Fact-checked by the Smart Insurance 101 editorial team

Burglary claims are among the most contested in residential insurance, and the numbers reveal why: the average homeowners insurance burglary payout sits at roughly $5,524 per theft claim, according to Insurance Information Institute data spanning 2019–2023. That figure sounds reassuring until you factor in a $1,500 deductible, a $1,000 jewelry sublimit, and an adjuster who prices your stolen 4K television at its depreciated value rather than what a replacement costs today. The gap between what was taken and what the insurer deposits into your account can be substantial.

Theft accounts for just 0.6% of total homeowners insurance losses in 2023, yet the 193,030 theft claims filed nationwide that year represent real households discovering exactly how their policies perform under pressure. Most policyholders carry personal property coverage set at 50–70% of their dwelling limit, but special sublimits for jewelry, cash, and firearms can cap a room-specific payout far below that ceiling. The result is a claim that looks generous on paper and disappointing in practice.

This guide breaks down what your policy actually pays after a burglary, organized by room, so you can see precisely where sublimits bite, how valuation methods change your check, and what documentation steps determine whether you collect close to your full loss or settle for a fraction of it.

Key Takeaways

- The weighted average theft claim payout from 2019–2023 was $5,524, but your net recovery drops significantly after your deductible is subtracted.

- Personal property limits typically run 50–70% of dwelling coverage; on a $300,000 home, that means $150,000–$210,000 in total personal property protection, but item-specific sublimits can override that ceiling.

- Jewelry and cash sublimits are commonly capped at $1,000–$1,500 per occurrence across major carriers, meaning a $5,000 ring stolen from your bedroom may yield less than $500 after your deductible.

- Actual cash value (ACV) settlements apply depreciation before paying; replacement cost value (RCV) policies pay full replacement cost but only after you provide proof of purchase.

- Theft claims face higher adjuster scrutiny than weather or fire claims, particularly for high-value portable items in bedrooms, home offices, and garages.

- Adding a scheduled personal property endorsement for jewelry or collectibles can cost as little as $20–$40 per year per $1,000 of coverage and eliminates sublimit exposure entirely.

In This Guide

- Does Homeowners Insurance Cover Burglary and Theft?

- How Limits, Deductibles, and Valuation Methods Shape Your Payout

- Living Room and Family Areas: What Insurance Typically Replaces

- Kitchen and Utility Spaces: Appliances, Small Electronics, and Everyday Items

- Bedrooms and Closets: Clothing, Jewelry, and Personal Valuables

- Home Office, Garage, and Other Spaces: Tech, Tools, and Special Items

- State Variations and Policy Differences That Affect Your Claim

- Filing the Claim and Getting Paid: Room-by-Room Documentation Strategies

Does Homeowners Insurance Cover Burglary and Theft?

The short answer is yes, with conditions. A standard HO-3 policy covers theft as a named peril under personal property coverage. The Texas Department of Insurance confirms that personal property coverage pays if your furniture, clothing, and other things you own are stolen, damaged, or destroyed, with theft explicitly listed among covered perils. That applies whether a thief takes your television, forces open a window, or damages your door frame on the way in.

Coverage splits across two buckets. Personal property coverage replaces stolen items. Dwelling coverage pays for structural damage, broken doors, shattered windows, damaged locks, caused during the break-in. Both buckets are subject to your deductible, and both have their own limits. Many homeowners focus only on the stolen items and overlook the structural repair component, which can add $500–$2,000 to a single claim.

Common Exclusions That Reduce Burglary Claims

Not every theft scenario triggers a full payout. Policies routinely exclude or limit theft from vacant homes, typically defined as unoccupied for 30–60 consecutive days depending on the carrier. If you left a property vacant and a burglar entered, your insurer may deny the personal property claim outright. Shoplifting, mysterious disappearance (where you cannot prove theft occurred), and employee theft are also excluded under most standard policies.

Off-premises theft coverage is standard in HO-3 policies but limited. Items stolen from your car, a hotel room, or a storage unit typically receive only 10% of your personal property limit. On a policy with $150,000 in personal property coverage, that’s $15,000 in off-premises protection, which sounds adequate until you realize sublimits for jewelry and cash apply within that 10% cap simultaneously.

