Fact-checked by the Smart Insurance 101 editorial team

The Verdict

Specialized classic car insurance coverage is worth it the moment your vehicle’s market value exceeds what a standard policy would pay on a total loss. That threshold is typically $10,000 above book value. It is not worth the extra effort for a driver-quality car you use daily, since usage-based eligibility rules will disqualify it anyway.

The single factor that determines whether you are adequately protected is not your premium, it is the valuation method your policy uses. A standard auto policy pays actual cash value (ACV), which assumes your car depreciates every year. For a classic that gains value, that assumption is wrong by design. Standard car insurance policies were built around daily drivers, not 1967 Mustang fastbacks that have appreciated 47% cumulatively from 2019 to 2025 according to the Hagerty Vehicle Rating index. That gap is where losses happen.

The global classic car insurance market hit $9.4 billion in 2025, and the majority of that growth is being driven by owners who finally understand the exposure a standard policy leaves open. If your car is already worth more than it was when you bought it, this decision is urgent.

| Factor | Reasons to Get Specialized Classic Car Insurance Coverage | Reasons to Stay on Standard Auto |

|---|---|---|

| Valuation Method | Agreed value pays 100% of the insured amount, no depreciation deduction | ACV pays market value minus depreciation, which undercuts a rising asset |

| Payout on Total Loss | Hagerty Guaranteed Value policies include sales tax in the payout | Standard policies exclude taxes and fees; you absorb those costs |

| Premium Cost | Carriers like Hagerty, Grundy, and American Collectors charge 40–60% less than standard auto rates | No eligibility hurdles, but you pay full standard-use premiums |

| Parts and Repairs | OEM or fabricated equivalent parts; your choice of specialist shop including out-of-state | Insurer selects repair shop; may substitute aftermarket or non-original parts |

| Coverage Growth | Inflation guard and mid-term reappraisal options let coverage rise with the market | Insured value is static or falls; no mechanism to track appreciation |

| Spare Parts | Spare parts inventory coverage available; protects NOS components and stockpiled pieces | Parts stored off the vehicle are typically excluded entirely |

| Use Restrictions | Low mileage caps (often 1,000–6,000 miles/year) reflect actual collector-car use | No mileage limit, but no premium credit for limited use either |

| Event Coverage | Car show, rally, and transit coverage included or available as an endorsement | Competitive events typically excluded; transit on a trailer may not be covered |

Key Takeaways: Specialized Classic Car Coverage Is Likely the Right Move If You Can Check Most of These

- Your vehicle is at least 15–25 years old (carrier thresholds vary; Hagerty and Grundy typically start at 25 years, while American Collectors Insurance accepts vehicles 15 years and older)

- The car’s current market value is at least $10,000 above what a standard ACV policy would pay on a total loss

- You drive it fewer than 6,000 miles per year and store it in an enclosed garage when not in use

- You have a daily driver for regular commuting, so the classic is not your primary transportation

- You have documentation of the car’s value: a recent independent appraisal, auction comparables, or a certified valuation report within the last 12 months

- Your vehicle has had significant restoration work or contains NOS (new old stock) parts with documented replacement cost above $2,500

- You plan to attend car shows, club events, or transport the vehicle on a trailer within the next year

Why Standard Auto Insurance Leaves Appreciating Classics Exposed

A standard auto policy calculates your total-loss payout using actual cash value, meaning the insurer estimates what your car would sell for on the open market, then subtracts depreciation. That math works for a 2022 Honda Accord. It does not work for a vehicle whose value has been climbing for a decade.

