Sandwich generation caregivers, adults simultaneously raising children and supporting aging parents, are the most financially exposed household type in the country, yet most insurance reviews treat them like a standard dual-income couple with a mortgage. That mismatch is expensive. Insurance for caregivers in this position needs to account for a reality that standard coverage checklists were never designed to address: one person is the structural load-bearer for two or three generations at once, and a single uncovered event cascades outward in ways it would not in a non-caregiver household.

According to AARP and the National Alliance for Caregiving (2025), 63 million Americans provided ongoing care for an adult or a child with a complex medical condition or disability in the past year, and 29% of those caregivers were sandwich generation, supporting both children and aging adults simultaneously. The average caregiver spends $7,200 out of pocket annually on caregiving costs alone. This article walks through the specific coverage gaps that most financial advisors overlook, the legal traps almost nobody warns you about, and the order in which to address them.

Key Takeaways

- 29% of family caregivers are sandwich generation, supporting both aging parents and dependent children, yet most insurance portfolios are built for a standard two-income household with no dependents beyond minor children.

- Employer group disability plans typically replace only 60–70% of income and often shift from “own occupation” to “any occupation” definitions after two years, a structural flaw that hits caregivers who reduced work hours especially hard.

- Hiring a private in-home aide for a parent can make a family a legal household employer, most homeowners policies explicitly exclude household employees from workers’ comp and liability coverage, leaving families personally exposed.

- Fewer than 3% of Americans own a long-term care insurance policy, meaning the caregiver in their 40s or 50s who buys hybrid life/LTC coverage now locks in lower premiums before underwriting becomes significantly harder.

Why the Sandwich Generation Caregiver Is Under-Insured by Design

Most insurance frameworks were built around a simple model: primary earner, dependents, replace income if something goes wrong. That model breaks down immediately for someone managing a parent’s medical appointments, coordinating paid help, doing school pickups, and maintaining a career at the same time. The U.S. Bureau of Labor Statistics (2025) counted 7.6 million eldercare providers who were also parents of children living at home. These households carry risks that standard coverage simply does not price.

The financial exposure is not theoretical. Caregivers lose an average of $21,000 annually from reduced work hours, and women who leave the workforce entirely for caregiving sacrifice an estimated $295,000 in wages and benefits over a career, with a retirement fund impact roughly $40,000 greater than their male counterparts. The AARP Public Policy Institute values unpaid family caregiving nationwide at more than $1 trillion annually, exceeding all combined federal, state, and local Medicaid spending in 2024. That number reflects an enormous economic contribution that has no insurance protection wrapped around it.

The core problem is that advisors assess risk in isolation: life insurance based on income, health insurance based on employer plan availability, maybe a disability rider on the side. Nobody sits down and maps out what happens if the caregiver becomes unable to function. Who manages the parent’s care? Who coordinates the children’s schedules? Who negotiates with the home health agency? Those tasks have market-rate costs that pile on top of lost income, and most coverage portfolios ignore them entirely. For a broader look at how different types of insurance connect to each other, the fundamentals are worth reviewing before doing a full audit.