Theft claims represent only 0.12 claims per 100 policies annually (2019–2023 weighted average), according to Insurance Information Institute data, but when a theft claim is filed, the average payout of $5,524 makes it one of the costlier personal property claim categories per incident.

HO-3 vs. HO-5: How Policy Form Changes Your Recovery

An HO-5 policy offers broader personal property protection. Where HO-3 covers personal property on a named-perils basis, HO-5 covers it on an open-perils basis, meaning theft is covered unless specifically excluded rather than only if specifically listed. HO-5 policies also tend to default to replacement cost value rather than actual cash value for contents, which meaningfully changes your payout on depreciated items like electronics and clothing. The premium difference between HO-3 and HO-5 is typically $100–$300 per year, a trade-off worth evaluating if you carry significant portable valuables. You can explore how different homeowners policies compare in the Homeowners Insurance Guide: A Beginner’s Overview.

How Limits, Deductibles, and Valuation Methods Shape Your Payout

Three variables control every burglary payout: your personal property limit, your deductible, and whether your policy settles on an actual cash value (ACV) or replacement cost value (RCV) basis. Understanding how they interact matters far more before a claim than after.

Personal property limits are not arbitrary. Most carriers set them at 50–70% of your dwelling coverage. On a home insured for $400,000, that means $200,000–$280,000 in personal property protection. The catch: sublimits for specific item categories sit inside that larger number and cap payouts regardless of the overall limit’s size.

Actual Cash Value vs. Replacement Cost Value

The valuation method your policy uses affects your payout far more than most people expect. Under ACV, the insurer pays what your stolen items were worth at the time of theft, accounting for age, condition, and depreciation. A laptop you bought for $1,200 three years ago might be valued at $480 under ACV. Under RCV, the insurer pays what a comparable new item costs today, that same laptop might be worth $1,100 as a replacement. The difference is $620 on a single item.

There is a timing wrinkle with RCV policies that catches many claimants off guard. Most carriers pay the ACV amount initially, then release the remaining depreciation holdback only after you provide proof that you purchased a replacement. If you cannot afford to replace the item immediately, you may only receive the ACV amount. This structure is standard practice across major carriers, not a carrier trick, but knowing it in advance helps you plan the claim strategically.

The weighted average theft claim payout from 2019–2023 was $5,524. With a typical $1,500 deductible, the net check to the policyholder averages closer to $4,024, and that assumes no sublimits apply to the stolen items.

Special Sublimits by Item Category

Sublimits are where the real complexity lives. Most HO-3 policies impose per-occurrence caps on the following categories regardless of your overall personal property limit:

| Item Category | Typical Sublimit | Coverage Tip |

|---|---|---|

| Jewelry, watches, furs | $1,000–$1,500 | Schedule valuable pieces separately |

| Cash, coins, gift cards | $200–$500 | Rarely worth claiming alone |

| Firearms | $2,500 | Endorsement available from most carriers |

| Securities, manuscripts | $1,000–$2,500 | Document originals; digital backups help |

| Business property on premises | $2,500 | Home-based business endorsement may apply |

| Electronic data | $0–$1,000 | Hardware replacement covered; data recovery varies |

The Virginia State Corporation Commission notes that homeowners policies provide limited coverage for personal property with specific sublimits for items like jewelry, furs, cash, and securities. Those sublimits are not disclosed prominently in marketing materials; they appear in the policy declarations and definitions sections that most homeowners skip entirely.

Living Room and Family Areas: What Insurance Typically Replaces

The living room is the most common target for burglars: televisions, gaming consoles, and speakers are portable, high-value, and easy to resell. The good news is that electronics and furniture generally fall outside the category-specific sublimits that cap jewelry or cash. A stolen 65-inch OLED television worth $1,800 is covered under your general personal property limit with no separate sublimit applying.

The challenge in living room claims is depreciation. Under an ACV policy, a three-year-old 65-inch TV that cost $1,800 might be valued at $900 after depreciation. A $1,500 deductible would reduce your payout to $0 on that item alone. This is the scenario that makes RCV coverage worth its modest premium, and explains why many homeowners with significant electronics holdings should review their valuation method before a claim occurs.

