Reviewed by the Smart Insurance 101 Editorial Team

Our Take

For most policyholders, the car insurance declarations page is the one document worth reading carefully every single renewal cycle. It is a legally recognized summary of your coverage, and errors on it, wrong driver names, outdated vehicle details, missing discounts, directly affect what you pay and whether a claim gets paid. The average bodily injury liability claim now runs $28,278, which means a coverage limit you misread could leave you personally exposed. The case for skipping this review is exactly zero; the case for skimming instead of reading closely is only valid if every field matches reality.

Auto insurance premiums are not abstract. The NAIC’s 2026 auto insurance database report puts the national average combined premium at $1,438 per insured vehicle in 2023, a figure most drivers pay without fully understanding what it covers. The declarations page is where that coverage is spelled out, one line at a time.

This article is for drivers who receive their policy documents and feel uncertain about what they are reading. The recommendation is straightforward: read the declarations page field by field, verify it against reality, and request a corrected copy before the policy period begins if anything is wrong.

Key Takeaways

- The declarations page is a legally recognized summary, not the full contract; the South Carolina Department of Insurance describes it as identifying the insured, covered risks, policy limits, and policy period.

- The average paid bodily injury liability claim reached $28,278 in 2024, according to the Insurance Information Institute, making it critical to verify your per-person and per-accident limits are actually what you requested.

- 47.1% of in-force auto policies were shopped at least once in the previous 12 months as of Q4 2025, per LexisNexis Risk Solutions, a rate that makes accurate limit comparisons across quotes more important than ever.

- A new declarations page is issued at every renewal and after any mid-term change; what I see consistently is that drivers treat the first copy they receive as permanent and never check the updated one.

- Multi-vehicle policies can carry different coverage levels per car on the same page; most drivers assume uniform coverage and are wrong, which is one of the gaps this article addresses directly.

What a Car Insurance Declarations Page Actually Is

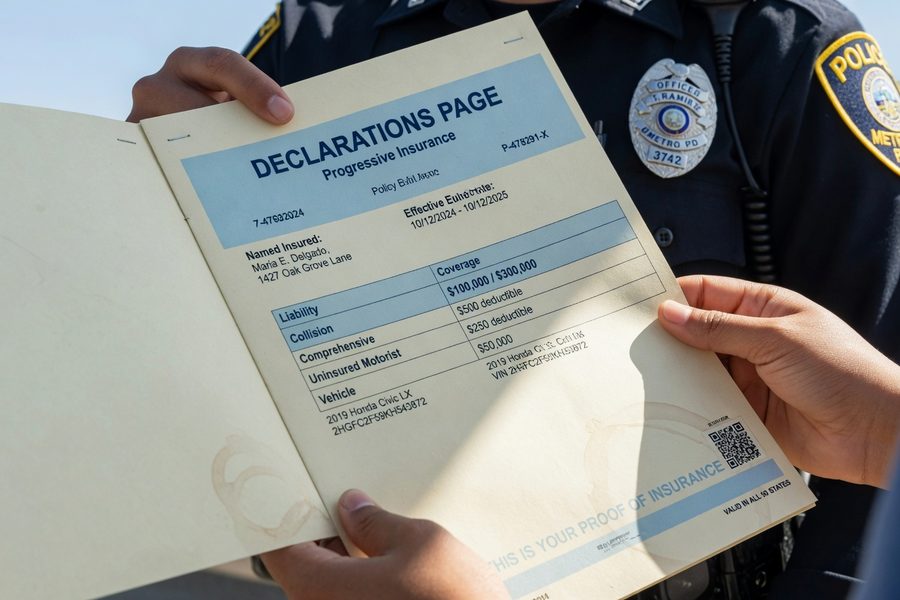

The declarations page is a policy summary, not the policy itself. That distinction matters. The full contract runs 20 to 40 pages and contains exclusions, conditions, and definitions that do not appear on the declarations page at all. The California Department of Insurance describes it as “a useful summary of the policy” and recommends reading it carefully, noting it “usually lists the insurance company name, coverages, deductibles, and insured vehicles.”

Think of it as a receipt. It confirms what you ordered, what it costs, and who it covers. What it does not do is tell you every scenario where coverage would be denied. That detail lives in the policy booklet or in attached endorsements. Progressive, Allstate, and Auto-Owners all note this explicitly in their policyholder materials: the declarations page is a snapshot, and the full policy governs in any dispute.

Why the declarations page has legal weight

Insurers and courts treat the declarations page as prima facie evidence of the coverage in force on a given date. Law enforcement accepts it as proof of insurance. Lenders reference it to verify that financed vehicles carry required collision and comprehensive coverage. If the page contains an error, say, a wrong vehicle year that affects your classification, that error can affect both your premium and your claim outcome until it is corrected in writing.

