Fact-checked by the Smart Insurance 101 editorial team

The Verdict

Loss of use coverage in homeowners insurance is worth understanding precisely because it pays the gap between your normal living costs and what you spend on temporary housing during repairs. It is most valuable when your policy limit is at least 20% of your dwelling coverage. It falls short if your home is in a high-cost rental market, repairs drag past 12 months, or the damage stems from a flood or earthquake, which standard policies exclude entirely.

When a fire, windstorm, or major pipe burst makes your home unlivable, the question shifts fast from “will I be okay?” to “who is paying for the hotel?” Loss of use coverage homeowners policies include as Coverage D is what answers that question, and the single factor that determines how much help you actually get is your dwelling coverage limit. According to Insurance.com’s 2025 analysis, most standard policies set this benefit at 20% to 30% of your Coverage A dwelling amount, so a home insured for $400,000 typically carries somewhere between $80,000 and $120,000 in additional living expenses coverage. That sounds like a lot until you price a furnished apartment in a coastal city for six months.

Homeowners insurance premiums are rising sharply, and many policyholders are cutting optional endorsements to offset the cost. Understanding exactly what Coverage D does and does not pay is now a practical necessity, not a detail you can skim.

| Factor | Reasons to Rely on Loss of Use Coverage | Reasons It May Fall Short |

|---|---|---|

| Cost to you | Included in most HO-3 policies at no extra premium line | Higher limits require an endorsement that raises your premium |

| Coverage limit | 20%–30% of dwelling coverage; $80,000 on a $400K policy | Limits can be exhausted before repairs finish in high-cost markets |

| Eligible expenses | Hotel, furnished rental, extra meals, pet boarding, storage, extra commuting costs | Only the increase above your normal spending; your regular mortgage still comes due |

| Covered perils | Fire, windstorm, hail, lightning, and most named perils in HO-3 open-peril policies | Flood and earthquake damage are excluded; you need separate NFIP or earthquake policies |

| Duration | Pays through the full repair or rebuild period, no arbitrary 90-day cap in most policies | Insurer must agree home is uninhabitable; disputes over this determination are common |

| State protections | California mandates a minimum 36-month ALE period for wildfire losses, with extensions | Most states have no minimum; coverage stops when repairs are “reasonably complete” |

| Documentation burden | Reimbursement process is straightforward with receipts and a log of normal pre-loss expenses | Adjusters can dispute what counts as “reasonable”; luxury upgrades are routinely denied |

| Policy type | Applies to homeowners (HO-3), renters (HO-4), and condo (HO-6) policies | Condo policies often tie limits to personal property coverage rather than dwelling value |

Key Takeaways

- Your loss of use limit should be at least 20% of your dwelling coverage; anything lower leaves a real gap if repairs take six months or more.

- Coverage pays only the increase in living costs above your normal baseline, not your full hotel bill or grocery tab.

- The damage must stem from a covered peril and your home must be officially uninhabitable; a leaky roof that keeps one bedroom dry rarely qualifies.

- You keep receipts for every out-of-the-ordinary expense: hotel invoices, restaurant bills above your usual grocery spend, pet boarding, storage unit fees, and extra mileage to work.

- Your normal mortgage, utilities, and debt payments continue regardless; Coverage D does not suspend those obligations.

- If you live in California, your insurer must provide at least 36 months of ALE coverage for wildfire losses, with six-month extension rights built in by regulation.

- If your home is in a market where one-bedroom furnished rentals run $3,000 or more per month, verify that your current limit covers at least 12 months of that rate before a claim happens.

What Does Loss of Use Coverage Actually Pay?

Here’s the thing: Coverage D does not pay your entire hotel bill. It pays the difference between what you now spend on temporary housing and what you were already spending to live in your home. If your mortgage costs $2,200 a month and a comparable furnished apartment runs $3,500, the insurer owes you the $1,300 gap, not the full $3,500.

The Texas Department of Insurance confirms that most home, renters, and condo policies pay some additional living expenses if you cannot live in your house while the insurer pays to repair it. The California Department of Insurance goes further, specifying that ALE coverage includes food and housing costs, telephone or utility installation costs in a temporary residence, extra transportation costs, relocation and storage expenses, and furniture rental when a property is not safe to occupy due to a covered peril such as a wildfire.

What adjusters routinely deny: hotel room upgrades above a comparable standard, meals at upscale restaurants when a casual option was available, a second vehicle when your commute did not require one, and costs that would have occurred regardless of the damage. Document the incremental costs specifically. The calculation is arithmetic, and the insurer’s adjuster will check yours.

When Does Coverage D Kick In?

Two conditions must both be true: the cause of damage must be a covered peril, and the home must be uninhabitable. Miss either condition and the claim gets denied regardless of how much you spent at the extended-stay hotel.

Standard HO-3 open-peril policies cover fire, lightning, windstorm, hail, explosion, theft, vandalism, the weight of snow or ice, and sudden water damage from burst pipes, among others. Floods and earthquakes are the two major carve-outs. If a hurricane’s surge floods your ground floor, the homeowners policy’s Coverage D will not respond; only an NFIP flood insurance policy or a private flood endorsement can cover displacement from that event. If you live in a seismically active area, a separate earthquake policy is the only way to get ALE protection for that specific risk.