Structural Damage from Entry Points

Burglars typically enter through front doors, sliding glass doors, and windows, all components of the dwelling structure, not personal property. Replacement of a kicked-in front door runs $800–$1,500 for materials and labor in most markets as of early 2026. A broken sliding glass door can run $1,200–$3,000. This structural damage is covered under your dwelling coverage, separate from personal property, and subject to the same deductible. If your single deductible applies to both coverages combined on one claim (which varies by carrier), the structural repair may consume most of it before your personal property loss is calculated.

After a burglary, photograph all points of entry before repairs begin and get written estimates from two contractors. Adjusters use standardized pricing databases that can undervalue regional labor costs; a competing estimate gives you documented grounds to negotiate the structural repair component upward.

Documentation Realities for Living Room Items

Proving ownership and value for living room electronics is typically straightforward. Serial numbers are often registered with manufacturers, and purchase receipts or credit card statements, from institutions like Chase, Bank of America, or any major bank, establish cost. Where claims stall is with decorative artwork or high-end audio equipment without registered serial numbers. If an adjuster cannot verify ownership through records, they may dispute or discount the item. A home inventory video that shows these items, with price tags or purchase documentation visible, resolves that dispute before it starts.

Kitchen and Utility Spaces: Appliances, Small Electronics, and Everyday Items

Kitchens and utility rooms are rarely primary targets in residential burglaries, major appliances are too heavy to carry, and most thieves move quickly. But kitchens do get hit for small electronics: tablets left on countertops, smart displays, and portable speakers. These items fall under general personal property coverage with no category-specific sublimits, which works in your favor.

Depreciation still applies under ACV policies. A $600 espresso machine purchased two years ago might be valued at $360 under ACV schedules. Under RCV, the insurer would owe $600 (or the current replacement cost, which may be higher due to inflation). The practical math: if your deductible is $1,500 and the only items stolen from the kitchen total $900 after depreciation, this portion of the claim nets you nothing on its own. Burglary claims are almost always whole-house events, however, so kitchen losses combine with losses from other rooms toward your total claim.

Forced Entry Damage in Kitchen and Utility Areas

Back doors and garage entry doors are common break-in points for kitchen-adjacent rooms. Damage to these structures, including door frames, deadbolts, and connected security hardware, is covered under dwelling coverage. Temporary boarding or emergency locksmith services are generally reimbursable as well, though carriers vary on how they classify emergency security expenses. Keep every receipt from the first 48 hours after a break-in.

