Fact-checked by the Smart Insurance 101 editorial team

Picture this: you’re sitting at a red light, running five minutes late, carrying an expired insurance card in your glovebox because the premium felt too steep this month. The light turns green, you go, and a distracted driver clips your rear bumper. That single moment triggers a chain of financial consequences most drivers have never actually priced out. The cost of driving uninsured isn’t just a ticket. It’s fines, potential lawsuits, license suspensions, impound fees, and a dramatic spike in future premiums that can follow you for years.

The scale of the problem is larger than most people assume. According to the Insurance Research Council’s 2025 report, roughly one in three U.S. drivers, 33.4%, was either uninsured or underinsured in 2023. That means the car next to you at that same red light has a one-in-three chance of not carrying enough coverage to pay your bills if they’re at fault. Uninsured drivers don’t just risk their own finances; they push costs onto everyone else through higher premiums industry-wide.

By the time you finish reading this guide, you’ll know exactly what penalties apply in different states, what happens after an accident without coverage, how lawsuits can reach into your paycheck years later, and what the realistic path back to affordable insurance looks like. The numbers here are specific, and some of them will surprise you.

Key Takeaways

- 15.4% of U.S. motorists were uninsured in 2023, according to the Insurance Research Council, and rates are higher in certain states.

- A single at-fault accident without insurance can expose you to an average bodily injury claim of $26,500+ and a property damage claim averaging $6,551, far exceeding years of typical premiums.

- First-offense fines range from $300 in Pennsylvania to over $700 in South Carolina, and that’s before reinstatement fees, court costs, or surcharges.

- Drivers caught without insurance typically face SR-22 requirements for 3 years, which can push premiums up by 50% to 200% above standard rates.

- Unpaid civil judgments from accidents don’t disappear, creditors can pursue wage garnishment and bank levies for years after the incident.

- Uninsured drivers generate an estimated $13+ billion in annual claims costs, a burden absorbed by insured drivers through higher premiums across every state.

In This Guide

- Immediate Penalties When You’re Pulled Over

- Vehicle Impoundment and Daily Storage Fees

- What Happens in an At-Fault Accident Without Coverage

- Lawsuits, Judgments, and Long-Term Financial Fallout

- SR-22 Requirements and Skyrocketing Future Premiums

- Hidden Costs Most Drivers Never Calculate

- Why the Risks Are Routinely Underestimated

- Getting Back to Covered: What It Actually Costs

Immediate Penalties When You’re Pulled Over

Here’s the thing: the fine itself is rarely the worst part of getting caught without insurance. It’s everything that follows. Still, the fine matters, and it varies dramatically by state, repeat offense, and whether your vehicle registration is also flagged as uninsured.

State-by-State Fine Ranges

In Pennsylvania, the Pennsylvania Department of Transportation is clear: a first offense for driving without insurance carries a minimum $300 fine, a three-month suspension of your vehicle registration, and a three-month suspension of your driver’s license. In South Carolina, the South Carolina DMV notes that uninsured vehicle owners face a $700 uninsured motorist fee plus reinstatement fees that can reach $400, a total that can easily exceed $1,100 before you’ve paid a single traffic court cost. Florida takes a slightly different approach: the Florida Department of Highway Safety and Motor Vehicles states that failure to maintain required insurance may result in license and registration suspension plus a reinstatement fee of up to $500.

Texas adds another layer. First-offense fines typically run $175 to $350, but the state also imposes a $250 annual surcharge for three consecutive years through its Driver Responsibility Program, that’s $750 in surcharges alone, on top of the initial fine and any court fees. When you add it up, a single first-offense traffic stop in Texas can cost a driver over $1,000 in fees across three years. That sum is close to 12 months of minimum-liability coverage in many Texas cities.

How Penalties Escalate With Repeat Offenses

A second offense almost always doubles or triples both the fine and the suspension period. Some states add mandatory community service hours, a criminal misdemeanor charge, or both. A misdemeanor conviction can follow you onto background checks for employment and housing applications, a consequence that goes well beyond the traffic fine.

In many states, simply owning an uninsured vehicle, even if you weren’t driving it, can trigger registration suspension and fines. The vehicle doesn’t need to be involved in an accident or pulled over for you to receive a penalty notice.

If you’re new to buying auto coverage and want to understand what types of policies exist before you shop, our guide on everything you need to know about car insurance covers the basics of liability, collision, and comprehensive policies in plain language.