The “uninhabitable” standard matters more than most policyholders realize. A burst pipe that saturates the kitchen and two adjoining rooms typically qualifies. Smoke damage that makes the air quality dangerous qualifies. A partial roof leak affecting only one room while the rest of the structure remains safe often does not. Your insurer will send an adjuster to make this determination, and it is not always fast. If you disagree with their finding, the Washington State Office of the Insurance Commissioner notes that Coverage D pays for living expenses over and above your normal costs only when your house is damaged or destroyed and you need another place to stay while it’s being repaired or rebuilt. Documenting the damage with photos and a licensed contractor’s assessment before the adjuster visits strengthens any dispute.

One more timing point: coverage runs concurrently with active repairs, not from the date of loss. If the contractor does not start work for three weeks because materials are backordered, those three weeks may or may not count depending on your policy language. Read that section now, before you need it.

How Loss of Use Limits Are Set and Whether Yours Is Enough

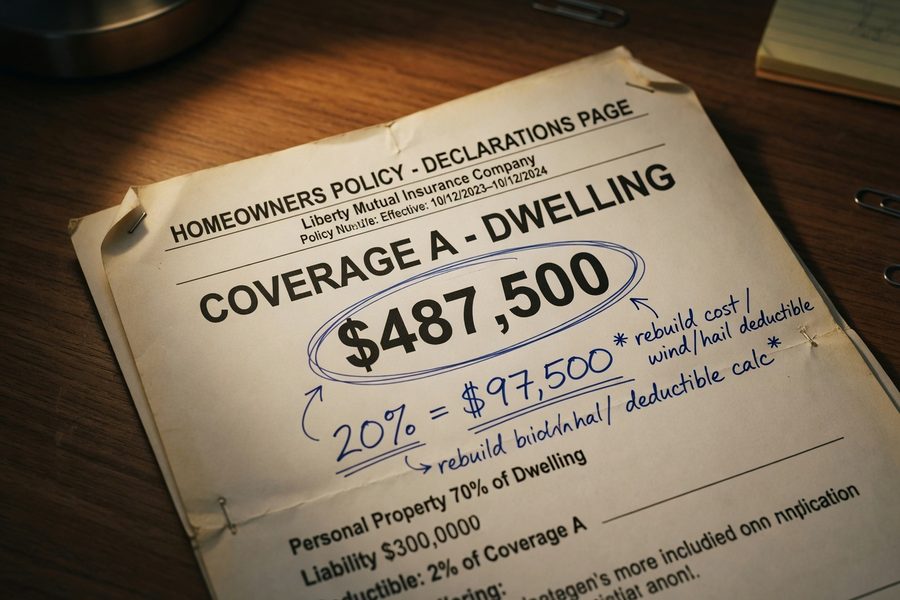

Twenty percent of dwelling coverage is the number most carriers default to, and it is worth doing the math on your own policy. A home insured at $400,000 under a standard HO-3 carries roughly $80,000 in Coverage D, per NerdWallet’s 2026 analysis. That sounds comfortable until you factor in a high-cost rental market.

Here is a concrete example. Suppose your normal monthly housing cost is $2,200 (mortgage plus utilities). A comparable furnished rental in your metro runs $3,800 per month. Your incremental cost is $1,600 per month. At that rate, an $80,000 limit covers 50 months of displacement in theory, but that math only holds if housing expenses are your only incremental cost. Add $600 a month in extra meals, $150 for pet boarding, $200 in storage fees, and $100 in extra commuting, and your monthly incremental spend jumps to $2,650. Now that same $80,000 covers roughly 30 months, which is tighter once you account for major disasters where contractor delays routinely stretch timelines well past a year.

The National Association of Insurance Commissioners (NAIC) describes Coverage D as paying some additional living expenses during home repair, which is accurate but understates the variation between policies. Insurers differ on whether they set limits as a dollar cap, a time cap, or both. Some apply a 12-month time limit regardless of the dollar ceiling. Check your declarations page for both numbers.

California stands out as an exception worth knowing. Following certain losses like wildfires, state law requires insurers to provide a minimum of 36 months of ALE coverage, with the right to six-month extensions, per the California Department of Insurance. Most other states set no floor. Policyholders in those states who face major structural damage are entirely dependent on whatever limit their carrier wrote into the policy. If yours is below 20%, call your agent and ask what a higher-limit endorsement costs annually. For context, the average homeowners insurance policy costs $2,490 per year for $400,000 in dwelling coverage; a Coverage D upgrade typically adds far less than 10% to that figure. For a deeper look at what drives those premium differences, the homeowners insurance guide for beginners on this site breaks down each coverage component clearly.

Who Should and Who Should Not Rely on Default Coverage D Limits

Good candidates

Policyholders who can verify that their current limit, time frame, and covered perils all align with their realistic displacement scenario are well-positioned to rely on the default coverage.

- Homeowners in inland areas with moderate rental markets, where $80,000 covers 18 or more months of incremental costs at prevailing furnished rental rates.