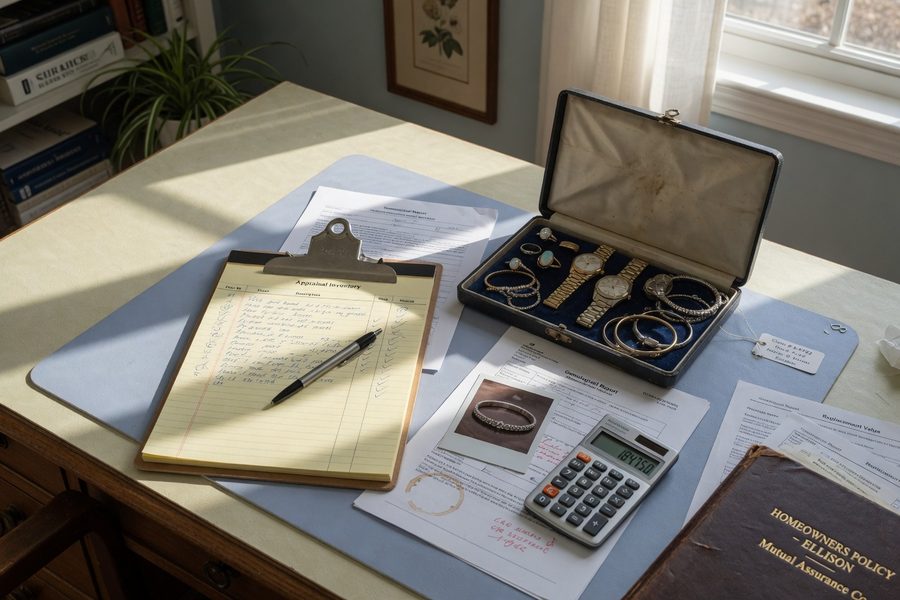

Bedrooms and Closets: Clothing, Jewelry, and Personal Valuables

This is where the gap between policyholder expectations and actual payouts is widest. Bedrooms and closets hold the highest concentration of sublimit-affected items: jewelry, watches, and cash. A master bedroom burglary involving a $4,000 ring, $2,500 in cash, and a $1,200 watch has a theoretical combined value of $7,700, but standard sublimits cap the jewelry at $1,500 and the cash at $200, for a maximum recoverable value of $2,900. After a $1,500 deductible, that’s a net payout of $1,400 on $7,700 in losses. That math is not hypothetical; it is the structure of most standard HO-3 policies.

The National Association of Insurance Commissioners (NAIC) confirms in its consumer guide that homeowners insurance reimburses for damage to property caused by covered perils such as fire or theft, but the NAIC also notes that sublimits and policy conditions govern what specific items actually pay. Many policyholders discover these sublimits only when they file a bedroom-specific claim and receive a check that bears little resemblance to their loss.

Jewelry and cash sublimits are per-occurrence, not per-item. If three rings, two necklaces, and $500 in cash are stolen in a single event, the entire jewelry group is capped at $1,000–$1,500 total, not $1,000–$1,500 per piece. This is one of the most frequently misunderstood limits in residential insurance.

Clothing and Linens: The Overlooked Loss

Clothing is personal property and is covered without a special sublimit, but ACV depreciation hits clothing hard. A wardrobe of 30 items totaling $6,000 in original purchase price might be valued at $2,000–$3,000 under ACV, depending on age. Luxury brands hold value better in ACV calculations because insurers reference resale market values, not just age-based depreciation schedules. Documenting clothing with brand names, purchase years, and approximate original cost in a room-by-room inventory makes a meaningful difference in what an adjuster can approve.

Scheduling Jewelry and High-Value Valuables

A scheduled personal property endorsement, sometimes called a floater, removes the standard sublimit and provides agreed-value coverage for specific items. Cost is typically $1–$2 per $100 of coverage annually, meaning a $5,000 ring costs roughly $50–$100 per year to schedule. The endorsement also eliminates the deductible for covered scheduled items under most carriers’ terms, a benefit that can exceed the premium savings many times over on a single claim. For anyone with engagement rings, heirloom jewelry, or a watch collection, scheduling is a baseline requirement, not an optional upgrade.

Home Office, Garage, and Other Spaces: Tech, Tools, and Special Items

Home offices and garages present a different set of coverage complications. The items stored there, computers, professional tools, hobby equipment, outdoor power tools, often sit at the intersection of personal and business property, and that distinction matters enormously to how a claim is settled.

Business Equipment Sublimits

Standard HO-3 policies cap business property kept at the residence at $2,500. If you work from home and have a $3,500 professional workstation and a $1,200 external monitor array, the total covered loss is still capped at $2,500 regardless of your policy’s overall personal property limit. A home-based business endorsement or a separate business property policy removes that cap. The National Association of Insurance Commissioners recommends that self-employed workers review this gap specifically, since standard homeowners forms were not designed to cover commercial equipment. If you are self-employed or run a side business from home, this gap deserves immediate attention.

Personal computers used solely for non-business purposes are covered under general personal property with no separate sublimit under most carriers. The distinction is how the insurer classifies primary use. If you work remotely for an employer and the laptop is employer-owned, it is not covered under your homeowners policy at all, it belongs to your employer’s commercial property policy.

Garage Contents and Off-Premises Limits

Tools and equipment stored in an attached garage are covered under standard personal property limits. Detached garages and sheds are typically covered under other structures coverage, usually set at 10% of dwelling coverage. Contents inside detached structures follow the same personal property rules, but some carriers apply a combined sublimit for other-structures contents that can cap the payout below the general personal property ceiling. State insurance departments, including those in Florida, Texas, and California, set minimum other-structures coverage thresholds differently, and some leave it entirely to carrier discretion. Items stored in a rented storage unit off-premises face the 10% off-premises sublimit discussed earlier.