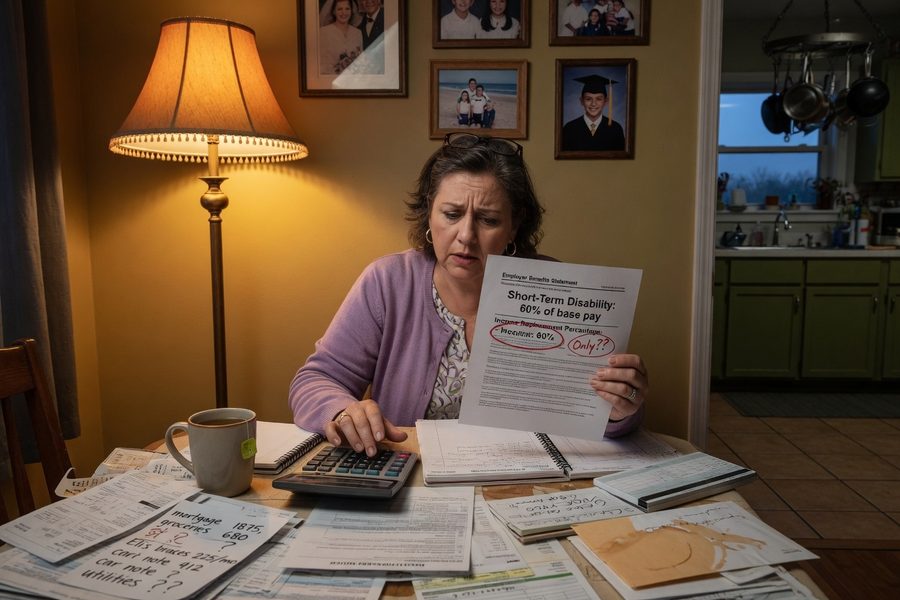

Disability Insurance: Why Your Employer Plan Will Fail You

Group long-term disability plans typically replace 60–70% of base salary. That sounds reasonable until you read the fine print. Most group plans define disability using an “own occupation” standard for the first two years of benefits, meaning you qualify if you can’t perform your specific job. After two years, the definition shifts to “any occupation”: you lose benefits if you can theoretically do any work at all, even work far below your skill level or salary. A caregiver who stepped back from a demanding professional role to manage elder care may find that the “occupation” the insurer uses at claim time is their reduced-hours version, dramatically lowering the benefit or eliminating it.

An individual own-occupation policy addresses this directly. Look for a benefit period running to age 65 (not a shorter five- or ten-year period), a residual/partial disability rider that pays proportionally if you can work reduced hours, and a future increase option so you can raise coverage later without new medical underwriting. The elimination period, typically 90 days, matters here too: that’s three months with zero disability income, which a household already spending $7,200 per year on caregiving costs may not be able to absorb. Critical illness insurance, discussed below, is specifically useful for bridging that window.

The caregiver-specific case for strong disability coverage is straightforward: disability for this person doesn’t just affect one income. It removes the person managing medications, driving parents to appointments, coordinating paid help, and absorbing elder-care logistics for an entire extended family. The gap doesn’t stop at the paycheck. If you’re evaluating your options, understanding how deductibles and out-of-pocket maximums interact is also relevant when estimating total financial exposure during a disability period.

Long-Term Care Insurance Is for You, Not Just Your Parent

Most articles aimed at sandwich generation readers focus on whether Mom or Dad has an LTC policy. This one is going to make a different point: the 45-year-old caregiver needs to think about their own long-term care coverage now. Fewer than 3% of Americans own a long-term care insurance policy, standalone LTC insurers have exited the market significantly since the early 2000s, and premiums have risen sharply. Buying in your 40s or early 50s locks in lower rates before underwriting becomes harder, and before health changes make coverage unaffordable or unavailable.

For most buyers in 2026, the most practical option is a hybrid life/LTC policy. The death benefit addresses the “use it or lose it” objection that makes traditional LTC feel like a gamble, and a living-benefits rider activates for qualifying conditions regardless of age. That dual function appeals especially to caregivers who also need life insurance, which most of them do. Traditional standalone LTC policies still exist and may be appropriate in specific situations, but the market reality makes hybrid policies the more defensible starting point for most sandwich generation buyers today.

One honest caveat: hybrid life/LTC policies carry higher upfront premiums than standalone term life, and the long-term care benefit pool is often smaller than what a dedicated LTC policy would provide. For someone with serious family history of cognitive decline or other long-duration care needs, a standalone LTC policy, where you can still qualify for one, may provide better total benefit at lower risk of exhaustion. The hybrid structure is a strong default, but it is not the right answer for every situation.

| Coverage Type | Typical Annual Cost (Age 50) | Benefit Trigger | Elimination Period | Key Caregiver Limitation |

|---|---|---|---|---|

| Employer Group LTD | $0–$600 (employer-subsidized) | Unable to perform own job (2 yrs), then any job | 90 days | Shifts to “any occupation” after 2 years; may base benefit on reduced-hours role |

| Individual Own-Occupation Disability | $2,400–$5,200 | Unable to perform specific occupation, to age 65 | 90 days | Underwriting can exclude pre-existing conditions; cost rises sharply after age 55 |

| Critical Illness Insurance | $400–$1,800 | Diagnosis of covered condition (cancer, heart attack, stroke) | None (lump sum on diagnosis) | Covered conditions are limited; does not replace income for non-covered illnesses |

| Hybrid Life/LTC Policy | $3,000–$7,500 | 2 of 6 ADL impairments, or cognitive impairment | 90 days | LTC benefit pool smaller than standalone LTC; higher upfront cost than term life alone |

| Standalone LTC Insurance | $2,200–$5,800 | 2 of 6 ADL impairments, or cognitive impairment | 30–90 days | Premiums can increase; fewer carriers offering new policies |

| Household Employer Workers’ Comp | $400–$800 (one part-time employee) | On-the-job injury of household employee | None | Required only for private hires; agency workers may already be covered, but must confirm in writing |