Where to Find Your Declarations Page and What Triggers a New One

Most insurers deliver the declarations page three ways: as the top sheet in a mailed renewal packet, as a downloadable PDF in your online account portal, or as a viewable document inside a carrier app. State Farm, GEICO, Progressive, and Allstate all surface it within one or two taps on their mobile apps. If you cannot find it digitally, call your agent and ask for the current declarations page to be emailed or mailed, that is a standard, no-cost request.

A new declarations page is generated every time your policy changes. Renewals trigger one automatically. So does adding or removing a vehicle, changing a driver, adjusting a coverage limit, adding an endorsement, or updating your garaging address. The Oklahoma Insurance Department advises verifying your personal information on the declarations page after receiving it, specifically because mid-term changes can introduce new errors.

What I see in practice: Readers who added a teenage driver mid-term often receive an updated declarations page weeks later, glance at the premium increase, and file it without checking whether the coverage limits or discounts changed. That is a mistake. Any updated declarations page should be reviewed line by line, not just for the new item that prompted the change.

One detail that often gets missed: if you request a change by phone, ask the agent to confirm when the updated declarations page will be available. Some carriers process changes same-day; others take 48 to 72 hours. Do not assume the coverage you requested is active until you see it confirmed on the document.

Policy Header Basics: Numbers, Dates, and Who to Call

The top section of the declarations page carries information that most people treat as boilerplate. It is not. The policy number is your claim reference, without it, an accident at 2 a.m. becomes a slower process. The effective and expiration dates confirm exactly when coverage applies. The Washington State Office of the Insurance Commissioner advises reviewing the declarations page specifically to make sure “all information is correct and all requested coverages are included”, starting with these header fields.

Verify the named insured exactly as it appears. A misspelled name or a missing co-insured (a spouse, for instance) can complicate a claim. Agent contact details in this section are your fastest path to corrections.

Drivers Listed and Vehicles Covered: Where Errors Cost the Most

Here’s the thing: the drivers listed on your policy determine who is rated, who is covered, and who is explicitly excluded. Named insureds have the broadest rights. Additional listed drivers are rated into the premium. Household members who are not listed may or may not have coverage depending on your state and policy language. An excluded driver is a different category entirely.

What an excluded driver endorsement actually means

An excluded driver endorsement removes a specific person from coverage, usually to lower the premium when a household member has a poor driving record. The practical consequence: if that excluded person drives your car and causes an accident, your insurer will likely deny the claim. What most policyholders do not realize is that the exclusion can sometimes affect coverage even when the excluded person is merely a passenger, depending on policy language and state rules. Review this section carefully before signing any exclusion endorsement.

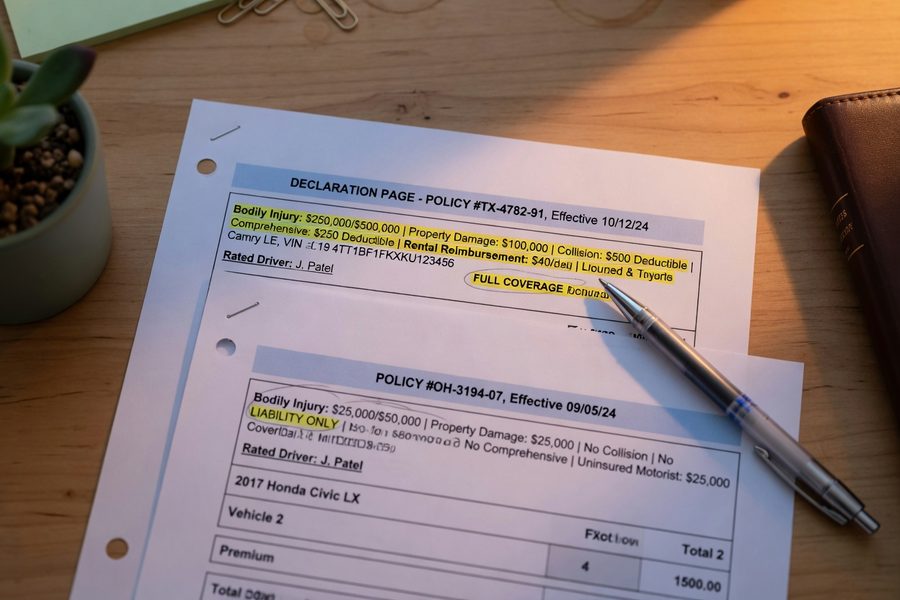

Multi-vehicle policies and per-car coverage differences

On a multi-vehicle policy, each vehicle gets its own coverage row. One car may carry full collision and comprehensive. Another, an older paid-off sedan, may carry liability only. This is intentional, and often appropriate, but it creates a gap when drivers assume all cars on the policy have the same protection. The full breakdown of car insurance coverages explains why those per-vehicle choices carry different risk profiles. Scan each vehicle row separately; do not assume uniformity.