Vehicles parked in a garage are not covered under homeowners insurance for theft of the vehicle itself, that falls under your auto policy’s comprehensive coverage. Items stolen from inside the vehicle, however, may be covered under your homeowners policy’s off-premises theft provision, subject to sublimits.

Collectibles, Hobby Items, and Specialty Equipment

Baseball card collections, vintage guitars, and camera bodies occupy an uncomfortable middle ground in theft claims. They are personal property, technically covered, but their values are difficult to document without appraisals or market-price evidence. Insurers routinely dispute valuations for collectibles without third-party appraisals on file. An annual appraisal update for any collection worth more than $2,000–$3,000 is essential documentation, not a luxury. Specialty insurance providers such as Collectibles Insurance Services or American Collectors Insurance offer standalone policies for these items that carry higher agreed-value limits than any standard HO-3 sublimit allows.

State Variations and Policy Differences That Affect Your Claim

Not all homeowners insurance burglary payout outcomes are equal across state lines. Some states mandate minimum personal property sublimits or restrict how carriers can apply depreciation schedules; others leave policy terms almost entirely to insurer discretion. The Illinois Department of Insurance describes homeowners insurance as “a financial protection policy that pays a lump sum if your house is damaged or destroyed by fire, weather, theft or other disasters”, but the size of that lump sum varies by state regulation as much as by policy type.

Florida, California, and Texas have seen significant policy language changes from major carriers between 2024 and 2026 in response to broader insurance market pressure. State insurance regulators, including the Florida Office of Insurance Regulation and the California Department of Insurance, have fielded increasing consumer complaints about carriers quietly raising jewelry sublimits from $1,000 to $1,500 while simultaneously tightening documentation requirements for claims above $3,000. Reading your current declarations page annually, not just at renewal, is the only way to catch these shifts. If you want more background on why insurance costs and terms have been shifting, the article on why insurance premiums are exploding explains the market forces driving these changes.

Filing the Claim and Getting Paid: Room-by-Room Documentation Strategies

How you document a burglary claim directly determines what you collect. Theft claims face higher scrutiny than fire or weather claims because ownership and value are more easily disputed. Adjusters for theft claims routinely ask for purchase receipts, serial numbers, and warranty registrations, and they ask for all of it per item, not per room.

The process starts before you call your insurer. File a police report first. Every homeowners policy requires a police report as a condition of theft claim payment; skipping this step can result in a denial. Request a copy of the report number immediately and the full report once available. Your insurer will request both.

Room-by-Room Inventory Documentation

Work through each room systematically after the police report is filed. For each stolen item, document: item description, brand and model, approximate purchase date, original purchase price, and current replacement cost (a quick online search for comparable models). Where you have photos, from social media, listing apps, or home videos, pull them. Serial numbers registered with manufacturers can be verified electronically by adjusters and eliminate ownership disputes entirely.

| Room | Key Items to Document | Documentation Priority |

|---|---|---|

| Living Room | TVs, consoles, speakers, art | Serial numbers, receipts, photos |

| Master Bedroom | Jewelry, watches, cash, laptops | Appraisals, photos with items worn, receipts |

| Home Office | Computers, monitors, peripherals | Serial numbers, purchase invoices |

| Garage | Power tools, sporting equipment | Receipts, model numbers, photos |

| Kitchen | Small appliances, tablets | Purchase records, model registrations |

Dealing with Adjuster Undervaluation

If an adjuster’s initial valuation seems low, you have options. Request the specific depreciation schedule applied to each disputed item in writing. Depreciation is not standardized; carriers use proprietary schedules, and the methodology is negotiable with documented counter-evidence. For high-value items, an independent appraisal from a certified appraiser, obtained within 30 days of the claim, carries significant weight in supplemental negotiations.

Most policies include an appraisal clause or dispute resolution provision. If you and your insurer cannot agree on the value of a loss, either party can invoke the appraisal process: each side selects an independent appraiser, those two appraisers select an umpire, and a majority decision sets the loss amount. This process costs money (you pay your appraiser), but for claims involving $10,000 or more in disputed value, it consistently produces better outcomes than accepting an initial low offer. For strategies on managing your coverage costs while maintaining adequate protection, the guide on how to save money on your homeowners insurance covers trade-offs worth knowing.