The Household Employer Trap Nobody Warns You About

Here is a risk almost no financial advisor flags: when a sandwich generation caregiver hires a private in-home aide for their parent, they may legally become a household employer. Most homeowners insurance policies explicitly exclude ongoing household employees from workers’ compensation and general liability coverage. If that aide trips on a wet floor, throws out their back transferring a patient, or is injured in any other on-the-job way, the family is personally liable for all medical costs and lost wages. In states like California, failure to carry a separate workers’ comp policy for household employees can also trigger criminal penalties and fines running into the tens of thousands of dollars. For more context on liability exposure in a personal household setting, liability insurance costs are rising for exactly these reasons.

The agency versus private-hire distinction matters here. Aides hired through a licensed home care agency typically bring their own workers’ comp and liability coverage; confirm this in writing before signing anything. Private hires do not carry their own coverage, and the liability falls entirely on the family. Some agencies classify their workers as independent contractors rather than employees; that arrangement may not provide liability coverage either, so the right question to ask is: “Do you carry workers’ comp and general liability for this specific worker on this specific job?” Get the answer in writing. A separate household employer workers’ comp policy generally costs between $400 and $800 per year for a single part-time employee, a modest cost relative to the exposure it eliminates.

Life Insurance: The Coverage Calculation Is Wrong for Caregivers

Standard life insurance advice is to replace 10 to 12 times your income. For sandwich generation caregivers, that math is incomplete. The death of a caregiver removes not just income but an enormous volume of unpaid labor: managing a parent’s medical care, coordinating paid help, driving children to activities, and serving as the household’s operational center. All of that now has to be purchased at market rates. A family with a $700,000 mortgage and $1 million in life insurance has $300,000 remaining, which may not come close to covering elder-care replacement costs, childcare, and the years of household management the deceased was providing without pay.

A true needs analysis for a sandwich generation caregiver should include elder-care replacement costs, projected years of parent support remaining, childcare costs if the surviving parent needs to return to full-time work, and a realistic estimate of household coordination costs. These are not small numbers. Run the arithmetic before settling on a coverage amount. For a starting point on the term life market, current term life options are worth comparing before locking in coverage.

One specific, actionable detail that almost never comes up in a life insurance review: the 529 successor-owner designation. If a caregiver owns a child’s college savings account and dies without naming a successor owner, the account can be frozen or subject to probate, creating delays and potential tax complications for the surviving household. Naming a successor owner takes about five minutes on the account provider’s website. It is the kind of detail that falls outside a standard insurance checklist but directly affects this audience.

Health Insurance When Caregiving Forces a Job Change

Many sandwich generation caregivers eventually reduce hours or leave jobs entirely to manage care. The Nebraska Department of Insurance specifically notes that caregivers who leave employer-sponsored positions should plan for health insurance continuity before, not after, the job change. Losing job-based coverage qualifies for a Special Enrollment Period through the ACA Marketplace, but you have 60 days to act, and few caregivers have the bandwidth to research plans under that kind of time pressure.

Medicaid is the backup plan for 13% of family caregivers, according to KFF (2026). That coverage is now at acute risk: the One Big Beautiful Bill Act, signed in 2025, introduced new Medicaid work requirements that could affect caregivers who left employment to provide full-time care. AARP has warned that 7.3 million caregivers ages 18 to 64 rely on Medicaid for their own health coverage, a population that overlaps directly with people whose caregiving responsibilities are the precise reason they aren’t employed. This is a live policy risk in 2026, with real consequences for caregivers who haven’t built a contingency plan. Separately, shrinking medical coverage and rising costs are already squeezing the households most affected.

For caregivers who remain on a high-deductible health plan, a Health Savings Account (HSA) is worth maximizing. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses, including many elder-care costs, are also tax-free. That triple tax advantage creates a meaningful buffer for a household already stretched thin. The Administration for Community Living’s National Family Caregiver Support Program also provides counseling and service referrals that can help caregivers identify which programs they qualify for, including state-level health coverage assistance. Veterans’ family caregivers should check separately: the VA’s Program of Comprehensive Assistance for Family Caregivers provides a financial stipend, CHAMPVA health insurance access, and mental health counseling for approved primary caregivers of eligible veterans.

