Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

A high-deductible health plan (HDHP) offers lower monthly premiums but requires you to pay more before coverage begins. In 2025, the IRS sets the minimum deductible at $1,650 for self-only and $3,300 for family coverage. HDHPs are best for healthy, low-utilization individuals who can fund a Health Savings Account (HSA) and absorb early-year out-of-pocket costs.

Should you pay less every month and risk a large bill when you actually get sick? That is the central trade-off behind every high-deductible health plan pros cons conversation. An HDHP pairs lower monthly premiums with a higher threshold before insurance picks up most costs, and, 33% of covered workers are enrolled in one, according to Kaiser Family Foundation’s 2025 Employer Health Benefits Survey. That is a significant share of the workforce making a bet that they will stay healthy enough for the math to work out in their favor.

The honest answer is that HDHPs are genuinely good deals for some people and genuinely risky for others. This guide covers exactly who benefits, who gets hurt, how the Health Savings Account changes the calculation, and what questions to ask before you switch during open enrollment.

Key Takeaways

- HDHPs are available to 50% of private industry workers participating in medical care plans, per the U.S. Bureau of Labor Statistics (2024).

- The average annual premium for single HDHP coverage is $8,620 in 2025, per KFF’s 2025 employer survey.

- In 2025, the IRS sets HDHP out-of-pocket maximums at $8,300 for self-only and $16,600 for family coverage, per IRS Publication 969.

- HSA contribution limits reach $4,300 for individuals and $8,550 for families in 2025, per IRS Publication 969.

- 34% of covered workers are now in a plan with a general annual deductible of $2,000 or more for single coverage, per KFF (2025).

In This Guide

- What Exactly Is a High-Deductible Health Plan in 2025?

- The Main Draw: Lower Premiums and Where the Savings Are Real

- The Big Risk: What You Actually Owe Before Coverage Kicks In

- HSAs as a Safety Net: How Tax Advantages Change the Math

- Who Wins and Who Loses With an HDHP?

- Hidden Downsides: Delayed Care and Long-Term Costs

What Exactly Is a High-Deductible Health Plan in 2025?

An HDHP is any health plan that meets the IRS minimum deductible thresholds, making it eligible for pairing with a Health Savings Account. Per IRS Publication 969, that means a deductible of at least $1,650 for self-only coverage and $3,300 for family coverage in 2025. The out-of-pocket maximums cap at $8,300 and $16,600, respectively.

How HDHPs Differ From Traditional Plans

The structural difference is when coverage triggers. In a traditional HMO or PPO, you pay a copay or small coinsurance from the first visit, and the insurance company absorbs costs immediately. With an HDHP, you pay 100% of most non-preventive services until you clear the deductible. Preventive services, annual physicals, immunizations, certain screenings, remain covered at no cost regardless of whether you have met your deductible. That distinction matters, but it does not soften the early-year bill for a specialist visit, an imaging scan, or a prescription drug.

The median annual deductible for private industry HDHP participants reached $2,750 in 2024, per the Bureau of Labor Statistics. That is the number sitting between you and your insurer every January 1.

The IRS defines HDHPs not by plan type (HMO, PPO, or EPO) but strictly by deductible and out-of-pocket thresholds. A PPO can qualify as an HDHP if it meets those thresholds, meaning your plan type alone does not determine HSA eligibility.

The Main Draw: Lower Premiums and Where the Savings Are Real

Lower monthly premiums are the most visible benefit. The average annual premium for single HDHP coverage is $8,620 in 2025, per KFF’s 2025 Employer Health Benefits Survey. For comparison, the average for a traditional PPO plan for single coverage runs closer to $9,500 to $10,000 annually. The gap, roughly $880 to $1,380 per year, or about $73 to $115 per month, is real money that stays in your paycheck.

A Worked Example: Break-Even Analysis

Say your HDHP premium saves you $1,200 per year compared to a lower-deductible plan, and your HDHP deductible is $2,750 versus $500 on the traditional plan. That is a $2,250 higher exposure on the deductible side. At your premium savings rate, you need to stay below roughly $1,200 in additional out-of-pocket spending to come out ahead. If your annual medical costs total $300 in lab work and one doctor visit, you save $900 for the year. If you need an MRI and two specialist visits, you might spend $1,500 to $2,000 out of pocket, erasing the premium savings entirely. The break-even point depends entirely on how much care you use, and how predictable that amount is.

Employer HSA contributions shift this calculation in your favor. Many employers who offer HDHPs seed their employees’ HSAs with $500 to $1,500 annually. If your employer contributes $1,000 to your HSA, your effective deductible exposure drops by that amount, narrowing the real risk significantly.