Accepting an initial settlement check marked “final payment” or “full and final settlement” may waive your right to supplement the claim later, even if you discover additional stolen items or dispute the valuation. Read the check endorsement language before depositing, and ask your adjuster in writing whether the payment is partial or final.

Temporary Security Costs After a Break-In

Boarding broken windows, replacing locks, and installing temporary security measures after a burglary are often covered as part of the claim but must be documented separately. Keep all receipts and request written confirmation from your adjuster that these costs are included in the claim rather than applied against your personal property limit. Some carriers code temporary security as a “loss mitigation expense” covered separately from the property loss itself, which can prevent these costs from reducing your main payout.

Of all homeowners insurance claims filed in 2023, 97.3% were for property damage, a category that includes theft. That concentration means insurers have extensive actuarial data on claim values and documentation disputes, which is why preparation before a loss determines your outcome as much as the policy language itself.

Real-World Example: A Two-Room Burglary Claim and the Sublimit Reality

Consider an illustrative example: a homeowner in a mid-size city files a burglary claim after a break-in through the front door affects the living room and master bedroom. The total reported loss spans two rooms. In the living room: a 65-inch OLED TV ($1,800 original cost, 2 years old), a gaming console ($500, 1 year old), and a Bluetooth speaker system ($400, 3 years old). In the master bedroom: a diamond engagement ring ($6,000 appraised value), a men’s watch ($1,200 original cost), $300 in cash, and a laptop ($1,100, 2 years old).

The homeowner has an HO-3 policy with a $1,500 deductible, ACV settlement for personal property, a $1,500 jewelry sublimit, and a $200 cash sublimit. The front door required $1,200 in structural repairs covered under dwelling coverage. Here is how the claim math works: The living room electronics total $2,700 in original purchase price. Under ACV with age-based depreciation (approximately 20% per year for electronics), the adjuster values the TV at $1,080, the console at $400, and the speaker at $192, for a living room ACV total of $1,672. The bedroom losses are where sublimits collide: the jewelry sublimit caps the ring and watch combined at $1,500. The cash sublimit caps the cash at $200. The laptop, at 2 years old, is ACV-valued at $660.

Total covered personal property loss before deductible: $1,672 (living room) + $1,500 (jewelry, capped) + $200 (cash, capped) + $660 (laptop) = $4,032. After the $1,500 deductible: net personal property payout of $2,532. The structural door repair ($1,200) is covered separately under dwelling coverage, subject to the same deductible on a combined basis, meaning if the carrier applies a single deductible per occurrence, the $1,500 has already been consumed by the personal property loss and the door repair pays in full. Total claim settlement: approximately $3,732 on roughly $11,300 in actual losses. The $7,568 gap comes almost entirely from jewelry sublimits, ACV depreciation, and the cash cap.

If this homeowner had carried an RCV endorsement and a scheduled personal property floater for the ring and watch at their appraised values, the math changes: RCV living room electronics at $2,700 (current replacement), jewelry and watch scheduled at $7,200 with no sublimit, cash at $200 (no change, sublimit still applies), laptop at $1,100. Total before deductible: $11,200. After $1,500 deductible: $9,700. The premium difference for RCV plus scheduled jewelry might run $250–$400 per year. In one claim event, that upgrade produces a $6,168 better outcome.

Your Action Plan

-

Pull your current policy declarations page and read your personal property sublimits

Locate the section listing special limits of liability in your current homeowners policy. Write down the specific dollar caps for jewelry, cash, firearms, and business equipment. If any of those figures look lower than the value of items you actually own in those categories, you have identified a gap that needs addressing before a claim occurs.

-

Confirm whether your policy settles on ACV or RCV for personal property

Check your declarations page for the valuation method applied to contents. If it says actual cash value, request a quote from your insurer or broker for an RCV endorsement. The premium difference is typically $50–$150 per year on a standard policy. For households with electronics, clothing, or furniture worth $30,000 or more in total, the RCV upgrade almost always pays for itself in the first substantive claim.

