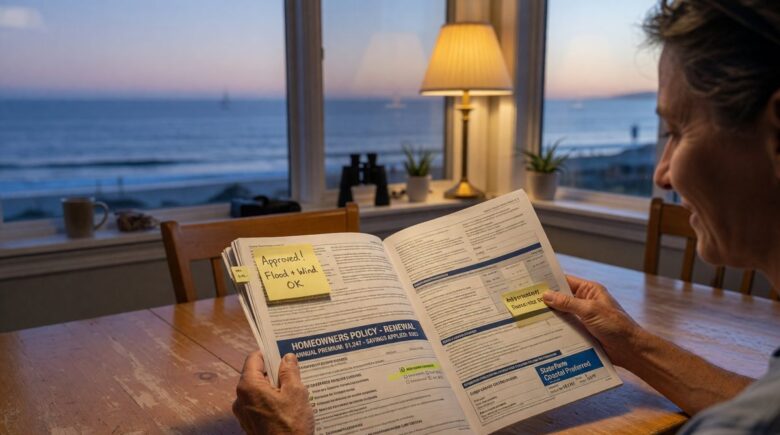

Coastal homeowners insurance affordable enough to justify staying in your home is the challenge facing millions of property owners along the Gulf and Atlantic coasts right now. Premiums haven’t just risen; they’ve reset to a new, higher floor. The U.S. Government Accountability Office found that while average U.S. homeowners insurance premiums rose just 3% nationally from 2019 to 2024 after inflation, parts of southern coastal areas saw increases of 25% or more over that same period. That’s not a blip. It’s a structural shift driven by reinsurance costs, rising construction prices, and more frequent storm damage.

The picture is complicated but not hopeless. Florida recorded an average rate increase of just 1% in 2024, the lowest in the nation, with costs actually dipping 0.9% in Q4 of that year, according to the Florida Office of Insurance Regulation. Other coastal states are at different stages of that cycle. Below, you’ll find out why standard policies fall short in coastal zones, which mitigation upgrades deliver real discounts, how to shop effectively, and what backup options exist when the private market won’t move.

Key Takeaways

- Southern coastal homeowners saw premium increases of 25% or more (inflation-adjusted) from 2019 to 2024, far outpacing the 3% national average.

- Florida’s median annual property insurance cost for mortgaged homes was $2,273 in 2023, the highest of any state, with many coastal owners paying well above that figure.

- Alabama mandates that insurers offer FORTIFIED Home discounts of 20–50% on the wind premium portion for certified properties, one of the most concrete savings opportunities available in 2026.

- Coastal owners typically need 2–3 separate policies (homeowners, wind, flood) to be fully covered; understanding each layer is the first step to managing total cost.