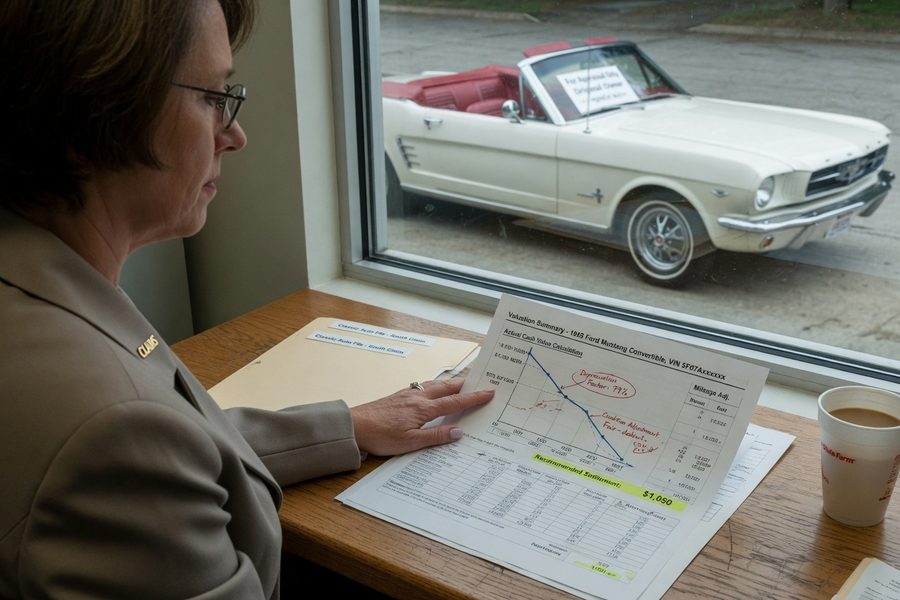

The problem goes deeper than the headline payout number. Standard carriers assume depreciation is happening even when it is not. If your 1970 Chevelle SS is appraised at $85,000 today but your standard policy carries it at an ACV of $48,000, a total loss pays you $48,000, and you lose $37,000 of real market value in an instant. That gap is not recoverable.

The repair situation is equally problematic. Standard insurers can direct you to any shop in their network and substitute aftermarket parts without your consent. For a collector vehicle, a non-original part can reduce show eligibility, lower auction value, and violate the terms of a future buyer’s own classic policy. Chubb and specialty carriers explicitly guarantee your choice of repair facility, including out-of-state specialists, and require OEM or fabricated-equivalent components. Standard policies offer no such guarantee.

State insurance regulators, including departments operating under the National Association of Insurance Commissioners (NAIC), have long required that ACV settlements reflect fair market value, but they do not require insurers to account for appreciation. That regulatory gap is precisely what specialty classic car programs are designed to fill.

Eligibility Rules: Does Your Vehicle Actually Qualify?

Most classic car policies require the vehicle to be at least 15 to 25 years old, garaged in an enclosed structure, and used exclusively for pleasure rather than daily transportation. Miss any one of those three, and you may be denied coverage or have a claim disputed.

Age thresholds differ by carrier. Hagerty Insurance Agency, which insures approximately 1.7 million vehicles globally, generally requires vehicles to be 25 years old. American Collectors Insurance starts at 15 years. Grundy Worldwide also applies a 25-year threshold in most states. The DVLA in the UK applies its own definition: 415,257 historic classic cars were registered in the UK in 2024, most of them meeting a 30-year age threshold for MOT exemption as well. In the United States, the Insurance Information Institute (III) notes that definitions of “classic” and “antique” vary by state, which can affect both titling and insurance eligibility.

Restomods, vehicles with significant aftermarket upgrades beyond their original specifications, are treated differently. A stock 1969 Camaro fits neatly into most classic programs. The same car with a modern LS3 swap, custom suspension, and a carbon fiber interior may be reclassified by some carriers as a custom or modified vehicle, requiring a separate endorsement or a different program entirely. If your vehicle has been substantially upgraded, get a written statement from your carrier confirming those modifications are covered before you assume they are. This is one gap most standard classic car policy articles overlook entirely.