-

Create a room-by-room home inventory with photos and serial numbers

Walk through each room and photograph its contents, open drawers and closets, and record serial numbers for electronics. Store the inventory in cloud backup or email it to yourself so it survives a theft of your home devices. Apps like Encircle or simply a shared Google Drive folder work well. Update the inventory annually or after any major purchase. This single step has more impact on claim outcomes than any policy change you can make.

-

Get jewelry, watches, and collectibles appraised and schedule them on your policy

For any item worth more than $1,500, obtain a written appraisal from a certified appraiser and ask your insurer to add a scheduled personal property endorsement. The cost is roughly $10–$20 per $1,000 of coverage per year. Scheduled items typically carry no deductible and are covered at agreed value, eliminating both the sublimit and the depreciation dispute on your most valuable portable assets.

-

Review your deductible relative to your likely claim size

A $2,500 deductible saves meaningful premium dollars but effectively excludes smaller burglary losses from your coverage. If a typical burglary in your area involves losses of $3,000–$6,000 (close to the national average), a $2,500 deductible leaves very little net payout after the deductible is applied. Consider dropping to a $1,000 or $1,500 deductible if your local crime data and the value of your portable property suggest moderate-sized losses are the more likely scenario. You can review trade-offs in detail among important homeowners insurance policies you should know.

-

Assess your home office and business equipment exposure

If you work from home as a self-employed person or run any business activity at your residence, verify whether your business equipment is subject to the $2,500 business property sublimit. If your equipment exceeds that figure, ask about a home-based business endorsement or a separate inland marine policy for business equipment. The endorsement typically costs $50–$150 per year and can raise the business property coverage limit to $10,000 or more.

-

Know the claim steps before a burglary happens

Keep your insurer’s claims number in your phone contacts and confirm your policy number is accessible somewhere other than inside your home (cloud storage, email, or a printed copy at work). In the event of a burglary: call police first and obtain a report number, then call your insurer. Do not discard damaged property or begin repairs before an adjuster has reviewed the damage. Document everything with photos before cleanup. Knowing this sequence in advance prevents the most common procedural mistakes that delay or reduce claim payments.

Frequently Asked Questions

Does homeowners insurance cover theft if there is no sign of forced entry?

Most policies require evidence that a theft actually occurred, but they do not universally require forced entry. If a thief entered through an unlocked door or window, the claim may still be valid provided you can document what was taken and when. However, mysterious disappearance, where you cannot confirm theft versus misplacement, is excluded under most standard policies. A police report documenting the theft is required in either case, and your insurer may ask for additional evidence of the break-in if entry points are undamaged.

Are items stolen from my car covered under homeowners insurance?

Personal property stolen from a vehicle is typically covered under homeowners insurance as an off-premises theft, subject to your policy’s off-premises sublimit (usually 10% of your personal property limit). The vehicle itself is not covered under homeowners; that falls to your auto policy’s comprehensive coverage. Note that jewelry, cash, and other sublimit-affected items carry the same per-occurrence caps even when stolen from your car.

What happens if my stolen items were shared property with a roommate or partner?

Standard homeowners policies cover residents of the household who are related to the policyholder. A domestic partner or spouse living in the home is typically covered; an unrelated roommate is generally not covered under your policy and would need their own renters insurance. If disputed items belonged to an uncovered party, the insurer may decline that portion of the claim. Confirm covered household members with your insurer, especially in non-traditional living arrangements.

How long does a homeowners theft claim typically take to settle?

Most straightforward burglary claims settle within 2–4 weeks once all documentation is submitted. Claims involving disputed valuations, high-value jewelry without appraisals, or large business equipment losses can extend to 60–90 days or longer if the formal appraisal dispute process is invoked. Providing a complete documentation package at the outset, the police report, itemized inventory, and purchase evidence, is the single most effective way to shorten the timeline.

Will filing a theft claim raise my homeowners insurance premium?

Filing a claim creates a record in the CLUE (Comprehensive Loss Underwriting Exchange) database that insurers review when setting premiums at renewal. A single theft claim typically results in a 5–20% premium increase at renewal, depending on your carrier, state, and claims history. Multiple claims within a three-to-five year period can trigger non-renewal. For smaller losses close to your deductible, it may be worth calculating whether paying out of pocket preserves your claims-free discount better than filing. There is no universal rule; it depends on your specific premium, deductible, and loss amount.

