loss exceeds the carrier’s risk appetite for that property type or geography.

Frequently Asked Questions

How many claims does it take before my insurer won’t renew my policy?

Most personal lines insurers review accounts with two or more claims within a 36-month period, and three claims in that window frequently triggers a non-renewal recommendation. The exact threshold depends on the carrier, the claim types, and your state’s regulatory environment. Frequency matters more than dollar amount, three $3,000 claims in one year is riskier in an insurer’s model than a single $20,000 claim.

Does a not-at-fault car accident still raise my renewal premium?

Yes, in most states. While the California Department of Insurance prohibits surcharges for not-at-fault claims, the majority of states permit carriers to factor them into renewal pricing. Insurers justify this by pointing to actuarial data showing that drivers involved in not-at-fault accidents have statistically higher future loss rates, likely due to driving environment or behavior patterns rather than legal fault.

How do I find out what’s in my CLUE report before my renewal?

Request your free annual CLUE report directly from LexisNexis at their consumer disclosure website. You’re entitled to one free report per year under the Fair Credit Reporting Act (FCRA). Review it for errors, misattributed claims, inflated payout amounts, or claims from a prior property owner are common issues. Dispute any inaccuracies in writing; corrections typically take 30 days and must be reflected in any subsequent insurance quotes.

Can I dispute a renewal rate increase if my claims history in CLUE is wrong?

Disputing an error in your CLUE report can directly change a renewal quote. Once LexisNexis corrects a verified error, you can ask your insurer to re-rate your policy based on the updated data. Some carriers will do this proactively; others require you to submit the corrected report yourself along with a written request. If your insurer refuses to adjust the rate after a confirmed correction, that’s grounds to shop for a new carrier and use the corrected report in those conversations.

How long does a claim stay on my record and affect my insurance renewal?

Claims typically remain in CLUE for five to seven years, as confirmed by the Utah Insurance Department. The impact on renewal pricing is strongest in the first one to three cycles after a claim, then fades as the loss ages. By the time a claim is four or five years old, most carriers weight it significantly less in their renewal models, though it remains visible in the database until it drops off.

Is it ever worth not filing a small claim to protect my renewal rate?

Often, yes. If a repair estimate is close to your deductible, or only modestly above it, paying out of pocket preserves your claims-free discount and avoids the surcharge cycle. Use the worked math as a guide: if filing saves you $800 today but costs you $260 in extra annual premiums plus 15% in lost discounts for three years, the net is negative. Run the numbers before calling your insurer, and remember that even an inquiry about a potential claim can be logged in some carrier systems. For more on managing your home insurance costs, see our guide to getting the best home insurance coverage.

Do insurance companies share claims history with each other?

Not directly, but they share it indirectly through CLUE and A-PLUS. Every claim submitted to your current carrier is reported to one or both databases maintained by LexisNexis and Verisk Analytics, and any carrier you apply to in the future will pull those reports during their underwriting review. This is why switching insurers doesn’t reset your claims history, the new carrier sees the same record your old one used.

What’s the difference between a renewal underwriting review and a new business review for the same claims history?

New business underwriting is generally stricter. Carriers have more flexibility to decline new applications outright than to non-renew existing policyholders, who are protected by state notice requirements and, in some cases, restrictions on grounds for non-renewal enforced by regulators like the California Department of Insurance or Florida’s Office of Insurance Regulation. A claims history that might prevent you from getting a new policy with a given carrier might still result in a conditional renewal, with higher rates or reduced coverage, with your current insurer. This is one reason why staying with a carrier through a claims period, even at a higher rate, can be strategically smarter than switching immediately.

Sources

- Washington State Office of the Insurance Commissioner, CLUE: Comprehensive Loss Underwriting Exchange

- Texas Department of Insurance, Will My Premium Go Up If I File a Claim?

- National Association of Insurance Commissioners (NAIC), Why Are My Insurance Premiums Increasing?

- Utah Insurance Department, CLUE Consumer Information

- NerdWallet, Average Homeowners Insurance Cost (2026)

- Smart Insurance 101, Insurance Premiums Are Exploding: Here’s Why

- Smart Insurance 101, How to Save Money on Your Homeowners Insurance

- Smart Insurance 101, Choosing an Insurance Broker Could Save You Time and Money

- Smart Insurance 101, Ways to Get the Best Home Insurance Coverage and Save Money