The 2026 Reality for Coastal Insurance Costs

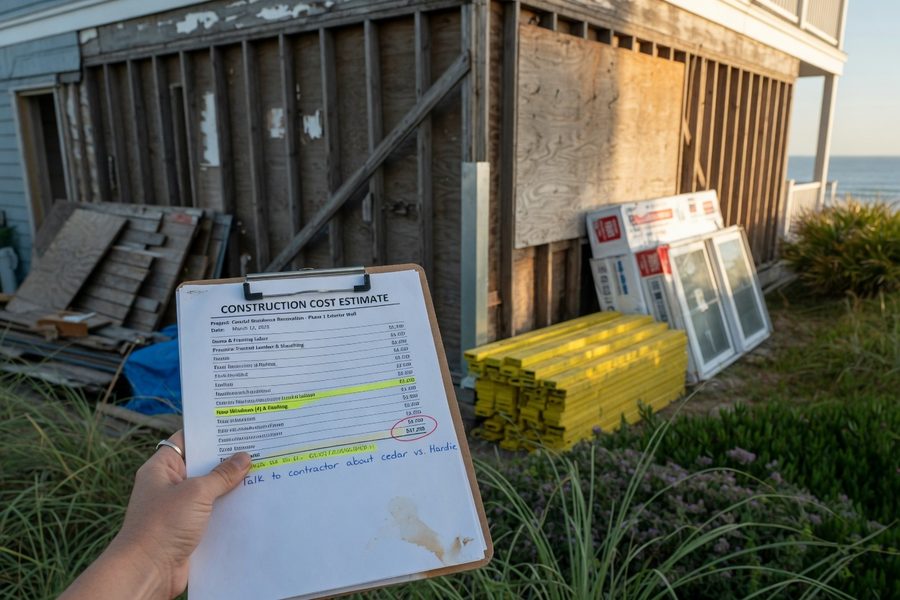

Premiums have stabilized in 2026, but “stabilized” doesn’t mean affordable. It means the steep climb of 2021–2023 has slowed, not reversed. Reinsurance costs, what insurers pay to backstop their own risk, remain elevated. Construction materials are still roughly 30–40% more expensive than pre-pandemic levels. When a home has to be rebuilt, it costs more, and insurers price that reality into every policy renewal.

The U.S. Census Bureau reported that 5.3 million U.S. households paid more than $4,000 per year for property insurance in 2023. Florida’s median was $2,273 annually for mortgaged homes, but that figure masks the coastal reality, where total coverage costs combining homeowners, wind, and flood frequently exceed $7,000 to $10,000 per year. At that level, insurance rivals or exceeds the principal-and-interest payment on many mortgages.

Florida’s recent stabilization is real and worth acknowledging. Some carriers reduced rates by roughly 11% for specific policy classes in early 2026 as new insurers entered the market and litigation reform took hold. But that improvement is uneven. Owners in high-surge zones, with older roofs, or on barrier islands are still seeing significant renewal increases. Don’t assume Florida’s statewide trend applies to your specific property and zip code.

The table below compares key cost and coverage benchmarks across major coastal states, so you can place your own situation in context before shopping.

| State | Avg. Annual Homeowners Premium (2024) | Typical Wind Deductible | Residual Market / Wind Pool | FORTIFIED Discount Mandate? | NFIP Policies in Force (2024) |

|---|---|---|---|---|---|

| Florida | $2,273 (mortgaged median, 2023) | 2–5% of dwelling value | Citizens Property Insurance | No statewide mandate | ~1.7 million |

| Alabama | $1,820 | 1–5% of dwelling value | Alabama Insurance Underwriting Association (AIUA) | Yes, 20–50% wind premium discount required | ~56,000 |

| Texas | $2,150 | 1–5% of dwelling value | Texas Windstorm Insurance Association (TWIA) | No statewide mandate | ~660,000 |

| Mississippi | $1,640 | 2–5% of dwelling value | Mississippi Windstorm Underwriting Association (MWUA) | No statewide mandate | ~47,000 |

| Louisiana | $2,490 | 2–5% of dwelling value | Louisiana Citizens Property Insurance | No statewide mandate | ~490,000 |

| New Jersey | $1,340 | 1–2% of dwelling value | New Jersey FAIR Plan | No statewide mandate | ~230,000 |

| South Carolina | $1,870 | 1–5% of dwelling value | South Carolina Wind and Hail Underwriting Association (SCWHUA) | No statewide mandate | ~210,000 |

Why Standard Policies Fall Short in Coastal Zones

A standard HO-3 homeowners policy was not designed with coastal storm risk in mind. Most HO-3 forms exclude wind and hail damage in designated coastal territories, and virtually all of them exclude flooding entirely. That means if a hurricane hits your home, the wind damage might not be covered by your main policy, and the storm surge almost certainly won’t be. You need separate coverage for both, which is where total costs climb fast.

Wind coverage in coastal states is often obtained through a state residual market (a wind pool) or through an endorsement from a surplus lines insurer. Flood coverage comes either through the National Flood Insurance Program (NFIP), administered by FEMA, or a private flood insurer. Each policy carries its own deductible. For windstorm, expect a percentage-based hurricane deductible: typically 2–5% of your dwelling’s insured value. On a $400,000 home, a 2% hurricane deductible means you absorb the first $8,000 of damage yourself. At 5%, that’s $20,000 out of pocket before the insurer writes a check.