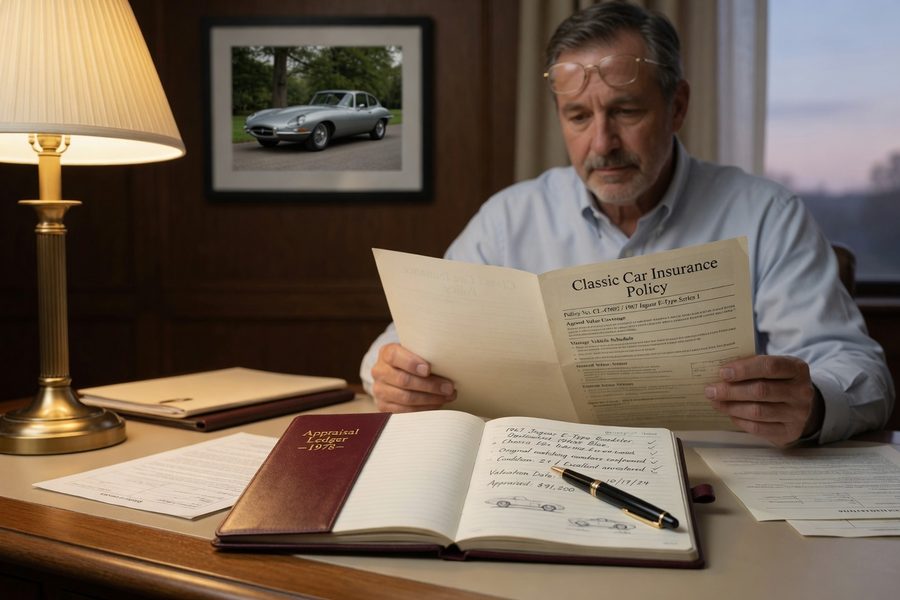

Agreed Value Coverage Locks In Real Protection

Agreed value coverage is the single most important feature in any classic car policy. Unlike stated value, which sounds similar but gives the insurer discretion to pay less, agreed value means both parties sign off on a specific dollar amount at policy inception, and that is exactly what gets paid on a total loss, no negotiation.

Agreed value coverage currently accounts for 34.2% of the global classic car insurance market in 2025, making it the most widely used valuation method in the specialty segment. For good reason: it eliminates the single largest source of post-claim disputes. Grundy states that coverage value is never reduced for the life of the policy, and many of its plans include an inflation guard plus a $0 deductible in most states. Hagerty’s Guaranteed Value program goes further, including sales tax in the total-loss payout, something most stated-value alternatives do not do.

Here is a real-numbers example. Say your agreed value is $75,000 and your state charges 8% sales tax on vehicle purchases. A Hagerty-style policy that includes sales tax pays you $81,000 ($75,000 × 1.08), enough to actually replace the car. A stated-value policy that excludes tax pays $75,000, leaving you $6,000 short before you have even started shopping. That delta grows proportionally as values rise.

Establishing the agreed value requires documentation: a certified independent appraisal, recent auction comparables from platforms like Bring a Trailer or Mecum Auctions, and photographs. Carriers will not simply take your word for it. Budget $200–$500 for a qualified appraiser, and treat that cost as part of your insurance expense. It is the foundation everything else rests on.

Updating Coverage as Market Values Continue to Rise

Setting your agreed value once and forgetting it is the most common mistake classic car owners make after getting properly insured. With North American collector cars up 47% cumulatively since 2019, a policy written three years ago can already be significantly behind the market.

Some carriers include an automatic inflation guard that adjusts your insured value by a fixed percentage each year, typically 2–4%. That is better than nothing, but it will not keep pace with a vehicle in a hot segment. A first-generation Ford Bronco or an air-cooled Porsche 911 from the early 1970s can jump 15–20% in a single year when demand spikes. An inflation guard of 3% does not close that gap.

The right protocol is to submit a new appraisal or market data to your carrier at least every two to three years, or immediately after a significant auction sale in your vehicle’s segment sets a new comparable. Most carriers allow mid-term policy endorsements to raise the agreed value; you will pay a slightly higher premium for the remainder of the term, but the math almost always favors doing it. Document every upgrade, restoration, or rare part addition with receipts, photographs, and mileage records. Those records are your negotiating material when you ask for a higher insured value.

If you are building a collection, consider how your classic car policy interacts with your broader financial picture. High-value collections can intersect with umbrella liability coverage, which provides excess protection if a guest is injured at an event where the vehicle is displayed. It is worth asking your broker whether a personal umbrella policy layered over your classic car coverage makes sense once your collection exceeds $250,000 in total agreed value. The Insurance Information Institute recommends reviewing all specialty coverage annually against current replacement cost, a standard that applies directly to appreciating collector vehicles.

Specialized Add-Ons, Cost Structure, and What You Are Actually Paying For

Premium costs for classic car coverage run 40–60% lower than standard auto insurance, according to data from Hagerty, Grundy, and American Collectors Insurance, and that discount is structural, not promotional. It reflects lower mileage exposure, better storage conditions, and an owner demographic with strong driving records. A vehicle worth $75,000 might cost $500–$900 per year to insure under a classic program versus $1,200–$1,600 under a standard policy.

The add-ons worth paying attention to: spare parts inventory coverage protects NOS components and stockpiled period-correct pieces stored off the vehicle, which a standard policy completely ignores. Trip interruption coverage reimburses hotel and towing costs if the vehicle breaks down more than a set distance from home, often 100 miles. Car show and transit coverage extends protection when the vehicle is displayed, trailered, or transported to an event. Most specialist carriers include several of these as standard features rather than optional riders.