The Big Risk: What You Actually Owe Before Coverage Kicks In

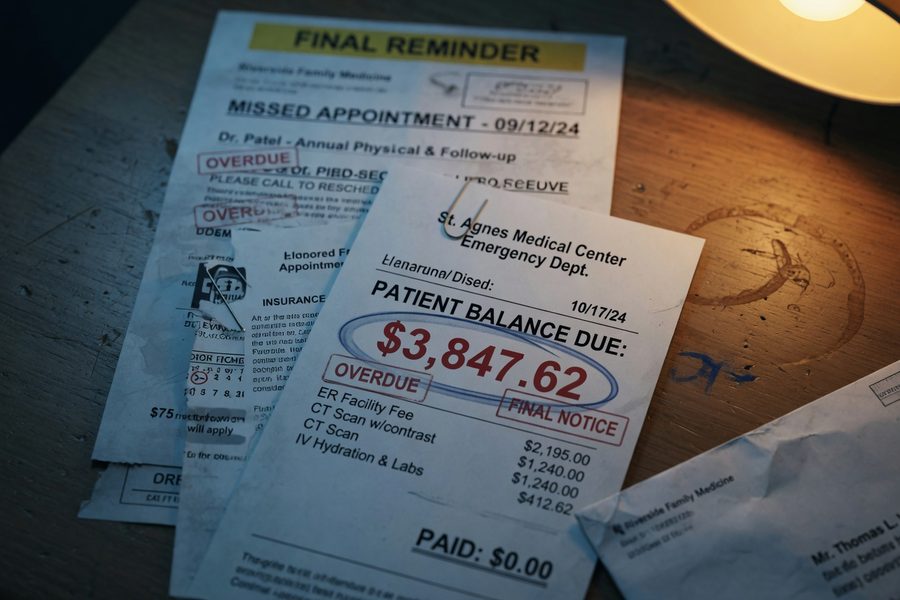

The deductible hits hardest in the first weeks of a new plan year. A single specialist visit, a round of imaging, or one urgent care trip can run $300 to $800 out of pocket before your insurer contributes a dollar. For someone managing a chronic condition, those costs can stack up fast enough to reach the full deductible by February or March.

The average general annual deductible for single coverage across all plan types was $1,886 in 2025, per KFF’s 2025 employer data. For HDHPs specifically, the figure runs higher. That is a meaningful cash-flow challenge if you do not have liquid savings to cover it. Understanding the full picture of what a deductible means versus an out-of-pocket maximum is essential before enrolling; our guide on the health insurance deductible vs. out-of-pocket maximum explains exactly how the two thresholds interact.

34% of covered workers in 2025 are enrolled in plans with single-coverage deductibles of $2,000 or more, per KFF’s 2025 Employer Health Benefits Survey. That threshold is high enough that most moderate illnesses will land entirely in the deductible window.

HSAs as a Safety Net: How Tax Advantages Change the Math

The HSA is the feature that makes an HDHP genuinely competitive, but only if you actually fund it. In 2025, you can contribute up to $4,300 as an individual and $8,550 for family coverage, per IRS Publication 969. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. That triple tax benefit is not available with any other savings vehicle tied to healthcare costs.

How the HSA Reduces Your Real Risk

Think of the HSA as a dedicated emergency fund that the IRS subsidizes. If you contribute $4,300 and you are in the 22% federal tax bracket, your tax savings alone amount to roughly $946 for the year. Pair that with an employer contribution of $1,000 and your $1,200 in premium savings, and you have offset a substantial portion of that $2,750 deductible before you see a single medical bill. The math still does not work for everyone, but for healthy employees with steady income and access to an employer HSA match, the HDHP plus HSA combination is often the strongest financial option available.

Unlike a Flexible Spending Account (FSA), HSA balances roll over indefinitely. Funds invested in index funds or money market accounts inside the HSA grow tax-free, making the account useful as a long-term healthcare reserve or even a secondary retirement account for those over 65, when withdrawals for any purpose are taxed like a traditional IRA.

| Feature | HDHP + HSA (2025) | Traditional PPO (Typical 2025) |

|---|---|---|

| Avg. Single Premium (Annual) | $8,620 | ~$9,700 |

| Min. Deductible (IRS / Typical) | $1,650 (IRS min); median ~$2,750 | $500–$1,000 |

| Out-of-Pocket Max (Single) | $8,300 | $7,000–$9,000 |

| HSA Eligible | Yes, up to $4,300/yr | No |

| Preventive Care Coverage | 100%, no deductible | 100%, no deductible |

| Specialist Copay Before Deductible | None, full cost until deductible met | $40–$60 copay typical |

| Best For | Healthy, low-utilization enrollees | Chronic conditions, predictable high use |

Who Wins and Who Loses With an HDHP?