HO-5 open-perils forms offer broader coverage but are harder to obtain in coastal zones and command higher premiums. Surplus lines carriers such as Lloyd’s of London syndicates and domestic specialty markets like Scottsdale Insurance, a Nationwide subsidiary, do write coastal risks that admitted carriers decline, though at a price premium and without the same state guaranty fund protections. If you’re unclear on what your current policy actually covers, our Homeowners Insurance Guide walks through the basics of what each form covers and excludes. Understanding the gaps is the prerequisite for filling them cost-effectively.

Mitigation Upgrades That Deliver Real Discounts

This is where coastal homeowners have the most direct control over their premiums. The FORTIFIED Home program, administered by the Insurance Institute for Business and Home Safety (IBHS), sets construction and retrofit standards at three levels: Bronze, Silver, and Gold. Alabama state law requires insurers to offer discounts for FORTIFIED certification, with wind premium reductions ranging from 20% to 50% depending on the level achieved. That’s not a courtesy discount; it’s mandated. Other Gulf Coast states are moving in the same direction, and IBHS has documented real-world premium outcomes across hundreds of certified properties.

Specific upgrades that generate measurable savings include impact-resistant windows and doors, roof-to-wall tie-downs, secondary water barriers beneath roofing material, and reinforced garage doors. Elevation matters on the flood side: homes elevated above base flood elevation qualify for lower NFIP rates, and private flood insurers price elevation aggressively. The ROI on a FORTIFIED Bronze re-roof can break even in two to four years purely through premium savings, depending on your wind insurer’s discount schedule. The Insurance Information Institute specifically cites disaster-resistant improvements as one of the most reliable paths to lower premiums in high-risk areas.

One caution: the upfront cost of full FORTIFIED Gold certification on an older home can run $15,000 to $30,000 or more. For owners on tighter budgets, starting with Bronze (which focuses on the roof system) is the most cost-efficient entry point and the level that unlocks most of the available discount.

Shopping Strategies to Secure Competitive Quotes

Rate shopping is more complicated for coastal properties than for inland homes, and it matters more. Standard carriers writing business in your zip code may be few, but the spread between the most expensive and least expensive available option can be $1,500 to $3,000 per year on identical coverage. Getting three or more quotes is the baseline; getting five is better.

Work with an Independent Agent Who Knows Coastal Markets

A captive agent represents one carrier. An independent agent can access surplus lines markets, regional specialty insurers, and state wind pool programs simultaneously. For coastal properties, that breadth matters. Ask any agent you work with how many coastal properties they place annually and which carriers are actively writing new business in your county right now. Carriers like Universal Property & Casualty, Heritage Insurance Holdings, and Slide Insurance have all been active in Florida’s coastal market at various points in recent years; knowing who is currently writing new policies in your zip code is genuinely useful intelligence. Our guide on choosing an insurance broker explains what to look for when selecting someone to represent you.

Use State Comparison Tools

Florida’s Office of Insurance Regulation offers a free CHOICES rate comparison tool that shows sample average rates by county, factoring in dwelling value, construction type, wind mitigation features, and deductibles. Sample rates don’t equal your actual quote, but the tool tells you quickly which carriers are competitive in your area and gives you a benchmark before you call agents. The Oregon Division of Financial Regulation offers similar guidance for Pacific coastal owners, recommending independent agents and shopping tools as the first step when standard market options feel limited.

Don’t Underinsure to Cut Costs

One common mistake is reducing dwelling coverage to lower the premium. If construction costs in your area have risen 35% since your policy was written, your coverage limit may already be too low. After a total loss, an underpaid claim is catastrophic. Raise your deductible before you lower your coverage limit; that’s where the risk trade-off makes more sense. For context on how deductibles interact with your total cost exposure, see our explainer on deductibles versus out-of-pocket maximums.