One honest caveat: classic car policies are not well-suited to owners who want flexibility. Mileage caps are real, and exceeding them can void a claim. Storage requirements are real too, if you park the car in an unenclosed space and it is damaged, the carrier may deny coverage based on the policy conditions. The Federal Trade Commission (FTC) advises consumers to read all policy conditions before binding, particularly exclusions tied to vehicle use and storage, which is especially relevant for specialty products like classic car coverage. For a broader look at how policy structure affects what you actually collect at claim time, the true cost of insurance goes beyond the premium you pay each year.

Multi-vehicle discounts are available from most specialty carriers if you insure more than one classic under the same policy. American Collectors Insurance and Hagerty both offer collection-level policies that can cover five or more vehicles under a single agreed-value umbrella with one deductible. For serious collectors, that structure simplifies administration and often reduces total premium by another 10–15%. If you are also comparing rates across carriers, a structured car insurance quote comparison will help you line up apples-to-apples terms before committing.

Who Should and Who Should Not Get Specialized Classic Car Insurance Coverage

Good candidates

Owners with appreciating vehicles and clear documentation of value above standard book price are the obvious fit, but a few specific profiles make the case even more plainly.

- An owner of a restored muscle car or pre-1980 European sports car with a current appraisal above $25,000 and fewer than 3,000 miles driven per year

- A collector insuring multiple vehicles, where a collection-level policy from Hagerty or American Collectors offers a single agreed-value umbrella at reduced total cost

- An owner of a restomod with significant documented upgrades, custom engine swap, period-correct interior restoration, where aftermarket parts represent more than $15,000 in replacement cost

- Anyone who regularly attends car shows, auctions like Mecum or Barrett-Jackson, or rallies where the vehicle is trailered or displayed, since standard policies typically exclude those events entirely

- An estate holding a classic vehicle as part of a larger asset portfolio, where agreed value and clean title protection simplify future transfer or sale

Who should skip it

Classic car policies have real eligibility walls, and some vehicles or owners simply will not clear them.

- An owner who uses a classic as a primary vehicle and drives it more than 7,500 miles per year, most specialty carriers will decline or severely limit coverage

- A vehicle stored in a carport or driveway without an enclosed structure, which disqualifies it from most classic programs regardless of age or value

- An owner whose car is in rough, unrestored condition with a market value below $10,000 and no clear appreciation trajectory

- Someone who has not kept maintenance or restoration records, making it difficult to justify any agreed value above a standard ACV estimate

Frequently Asked Questions

What is the difference between agreed value and stated value in classic car insurance?

Agreed value means the insurer pays the full insured amount on a total loss, no deductions, no negotiation. Stated value gives the insurer the option to pay the lesser of the stated amount or actual cash value, which means you can still get shorted even after declaring a specific number. Always confirm in writing which type your policy uses before you bind coverage. The NAIC maintains a consumer resource center where you can verify your state’s specific rules on stated versus agreed value settlements.

How often should I update my classic car insurance coverage as the vehicle appreciates?

Every two to three years at minimum, and immediately after a significant comparable sale in your vehicle’s segment. An inflation guard of 2–4% per year will not keep pace with segments appreciating at 10–20% annually. Submit new appraisals or auction data to your carrier and request a mid-term endorsement to raise the agreed value.

Does a restomod or heavily modified classic qualify for specialty coverage?

It depends on the carrier and the extent of the modifications. Vehicles with mild upgrades often qualify under standard classic programs. Significant drivetrain swaps, custom fabrication, or non-period modifications may require a separate custom or modified vehicle endorsement from carriers like Chubb or Grundy. Get written confirmation from the carrier that specific modifications are covered before assuming they are.

Are spare parts and tools covered under a classic car policy?

Many specialty classic car policies include spare parts inventory coverage as a standard feature or available endorsement, protecting NOS components and period-correct parts stored off the vehicle. Standard auto policies exclude off-vehicle parts entirely. Confirm the per-item and aggregate limits with your carrier, since coverage caps vary significantly between programs. Hagerty and American Collectors Insurance both publish their spare parts coverage terms in their policy declarations, making direct comparison straightforward.

Sources

- DataIntelo (2025), Classic Car Insurance Market Report

- Heritage Insurance / DVLA FOI (2024), Heritage Classic Car Report 2025

- Hagerty (2025), By the Numbers: The Collector Car Market in 2025

- Insurance Information Institute, Auto Insurance Basics

- National Association of Insurance Commissioners (NAIC), Consumer Insurance Search

- Federal Trade Commission (FTC), Auto Insurance Consumer Guide

- Smart Insurance 101, Car Insurance Quotes Explained: Factors, Costs, and Tips