Vehicle Impoundment and Daily Storage Fees

In many states, a traffic stop for no insurance doesn’t end with a ticket. Officers have the authority, and in some jurisdictions the obligation, to order your vehicle towed and impounded on the spot. Towing fees typically run $100 to $300, and daily storage charges average $25 to $75 per day depending on the facility and location. If you can’t get the insurance documentation sorted quickly, those storage fees compound fast. A vehicle held for 10 days in an urban impound lot could easily accumulate $500 or more in storage alone, on top of the tow charge and any administrative release fees the facility requires.

To reclaim the vehicle, most states require you to show proof of active insurance before they release it. That means you need to purchase a policy, have the card or electronic proof ready, and sometimes appear in person at both the impound lot and a DMV office. The entire process, from impound to release, can take two to five business days even when everything goes smoothly.

What Happens in an At-Fault Accident Without Coverage

Fines and impound fees hurt. An at-fault accident without insurance can be financially devastating. Here’s the thing: the other driver doesn’t absorb your mistake. You do, personally and out of pocket.

Property Damage Liability

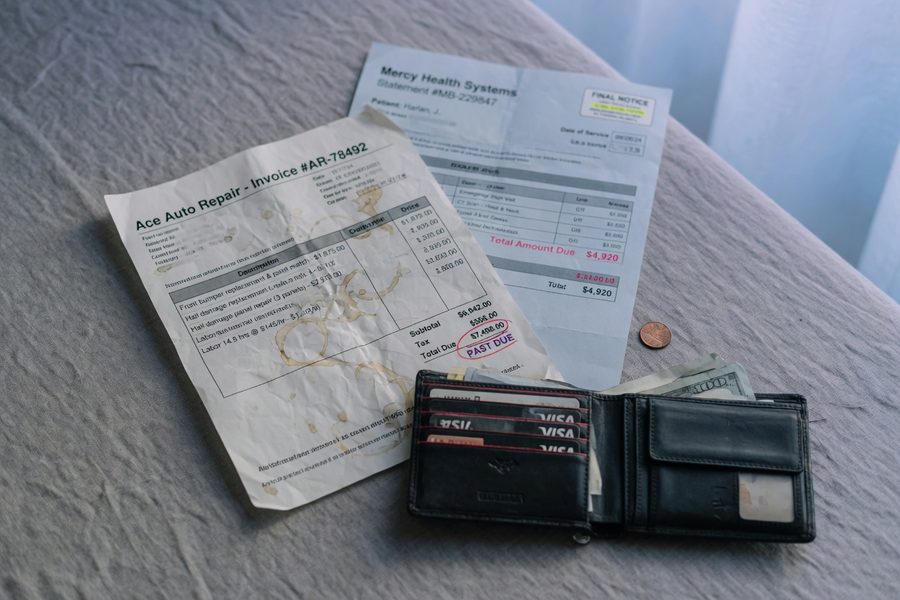

The average property damage liability claim in the U.S. runs around $6,551 based on insurance industry data. That covers a broad range of incidents: a bumper replacement on a mid-size sedan, a cracked windshield on an SUV, or a light-pole collision. But newer vehicles are more expensive to repair, and if you hit a vehicle worth $35,000 or more, the out-of-pocket exposure grows proportionally. Without insurance, every dollar of that repair bill comes directly from you.

The average bodily injury liability claim in the U.S. exceeds $26,500. A single accident where you injure another driver can trigger a claim that wipes out years of savings, while the annual cost of minimum-liability coverage in most states runs $500 to $1,200.

Medical Bills and Bodily Injury Claims

Bodily injury claims are where costs become genuinely life-altering. The average payout exceeds $26,500, but that figure represents a midpoint. A soft-tissue injury with physical therapy can cost $15,000 to $20,000. A broken bone requiring surgery easily clears $50,000. A serious accident with hospitalization can reach six figures.

In states with tort-based systems, where the at-fault driver is fully responsible for damages, an uninsured driver bears the complete financial exposure from the moment of impact. In no-fault states, each driver’s own insurance covers their initial medical costs, which sounds protective, but an uninsured driver in a no-fault state doesn’t have that cushion either. Their own medical bills go unpaid, and if the injury crosses the state’s threshold for a lawsuit, the at-fault driver still faces a civil claim. Either way, the uninsured driver loses.

Lawsuits, Judgments, and Long-Term Financial Fallout

When an uninsured driver causes an accident and can’t pay the bills voluntarily, the injured party has a straightforward legal remedy: sue. And in most states, they have several years (often two to four under the statute of limitations) to file that civil suit. A court judgment against you doesn’t expire quickly, it can remain collectible for 10 to 20 years in many states, and creditors can renew it.