- Owners of newer, wood-frame homes where fire damage is typically repaired in six to nine months rather than requiring a full rebuild.

- Renters with HO-4 policies who pay relatively low monthly rent and whose insurer sets ALE at 30% or more of personal property coverage.

- California policyholders who have confirmed in writing that their carrier applies the 36-month minimum ALE rule to wildfire losses and who have adequate dwelling limits for a full rebuild.

Who should skip it

Default limits are a real liability for certain homeowners, who need either a higher-limit endorsement or a separate policy to fill the gap.

- Homeowners in coastal or high-cost metro markets where furnished rentals routinely run $4,000 or more per month, consuming limit faster than a standard 20% cap can sustain.

- Anyone whose primary displacement risk is a flood or earthquake; standard Coverage D will not respond, and relying on it is a dangerous assumption.

- Owners of historic or custom-built homes where a full rebuild easily takes 24 to 36 months due to permitting, material sourcing, and specialty labor scarcity.

- Policyholders who have already reduced their Coverage A dwelling limit below the full replacement cost value, which proportionally reduces the Coverage D ceiling as well.

Frequently Asked Questions

Does loss of use coverage pay my mortgage while I’m displaced?

No. Coverage D pays the increase in your living costs above your normal baseline, and your mortgage is part of your normal baseline. You still owe every payment to your lender during displacement. Some servicers offer forbearance after a declared disaster, but that is a separate arrangement with your mortgage company and has nothing to do with your insurance claim.

How long does loss of use coverage last?

It lasts as long as your home is being actively repaired due to a covered peril, up to your policy’s dollar or time limit, whichever comes first. Most policies have both. California is the notable exception: state law requires a minimum of 36 months of ALE for wildfire losses, with extension rights built in. Outside California, check your declarations page; a 12-month time cap is common and can be a serious problem if your rebuild runs long.

What if my insurer says my home is habitable but I disagree?

Get a written assessment from a licensed contractor or a licensed industrial hygienist documenting specific hazards, such as structural instability, air quality readings, or code violations, that make the home unsafe to occupy. Present that documentation to your adjuster formally. If the dispute persists, you can file a complaint with your state insurance commissioner or invoke the appraisal or arbitration clause most policies include. For more on navigating insurer disputes and coverage decisions, the article on important homeowners insurance policies you should know covers your rights in more detail.

Is loss of use coverage included in renters insurance?

Yes, renters insurance (HO-4) includes ALE coverage, though limits are set differently since there is no dwelling coverage to peg a percentage to. Renters policies typically set the limit as a percentage of personal property coverage or as a fixed dollar amount. According to Insurance Information Institute data, only 5.3% of insured homes filed a claim in 2023, but displacement claims when they do occur are among the most financially disruptive. Renters, who lack equity to fall back on, often feel that impact hardest.

Filing a Claim: What the Process Looks Like

Speed and documentation are the two levers you control. Call your insurer the day you are displaced, not a week later. Report the claim, ask for the claims adjuster’s direct contact information, and confirm whether your policy requires pre-approval for temporary housing expenses or allows reimbursement after the fact. Policies differ on this, and exceeding a daily hotel rate your insurer considers unreasonable is a dispute you want to avoid.

Keep a running log from day one. Record every incremental expense with the receipt attached: hotel invoices, restaurant bills with a note of your normal weekly grocery spend for comparison, pet boarding confirmation, extra miles driven to work or school. The adjuster’s job is to verify that each cost is both caused by the displacement and above your pre-loss baseline. The easier you make that verification, the faster payments move.

One often-overlooked documentation step is establishing your normal pre-loss expenses in writing. Pull three months of bank and credit card statements showing your typical grocery, utility, and transportation costs before the damage occurred. That baseline is what the adjuster uses to calculate the incremental difference. Without it, you may end up negotiating from a number the insurer picked rather than one rooted in your actual household spending. This is also where understanding what your home and belongings coverage actually includes pays off; knowing the policy language before a claim avoids surprises mid-process.

If your insurer’s payments are slow or disputed, many state insurance departments have emergency hotlines active after major disasters. Using them is faster than waiting for an internal escalation. And if you are simultaneously managing a personal property (Coverage C) claim, keep those receipts and the ALE receipts in separate files. Commingling them creates confusion that slows both claims. For a broader look at how home coverage costs are structured and what you can do to manage them, the guide on how to save money on homeowners insurance is worth reading before your next renewal. And if rising premiums are already stressing your household budget, the piece on why insurance premiums are rising so sharply explains the market forces driving that trend.

Sources

- Texas Department of Insurance, Additional Living Expenses Coverage

- California Department of Insurance, Insurance Coverage for Additional Living Expenses

- Washington State Office of the Insurance Commissioner, How Home Insurance Works

- National Association of Insurance Commissioners (NAIC), Homeowners Insurance Topics

- Insurance Information Institute, Facts and Statistics: Homeowners and Renters Insurance

- NerdWallet, Average Homeowners Insurance Cost (2026)

- Insurance.com, Additional Living Expenses Coverage Explained (2025)

- FEMA, National Flood Insurance Program