Can I claim a burglary loss on my taxes if insurance doesn’t fully cover it?

The federal casualty and theft loss deduction for personal property is only available for losses attributed to federally declared disasters under current tax law. A standard residential burglary that is not part of a declared disaster does not qualify for the personal casualty loss deduction. State tax rules vary; a small number of states retain broader theft loss deduction provisions. Consult a tax professional for guidance specific to your state and situation, as tax law in this area has changed multiple times in recent years.

What is a scheduled personal property endorsement and do I need one?

A scheduled personal property endorsement adds specific high-value items to your policy at their appraised or agreed value, bypassing standard sublimits and usually eliminating the deductible for covered losses on those items. You need one if you own jewelry, watches, cameras, musical instruments, or fine art worth more than your policy’s standard sublimit. The cost is low relative to the protection: typically $10–$20 per $1,000 of value per year. Anyone with an engagement ring, heirloom jewelry, or a high-value collection should treat scheduling as a baseline requirement, not an optional upgrade.

Does homeowners insurance pay for hotel stays after a burglary if I feel unsafe returning?

Standard loss of use coverage (Coverage D) pays for additional living expenses when a covered loss makes your home uninhabitable. A burglary that does not render the home physically uninhabitable does not trigger loss of use coverage, even if you feel unsafe staying there. If structural damage from the break-in, a destroyed door, unsecured windows, makes the home genuinely uninhabitable until repairs are complete, temporary housing costs may be covered. The threshold is physical habitability, not personal comfort.

Are firearms covered under homeowners insurance after a theft?

Yes, firearms are personal property covered under homeowners insurance, but most standard policies cap the theft-related payout for firearms at $2,500 per occurrence. If you own multiple firearms with a combined replacement value above that threshold, a firearms endorsement or a separate firearms floater policy can raise the coverage limit significantly. Firearms floater policies from specialty insurers often provide broader protection than standard homeowners sublimits, including coverage for accidental damage and loss in addition to theft.

What documentation do I need to file a successful burglary claim?

At minimum: a police report with a case number, a written itemized list of stolen property including descriptions and approximate values, and any purchase receipts, credit card statements, warranty registrations, or photos that support ownership and value. For jewelry or collectibles above the standard sublimit, a professional appraisal strengthens the claim significantly. Serial numbers for electronics, obtained through manufacturer registrations or prior home inventory records, eliminate the ownership disputes that most commonly delay theft claim settlements. The more documentation you can provide upfront, the faster and more accurately the claim resolves. For broader guidance on coverage documentation, the article on what your home and belongings coverage actually includes provides useful additional context.

The CLUE database retains claim records for up to seven years. Insurers reviewing your application or renewal can see every claim filed during that period, including claims you filed on a previous home. A strong claims history, meaning few or no claims, is one of the most effective tools for negotiating lower homeowners premiums when shopping for coverage.

Only 0.12 out of every 100 homeowners policies resulted in a theft claim annually (2019–2023 weighted average). The low frequency explains why many insurers treat theft claims with extra scrutiny when they do occur, the statistical rarity makes each claim an outlier worth examining closely.

Sources

- Insurance Information Institute, Facts + Statistics: Homeowners and Renters Insurance

- ValuePenguin, Home Insurance Statistics and Data

- Texas Department of Insurance, Homeowners Insurance Guide

- National Association of Insurance Commissioners, A Consumer’s Guide to Homeowners Insurance

- Virginia State Corporation Commission, Virginia Homeowners Insurance Guide

- Illinois Department of Insurance, Homeowners Insurance Shopping Tips and Information

- Federal Bureau of Investigation, Uniform Crime Reporting Program

- NerdWallet, Does Homeowners Insurance Cover Theft?

- Smart Insurance 101, Homeowners Insurance Guide: A Beginner’s Overview

- Smart Insurance 101, How to Save Money on Your Homeowners Insurance

- Smart Insurance 101, Important Homeowners Insurance Policies You Should Know

- Smart Insurance 101, Are You Covered For Anything That Can Happen To Your Home And Belongings?