Wage Garnishment and Bank Levies

Here’s what most articles skip over: a civil judgment doesn’t just sit on paper. Once a creditor has a judgment, they can pursue wage garnishment, a legal order directing your employer to withhold a portion of each paycheck and send it to the creditor. Federal law caps garnishment at 25% of disposable income (or the amount by which your weekly earnings exceed 30 times the federal minimum wage, whichever is less), but 25% of take-home pay is substantial. Creditors can also place liens on your bank account, forcing a freeze until the debt is satisfied.

These collection actions can follow you for years after the accident itself. Someone who caused a crash at 28 and never settled the judgment might find their wages garnished at 35. The injury victim also has options like placing a lien on any real property you own, which blocks a home sale or refinance until the debt is cleared.

Bankruptcy does not automatically discharge civil judgments from car accidents, especially those involving gross negligence. Consult a bankruptcy attorney before assuming that filing will wipe out accident-related debt.

Our related post on why lawsuits are quietly getting more expensive covers how rising litigation costs are affecting liability claims broadly, an important backdrop for understanding why accident judgments are climbing.

Credit Damage From Unpaid Judgments

Unpaid civil judgments, collection accounts, and wage garnishment orders all create a paper trail that affects creditworthiness. A significantly damaged credit score raises costs on car loans, mortgages, and even some rental applications. The financial damage from one uninsured driving incident can reshape what you pay for borrowing money for a decade.

SR-22 Requirements and Skyrocketing Future Premiums

After a conviction for driving without insurance, most states require the driver to file an SR-22 certificate, a document your insurer files with the state as proof you’re maintaining continuous liability coverage. It isn’t a separate policy; it’s a filing attached to your existing one. The problem is what it signals to insurers about your risk profile.

How Long SR-22 Lasts and What It Costs to File

Most states require SR-22 filing for three years from the date of conviction or license reinstatement. The filing fee itself is relatively small, typically $25 to $50. The real cost is the rate increase it triggers. Insurers treat an SR-22 requirement as a high-risk marker, and premium increases of 50% to 200% above your prior rate are common. If you were paying $100 per month before the conviction, you might pay $150 to $300 per month once the SR-22 is in place.

Here’s a straightforward example: a driver previously paying $100 per month ($1,200 per year) who now pays $200 per month ($2,400 per year) incurs an extra $1,200 annually. Over three years of mandatory SR-22 coverage, that’s $3,600 in additional premium costs, from a single traffic stop. That’s before factoring in the original fine, reinstatement fees, or any accident costs.

What Happens If Coverage Lapses

If your policy lapses during the SR-22 period, even for one day, your insurer is required to notify the state immediately. The state then typically reinstates your suspension, and your three-year SR-22 clock may restart from zero. This is not a technicality insurers overlook. It happens, it costs, and it extends the financial penalty by years.

If you’re shopping for coverage after a lapse or SR-22 requirement, compare quotes from at least four insurers, rates for high-risk drivers vary far more than rates for clean-record drivers. Our step-by-step guide to car insurance quote comparison walks through exactly how to do this efficiently.

Hidden Costs Most Drivers Never Calculate

The fines and lawsuit exposure are obvious in hindsight. What most drivers don’t tally in advance are the indirect costs that accumulate while their license is suspended.

Lost Wages and Transportation Expenses

A three-month license suspension means three months of arranging alternative transportation, rideshares, buses, carpools, or borrowing a vehicle from someone whose insurance covers permissive use. For a driver who earns $18 per hour and misses 10 hours of work due to court dates, DMV appointments, and impound pickups, that’s $180 in direct lost wages before the suspension even starts. During the suspension itself, rideshare costs to commute to a full-time job can easily run $300 to $600 per month in a mid-size city.

Employment and Housing Consequences

Jobs that require driving, delivery, sales, field service, caregiving, may not be available to someone without a valid license. A misdemeanor conviction for repeat uninsured driving can show up on background checks and disqualify applicants from certain positions. Some landlords now run criminal history checks as part of rental applications, which adds a housing dimension to what started as a traffic violation. These are real, documented consequences that don’t show up in the fine schedule posted on a state DMV website.

Why the Risks Are Routinely Underestimated

Ask most uninsured drivers why they’re driving without coverage, and the honest answer usually involves cost, insurance feels expensive, especially when the odds of getting caught on any given day feel low. That calculation is faulty for two reasons.