Alternative Coverage Options Beyond Traditional Insurers

State wind pools are residual market insurers of last resort. Florida has Citizens Property Insurance; Alabama has the Alabama Insurance Underwriting Association (AIUA); Mississippi has the Mississippi Windstorm Underwriting Association (MWUA); and Texas has the Texas Windstorm Insurance Association (TWIA). These programs exist to cover properties the private market won’t. The trade-off is real: wind pools often carry coverage limits below full replacement cost, charge rates that reflect the state’s underlying risk exposure, and may require a waiting period or proof of private market denial before you can enroll. They are a backstop, not a bargain.

Private flood markets have expanded meaningfully for mitigated and elevated properties. Insurers such as Neptune Flood and Palomar Specialty Insurance are offering policies in select coastal communities, including towns along the Jersey Shore in New Jersey, that undercut NFIP rates for well-elevated homes, with broader coverage terms and faster claims processes. This is a genuine alternative worth pricing. If your home sits above base flood elevation and you’ve invested in mitigation, private flood deserves a serious look before you default to NFIP renewal.

Bundling your homeowners coverage with auto insurance can generate 5–15% discounts on each policy, depending on the carrier. If your insurer writes both lines and is competitive on coastal property, that bundling discount is straightforward savings. For a $7,000 annual homeowners premium, even a 5% discount represents $350 per year. The U.S. Government Accountability Office has also noted that federal and state policy options, including potential tax incentives for resilience investments, are under discussion as longer-term solutions to the coastal affordability problem, though no sweeping national program was in place.

One concrete example: a coastal Florida homeowner paying $7,000 per year for combined coverage who qualifies for a FORTIFIED Bronze wind discount of 25% on a wind premium that represents 40% of total cost would save roughly $700 per year ($7,000 × 40% = $2,800 wind premium; $2,800 × 25% = $700 annual savings). Over five years, that’s $3,500 in savings, more than enough to offset a typical re-roofing premium upgrade to FORTIFIED standards.

If you want a broader view of how premium pressures are building across all insurance types, our article on why insurance premiums are rising provides useful context on the forces driving costs nationwide.

How to Save Money on Your Coastal Homeowners Insurance

Beyond mitigation upgrades, several other tactics can trim your total bill. Raising your hurricane deductible from 2% to 5% of dwelling value will reduce your premium, but only make that move if you have the cash reserves to cover the larger out-of-pocket exposure. For a $400,000 home, the difference is $8,000 versus $20,000 at your expense before insurance kicks in. That’s not a trade-off to make lightly, and financial advisors generally recommend keeping three to six months of liquid savings before accepting a higher deductible.

Security systems, claims-free discounts, and newer home features (updated electrical, updated plumbing, hip roofs) all generate smaller but additive savings. Annual policy reviews matter here. If you’ve made improvements, had no claims, or if your home has appreciated significantly, your risk profile may have shifted enough to warrant re-quoting. Carriers like State Farm, Allstate, and Chubb each evaluate risk characteristics differently; what one carrier declines or prices punitively, another may rate more favorably. The Maryland Insurance Administration has documented through formal hearings how regulatory attention to coastal affordability is increasing, which means more pressure on insurers in some states to keep options available. Our post on how to save money on homeowners insurance covers many of these tactics in more detail for any property type.

One more consideration worth naming: some homeowners have explored parametric insurance products, policies that pay out based on a measured event (say, wind speed at a specific weather station) rather than a traditional loss adjustment. These products, offered by carriers such as Jumpstart Insurance and some Lloyd’s syndicates, can supplement a standard policy for coastal wind risk, though they require careful reading of trigger conditions and don’t replace conventional coverage.

Frequently Asked Questions

Is coastal homeowners insurance always more expensive than inland coverage?