Vehicle identification matters equally. The VIN, year, make, model, and garaging address on the declarations page must match reality. The Ohio Department of Insurance confirms that the declarations page normally includes vehicle-specific details and serves as the key reference document for both coverage questions and claims. If a VIN is wrong, a total loss settlement can be delayed while the insurer reconciles the discrepancy.

Also look for lienholder information. If you financed or leased a vehicle, the lender is typically listed as a loss payee or additional interest. That field tells you the insurer will issue any total loss check jointly to you and the lender. Missing or incorrect lienholder data can stall payment after a total loss.

Where this gets tricky: When readers are comparing quotes from different insurers, they often compare headline premium numbers without checking whether the coverage limits match. What we tell readers in this situation is to pull the declarations page from the current policy and use it as a template: align limits and deductibles line by line before any comparison means anything.

Coverages, Limits, Deductibles, and the Premium Breakdown

The coverage section is where the declarations page earns its keep. Each coverage type is listed with two numbers: the limit (the maximum the insurer pays) and, for physical damage coverages, the deductible (what you pay first). Reading them together is essential.

Liability limits and what the numbers mean

Liability limits appear in one of two formats. A split-limit policy like 100/300/100 means $100,000 per person for bodily injury, $300,000 per accident for bodily injury, and $100,000 for property damage. A combined single limit like $300,000 CSL covers bodily injury and property damage together up to that number. Given that the average paid bodily injury claim hit $28,278 in 2024 and the average property damage claim ran $6,770 according to the Insurance Information Institute, state minimum limits often leave a meaningful coverage gap. Minimum liability requirements vary by state; check whether yours is adequate for your net worth. Our post on why liability insurance costs are climbing provides useful context on why higher limits matter now more than they did five years ago.

Collision and comprehensive deductibles

A $500 collision deductible means you pay the first $500 of any covered repair; the insurer covers the rest up to the vehicle’s actual cash value. The NAIC’s 2026 report puts the average incurred loss per collision claim at $7,191 in 2022. On a $7,191 claim with a $500 deductible, you pay $500 and your insurer pays $6,691. On that same claim with a $1,000 deductible, you pay $1,000 and your insurer pays $6,191, a $500 difference in your pocket versus a likely premium savings of $50 to $150 per year depending on your profile. The math favors a higher deductible only if you have the savings to cover it.

Premiums, itemized by coverage

Most declarations pages break the total premium into line items per coverage: liability, collision, comprehensive, uninsured motorist, medical payments, and any endorsements. Discounts are often listed separately, either as a named line item or as a percentage reduction. Verify that every discount you were quoted appears here. Good driver discounts, multi-policy discounts, anti-theft device credits, if they were promised and do not appear, the insurer may have missed applying them.

For context on why premiums have moved sharply in recent years, our article on why insurance premiums are rising across the board covers the underlying cost drivers in detail. And if you are shopping after reviewing your current declarations page, the step-by-step guide to comparing car insurance quotes explains how to line up competing offers accurately.

| Coverage Type | Typical Limit or Deductible Range | Average Claim Cost (Source) |

|---|---|---|

| Bodily Injury Liability | $25,000/$50,000 state min to $500,000+ | $28,278 avg paid claim (III, 2024) |

| Property Damage Liability | $10,000 state min to $100,000+ | $6,770 avg paid claim (III, 2024) |

| Collision | $250–$2,000 deductible | $7,191 avg incurred loss (NAIC, 2022) |

| Comprehensive | $100–$1,000 deductible | Varies by peril; typically lower than collision |

| Uninsured Motorist | Mirrors liability limits in most states | Mirrors bodily injury claim costs |

What clients often miss: Readers frequently assume their uninsured motorist coverage matches their liability limits. It does not always. Some carriers default it to state minimum unless you explicitly request matching limits. Check both lines on the declarations page and confirm they reflect your actual request.

Where This Recommendation Falls Short

The advice to review your declarations page carefully at every renewal is correct for most people. The tradeoff is that for a small group of drivers, it creates false confidence.