The Misconception of “Getting Away With It”

Enforcement has improved. Many states now use electronic insurance verification systems that flag uninsured vehicles automatically when license plates are scanned, which happens at routine traffic stops, toll booths in some jurisdictions, and even automated plate reader patrols. Drivers who haven’t been pulled over in years can receive a registration suspension notice in the mail because their plate was scanned and the system found no active policy on record.

According to the Insurance Information Institute citing IRC data, 15.4% of motorists nationwide were uninsured in 2023. In California alone, the uninsured driver rate reached 20.4%, ranking eighth highest nationally. High uninsured rates don’t reduce your risk of being caught; they increase the likelihood that any accident you’re in involves an uninsured party on both sides.

Uninsured drivers collectively generate an estimated $13+ billion in annual claims costs in the United States. Insured drivers absorb this through higher premiums, specifically, the uninsured motorist coverage component of their own policies.

The Effect on Everyone’s Premiums

The Texas Department of Insurance explains that uninsured and underinsured motorist coverage exists specifically to pay when you’re hit by someone who didn’t have insurance or didn’t have enough to cover your bills. Every insured driver pays for that coverage, and the higher the uninsured rate in a state, the more it costs. This is the mechanism by which uninsured drivers raise premiums for everyone, including people who are doing everything right. For a deeper look at what’s driving premium increases broadly, see our analysis of why insurance premiums are exploding.

Getting Back to Covered: What It Actually Costs

People sometimes avoid buying insurance because they believe their lapse history has made coverage unaffordable. That concern is real, SR-22 carriers and high-risk pools do charge more, but the cost of remaining uninsured is almost always higher than the cost of the elevated premium.

Minimum-Liability vs. SR-22 Carrier Pricing

A standard minimum-liability policy for a driver with a clean record runs roughly $500 to $900 per year in most states. After an uninsured driving conviction, that same profile might pay $900 to $1,800 per year with an SR-22 attached. That’s a meaningful increase, but compare it to the alternative: a single at-fault accident producing a $26,500 bodily injury judgment leaves you personally exposed to the full amount, collectible via garnishment for years.

| Scenario | Annual Cost | Worst-Case Exposure |

|---|---|---|

| Minimum liability (clean record) | $500 – $900/yr | Covered up to policy limits |

| SR-22 high-risk policy | $900 – $1,800/yr | Covered up to policy limits |

| Driving uninsured | $0 in premiums | $6,551+ property / $26,500+ bodily injury per incident, plus fines, fees, and SR-22 for 3 years afterward |

The California Department of Insurance also notes that the state’s Low Cost Automobile Insurance Program provides income-eligible drivers with liability coverage at reduced rates, a program that exists specifically to make compliance accessible for drivers who cite affordability as the barrier. Other states have similar programs, and it’s worth checking your state insurance commissioner’s website before assuming coverage is out of reach.

One Honest Caveat

Minimum-liability coverage does protect you from the worst financial outcomes, but it has a real limitation: it doesn’t pay for your own vehicle repairs or your own medical bills after an accident where you’re at fault. If you’re buying only the legal minimum to avoid fines, you’re still self-insuring your own losses. Full coverage, collision and comprehensive, costs more, but it closes that gap. Most financial advisors recommend at least modest collision coverage for vehicles worth over $8,000 to $10,000.

Some insurers offer payment installment plans monthly or quarterly that break up the annual premium into smaller amounts. Paying monthly costs slightly more in total, but it removes the barrier of a large upfront payment that causes some drivers to let their coverage lapse.

Your Action Plan

-

Check your current policy status today

Log into your insurer’s portal or call your agent to confirm your policy is active and that the correct vehicle is listed. If you’re not sure whether a lapse occurred, request a coverage history letter. A five-minute check prevents a $300 fine and a three-month suspension from a routine traffic stop.

-

Compare rates before you drop coverage, not after

If cost is driving the decision to go uninsured, get quotes from at least four insurers before canceling. Prices for the same coverage profile can vary by 40% to 60% between companies. Use an online comparison tool or contact an independent broker, our guide to reducing your auto insurance costs lists practical options for lowering your premium without eliminating coverage.

-

Understand what your state requires and what it enforces

Look up your state’s minimum liability requirements and its penalties for driving uninsured on the official DMV or Department of Insurance website. Know whether your state uses electronic verification, which increases the chance of a penalty even without being pulled over. States with no-fault systems have different but equally significant exposure for uninsured drivers.