Yes, in virtually every coastal market, and the gap is significant. The combination of hurricane wind risk, storm surge flood exposure, and higher rebuilding costs produces premiums that often run two to four times the national median. The exact premium depends on your specific location, construction type, elevation, and mitigation features, but baseline costs are structurally higher than inland equivalents, and that’s unlikely to change in the near term.

Do I really need a separate flood policy if I have homeowners insurance?

Almost certainly. Standard homeowners policies exclude flood damage entirely; that includes storm surge, which is often the most destructive force in a hurricane. If your home is in a FEMA-designated Special Flood Hazard Area (SFHA) and you have a federally backed mortgage, flood insurance isn’t optional; it’s required. Even outside those zones, coastal properties face meaningful flood risk. Pricing both NFIP and private flood options takes about 30 minutes and can save you from a total uninsured loss.

What is the FORTIFIED Home program and how do I get certified?

FORTIFIED is a voluntary construction and retrofit standard developed by the Insurance Institute for Business and Home Safety (IBHS). Bronze certification focuses on the roof system; Silver adds connections from roof to walls; Gold addresses the whole structure. To get certified, a licensed FORTIFIED evaluator inspects your home and documents that it meets the standard’s requirements. Certification must be renewed periodically, typically every five years for roofs. In Alabama, insurers are legally required to offer wind premium discounts of 20–50% to FORTIFIED-certified homes. Other states offer incentives, though the mandate varies.

What happens if no private insurer will cover my coastal home?

Your state’s residual market insurer, often called a wind pool or FAIR Plan, is the backstop. These programs are required to cover properties the voluntary market won’t. The trade-off: coverage limits are often lower than full replacement cost, rates can be high, and availability rules vary by state. The Oregon Division of Financial Regulation recommends the FAIR Plan only as a last resort after being denied by at least two standard insurers and after exhausting independent agent options. If you end up in a wind pool, treat it as temporary and keep shopping the private market annually.

Can bundling my auto and homeowners insurance actually help on coastal premiums?

It can, but with one important caveat: the savings only materialize if your homeowners insurer is also competitive on coastal property. Many carriers writing coastal business don’t also write competitive auto rates, and vice versa. Get separate quotes for each before assuming the bundle is a win. If the same insurer is legitimately competitive on both, bundling discounts of 5–15% are common and worth taking.

Is it worth staying in a coastal home if insurance costs keep rising?

That’s a financial decision only you can make, but it’s worth running the full math. Add your current or projected insurance cost, property taxes, and maintenance to your mortgage payment and compare that total against local rent. Some coastal markets have crossed the line where ownership costs are genuinely unsustainable without significant equity gains to offset them. On the other side: mitigation investments, improving state markets (Florida’s stabilization is real even if partial), and the possibility of federal incentive programs in coming years all factor in. There’s no universal answer, but the question deserves honest arithmetic, not just emotional attachment to a property.

Sources

- U.S. Government Accountability Office, Homeowners Insurance: Affordability and Availability in Coastal and Disaster-Prone Areas (2026)

- U.S. Census Bureau, Property Insurance Costs (2025)

- Insurance Information Institute, 12 Ways to Lower Your Homeowners Insurance Costs

- Maryland Insurance Administration, Coastal Property Insurance Availability and Affordability Hearings

- FEMA, National Flood Insurance Program (NFIP)

- Florida Office of Insurance Regulation, Homeowners Insurance Market Reports

- Florida Office of Insurance Regulation, CHOICES Rate Comparison Tool

- Insurance Institute for Business and Home Safety (IBHS), FORTIFIED Home Program

- Texas Windstorm Insurance Association (TWIA)

- Citizens Property Insurance Corporation (Florida)

- Alabama Insurance Underwriting Association (AIUA)

- Oregon Division of Financial Regulation, Homeowners Insurance Resources

- Insurance Information Institute, Facts and Statistics: Flood Insurance

- NOAA National Centers for Environmental Information, Billion-Dollar Weather and Climate Disasters

- Consumer Financial Protection Bureau (CFPB), Homeownership Resources