Here’s the thing: the declarations page only shows what is covered. It does not show what is excluded. Reading it carefully and seeing “Comprehensive: $500 deductible” tells you that coverage exists, but it does not tell you that flood damage from a specific cause, or damage while the car is used for rideshare, may be excluded in the policy language. Those exclusions live in the policy booklet and in endorsements, not on the declarations page. Drivers who read only the declarations page and assume they understand their full coverage are in a better position than those who read nothing, but they are not fully informed.

The catch is also relevant for drivers with complex situations. If you have a rideshare endorsement, a rental car endorsement, or a named non-owner policy, the declarations page may list those additions in shorthand that is genuinely hard to interpret without the full endorsement form. In those cases, reading the declarations page is necessary but not sufficient.

The risk is compounded for leased vehicles. Leaseholders are required to carry specific limits, and the declarations page shows what limits are in force, but it does not flag whether those limits satisfy the lease agreement. You have to check the lease contract separately and compare it to what the declarations page shows.

The drawback for budget-focused shoppers is different: using the declarations page to compare quotes across insurers is the right method, but only if you are comparing identical limits. A policy from Insurer A at $1,200/year with 100/300/100 liability limits is not comparable to a policy from Insurer B at $900/year with 25/50/25 limits. The price difference reflects the coverage gap. Not for everyone is the simplest summary: drivers who carry state minimum limits, have no assets to protect, and rarely review their coverage may be making a rational choice, but they should know the exposure they are accepting, particularly given that bodily injury claims regularly exceed minimum liability thresholds.

How We Sourced This

This article draws from official state insurance department guidance published by Ohio, Oklahoma, Washington, California, and South Carolina, all of which maintain publicly accessible auto insurance consumer guides. Premium and claims data come from the NAIC’s 2026 Auto Insurance Database Report (covering policy year 2023 and 2022 claims data) and the Insurance Information Institute’s 2026 auto insurance fact statistics page (covering 2024 claims). Shopping behavior data comes from LexisNexis Risk Solutions’ 2026 Auto Insurance Trends Report covering Q4 2025. All state guidance documents were verified as current. No statistics in this article were extrapolated or estimated; every figure is reproduced exactly from the cited source.

Frequently Asked Questions

What is the difference between a declarations page and the full policy?

The declarations page is a one-to-three page summary listing your coverages, limits, deductibles, vehicles, and premium. The full policy is the legal contract, typically 20 to 40 pages, that contains exclusions, definitions, and conditions not shown on the declarations page. When there is a dispute, the full policy governs.

Does the declarations page serve as proof of insurance?

Yes, in most states. Law enforcement and lenders commonly accept it as evidence that a policy is in force for the listed vehicles. Some states also accept a digital version displayed on a phone. Keep a copy in each insured vehicle, either printed or saved in your carrier’s app.

What should I do if I find an error on my declarations page?

Contact your insurer or agent immediately in writing, email creates a paper trail. Request a corrected declarations page and confirm the effective date of the correction. Do not wait until renewal; errors in driver names, vehicle details, or garaging addresses can affect both your premium and a future claim.

Can different cars on the same policy have different coverage levels?

They can, and this is common. An older paid-off vehicle might carry liability only, while a financed vehicle carries full collision and comprehensive. Check each vehicle row separately on a multi-vehicle policy rather than assuming all cars share the same protection.

How do I use my declarations page to compare quotes from other insurers?

Pull your current declarations page and use the exact coverage types, limits, and deductibles as your comparison baseline. When requesting quotes, specify those same numbers to each insurer. A lower premium from a competing carrier is only meaningful if the limits and deductibles are identical to what you currently carry.

Why does the declarations page not list all my policy exclusions?

By design, the declarations page is a summary. Exclusions, conditions, and definitions are contained in the full policy form and any attached endorsements. Major carriers including Progressive and Allstate explicitly note this in their customer materials. If you want to know what is not covered, you need to read the full policy or ask your agent to walk you through the key exclusions for your specific situation.

Sources

- National Association of Insurance Commissioners, NAIC Releases 2022/2023 Auto Insurance Database Report

- Insurance Information Institute, Facts + Statistics: Auto Insurance (2026)

- LexisNexis Risk Solutions, Auto Insurance Trends Report (2026)

- Ohio Department of Insurance, Automobile Insurance Guide

- Oklahoma Insurance Department, Choosing Your Automobile Insurance Policy

- Washington State Office of the Insurance Commissioner, Auto Insurance Guide (March 2025)

- California Department of Insurance, Auto Insurance 101

- South Carolina Department of Insurance, Understanding Your Insurance Policy

- Smart Insurance 101, Everything You Need to Know About Car Insurance

- Smart Insurance 101, Step-by-Step Guide to Car Insurance Quote Comparison