-

If you have an SR-22 requirement, set up autopay immediately

A single missed payment that causes a coverage lapse resets your SR-22 period and triggers a new suspension. Autopay removes the human error from the equation. Contact your insurer to confirm they will notify you before any cancellation for non-payment, and set a calendar reminder as a backup.

-

If you caused an accident while uninsured, consult an attorney before making any payments or statements

A personal injury attorney or civil defense lawyer can assess whether a settlement is possible, whether any assets are genuinely protected under your state’s exemptions, and whether your exposure is less than what the claimant is requesting. Paying a partial amount without a formal release can sometimes extend the claim rather than end it. Get legal guidance first.

Frequently Asked Questions

What is the minimum fine for driving without insurance in the U.S.?

It depends on the state. Pennsylvania sets a minimum of $300 for a first offense. Texas first-offense fines start at $175 but add a $250 annual surcharge for three years. South Carolina can reach $700 plus reinstatement fees for vehicle owners. There is no single national minimum, each state sets its own schedule, and penalties scale with repeat offenses.

Can an uninsured driver be sued personally after an accident?

Yes, and that lawsuit can result in a civil judgment enforceable through wage garnishment, bank levies, or liens on real property. The injured party typically has two to four years to file suit depending on state statute of limitations, and a judgment can remain collectible for 10 to 20 years. Paying out of pocket at the time of the accident is the only way to prevent litigation, and that requires having the funds available immediately.

Will driving uninsured affect my credit score?

Not directly, traffic violations don’t appear on credit reports. But if an accident leads to a civil judgment, and that judgment goes unpaid, the creditor may sell the debt to a collection agency or pursue formal collection actions that do appear on credit reports. The indirect path from “uninsured traffic stop” to damaged credit is real but requires the additional step of an unpaid judgment or collection action.

How long does an SR-22 requirement last?

In most states, three years from the date of the underlying violation or license reinstatement. During that period, your insurer files continuous proof of coverage with the state. If coverage lapses even briefly, the insurer notifies the state, your license may be re-suspended, and the SR-22 period can restart. The filing fee itself is modest ($25 to $50), but the premium surcharge attached to SR-22 status is the significant cost.

Is minimum-liability insurance actually enough to protect me?

It protects you from the legal consequences of driving uninsured and covers the other party’s property damage and medical bills up to your policy limits. It does not cover your own vehicle damage or your own medical bills if you’re at fault. For drivers with vehicles worth more than $8,000 to $10,000, adding collision coverage is worth the additional cost. If you’re self-employed and depend on your vehicle for income, the gap between minimum-liability and fuller coverage is even more significant, our guide for self-employed workers covers the broader coverage picture for independent workers.

Do no-fault states protect uninsured drivers differently?

No-fault states require each driver’s own insurer to cover their initial medical expenses regardless of who caused the crash. An uninsured driver in a no-fault state doesn’t have that protection because they have no insurer. They absorb their own medical costs out of pocket and still face civil liability if the other party’s injuries exceed the state’s threshold for a tort claim. No-fault rules reduce litigation for insured drivers; they don’t benefit uninsured ones.

Can I get affordable insurance after a lapse in coverage?

Yes, though it takes more shopping. Rates after a lapse or SR-22 requirement are higher, but they vary significantly by insurer. Some specialty high-risk carriers offer competitive rates for drivers rebuilding their records. States like California also have low-income assistance programs, the California Low Cost Automobile Insurance Program, that provide basic liability coverage to income-eligible drivers at reduced rates. After three years of clean SR-22 compliance, most drivers can return to standard market rates.

Sources

- Florida Department of Highway Safety and Motor Vehicles, Insurance Requirements

- Pennsylvania Department of Transportation, Insurance Law FAQs

- South Carolina Department of Motor Vehicles, Facts About Driving Uninsured

- Texas Department of Insurance, Uninsured and Underinsured Motorist Coverage

- California Department of Insurance, Low Cost Automobile Insurance Program

- Insurance Information Institute, Facts and Statistics: Uninsured Motorists

- Insurance Research Council, One in Three Drivers Are Either Uninsured or Underinsured (2025)

- California Uninsured and Underinsured Driver Statistics, IRC 2025 Data

- Smart Insurance 101, Liability Insurance: Why Lawsuits Are Quietly Getting More Expensive

- Smart Insurance 101, Insurance Premiums Are Exploding: Here’s Why

- Smart Insurance 101, Step-by-Step Guide to Car Insurance Quote Comparison

- Smart Insurance 101–9 Ways to Reduce Your Auto Insurance