Frequently Asked Questions

Does homeowners insurance cover an in-home aide who gets injured on the job?

Almost certainly not. Most homeowners policies explicitly exclude ongoing household employees from workers’ compensation coverage. A standard homeowners liability policy might cover a one-time visitor who slips on your steps, but it is not designed to cover employees who work in your home regularly. If you hire a private aide directly, rather than through a licensed agency that carries its own coverage, you need a separate household employer workers’ comp policy. Confirm in writing with any agency you use whether their workers are covered, because independent contractor arrangements may leave you exposed regardless of the agency label.

Is my employer’s disability plan enough if I’m a sandwich generation caregiver?

Probably not. Group plans typically replace 60–70% of base salary and shift from an “own occupation” to an “any occupation” definition after two years. For a caregiver who has already scaled back their work role to manage elder care, the insurer may assess disability based on that reduced position rather than your original career. An individual own-occupation policy, bought in addition to any group coverage, is the more reliable foundation. The cost depends on your occupation class, age, and health, but locking it in before a health change makes it significantly more affordable.

At what age should a caregiver buy long-term care insurance for themselves?

The practical window is your mid-40s to mid-50s. Premiums are substantially lower at 45 than at 60, and underwriting is more straightforward before chronic health conditions develop. Waiting until you’re already in heavy caregiving mode risks a health change that makes you uninsurable. If standalone LTC premiums feel unaffordable, a hybrid life/LTC policy packages the death benefit with the long-term care rider, making the combined cost easier to justify, especially for caregivers who also need life coverage.

Can a sandwich generation caregiver qualify for any government support to help with their own health insurance?

Yes, several programs exist, though eligibility varies. ACA Marketplace subsidies are available to caregivers whose household income falls within the qualifying range, especially if they’ve left employment or reduced hours. The Illinois Department on Aging’s Senior Health Insurance Program (SHIP) offers free, independent benefits counseling to Medicare beneficiaries and their caregivers in Illinois, similar programs exist in other states under Medicare’s State Health Insurance Assistance Program (SHIP) network. Veterans’ family caregivers should review the VA’s CHAMPVA program. The Medicaid landscape is in transition in 2026 due to new work requirements, so get current information from your state Medicaid office before relying on it as a long-term plan.

What is critical illness insurance and why does it matter specifically for caregivers?

Critical illness insurance pays a lump sum directly to you upon diagnosis of a covered condition, typically cancer, heart attack, or stroke. Unlike disability insurance, there is no elimination period; the cash arrives shortly after diagnosis, not after a 90-day wait. For a caregiver, that matters enormously: you need money immediately to hire replacement care for your parent and your children while you’re in treatment, not three months later. The payout can also cover out-of-pocket medical costs and bridge the gap while a disability policy kicks in. Critical illness riders can often be added to an existing life insurance policy at relatively modest cost, making this one of the more accessible additions for caregivers whose budgets are already tight.

If I can only afford one additional coverage layer, where should I start?

Disability insurance. If the caregiver cannot work, every other financial obligation, mortgage, elder-care costs, children’s needs, becomes immediately threatened. Life insurance matters too, but death is a one-time event; disability can stretch for years while costs keep accumulating. An individual own-occupation disability policy that covers you to age 65 is the financial foundation everything else rests on. Once that’s secured, layer in household employer liability coverage if you use paid help, then address life insurance gaps, and add LTC and critical illness coverage as budget permits.

Sources

- AARP & National Alliance for Caregiving, Caregiving in the U.S. 2025

- AARP, New Report Reveals Crisis Point for America’s 63 Million Family Caregivers (2025)

- U.S. Bureau of Labor Statistics, Eldercare in the United States (2025)

- KFF, Medicaid’s Home Care Support for Family Caregivers in 2025

- Centers for Medicare & Medicaid Services, Home Health Services Coverage

- Nebraska Department of Insurance, Insurance Considerations for Caregivers

- U.S. Department of Veterans Affairs, Family and Caregiver Health and Disability Benefits

- Administration for Community Living, National Family Caregiver Support Program