Healthy, younger enrollees with low annual healthcare utilization typically come out ahead. The premium savings accumulate, HSA contributions grow tax-free, and the deductible rarely gets reached. This group includes people in their 20s and early 30s who primarily use preventive services, or higher-income individuals who can absorb a large deductible without financial stress and benefit from the HSA’s tax shelter.

Where HDHPs Create Real Financial Strain

People with chronic conditions face a different reality. Someone managing Type 2 diabetes, asthma, or rheumatoid arthritis may reach their deductible within the first quarter of the year through prescription costs and specialist visits alone. Research cited by Kaiser Family Foundation consistently shows that high-deductible exposure correlates with reduced medication adherence and skipped follow-up appointments among lower-income and chronically ill populations. The premium savings do not compensate for that financial barrier when you need regular care.

Self-employed workers face a compounded challenge. Without an employer HSA contribution, the full funding burden falls on them, and irregular income can make it difficult to front-load the account before medical needs arise. Our guide to health insurance plans for self-employed workers covers these trade-offs in more depth.

Before enrolling in an HDHP, calculate your expected annual medical spending using last year’s explanation of benefits (EOB) statements. If your projected out-of-pocket costs plus the HDHP premium exceed what you would pay on a traditional plan all-in, the HDHP is likely the wrong choice for you.

Hidden Downsides: Delayed Care and Long-Term Costs

The most significant risk of HDHPs does not show up in a premium comparison, it shows up months or years later. Studies consistently link high-deductible exposure to deferred care, particularly among lower-income enrollees and those managing ongoing health conditions.

When Skipping Care Costs More in the End

When a patient skips a $300 follow-up appointment to avoid hitting their deductible, that decision can lead to a $3,000 emergency room visit later. The Centers for Medicare and Medicaid Services has acknowledged these access barriers in its 2026 guidance, expanding hardship exemptions to allow more consumers to access catastrophic coverage options that better fit their financial situation. The broader concern is that cost-sharing at the deductible level discourages early intervention, exactly the care that is cheapest to provide and most effective clinically.

Rising medical inflation compounds this risk. As we covered in our piece on medical coverage shrinking as costs explode, provider prices continue to outpace wage growth, which means the real cost of reaching a deductible grows every year. Surprise billing protections offer some relief for emergency and out-of-network situations, but they do not apply to in-network deductible spending, where most HDHP exposure actually occurs.

One honest concession: even for people who are good candidates for an HDHP, the plan requires financial discipline that not everyone can sustain. Consistently funding an HSA, maintaining a cash reserve equal to your deductible, and resisting the urge to skip necessary care are real behavioral demands. The tax advantages are genuine, but they only materialize if you follow through.

Frequently Asked Questions

What qualifies as a high-deductible health plan in 2025?

A plan qualifies as an HDHP in 2025 if its annual deductible meets IRS minimums of $1,650 for self-only or $3,300 for family coverage, per IRS Publication 969. The plan must also cap out-of-pocket costs at no more than $8,300 (self-only) or $16,600 (family). Meeting these thresholds is what makes the plan eligible for pairing with an HSA.

Can I open an HSA if my employer does not offer one?

Yes, as long as you are enrolled in a qualifying HDHP, you can open and fund an HSA independently through a bank, credit union, or investment firm. You do not need employer sponsorship to open the account, though you do lose out on any employer seed contributions your company might otherwise provide.

Are prescription drugs covered before the deductible on an HDHP?

Generally, no. Most HDHP plans apply prescription drug costs to the deductible, meaning you pay full contracted rates for medications until you meet it. Some plans carve out certain generic drugs from the deductible, but this varies by plan. Review the Summary of Benefits and Coverage (SBC) for your specific plan before assuming any prescriptions are exempt.

Who should avoid a high-deductible health plan?

People with chronic conditions requiring regular specialist visits or ongoing prescriptions, those with limited liquid savings, and lower-income households that could not absorb a $2,000-plus expense in early January are generally better served by a lower-deductible plan. The premium savings rarely offset the out-of-pocket exposure for high utilizers.

Does choosing an HDHP affect my options for other types of coverage?

Your health plan choice does not directly restrict life, dental, or property coverage. If you are comparing the full picture of what insurance costs and protects against, resources like our overview of insurance types and their benefits can help you see how health coverage fits alongside your other policies. Enrolling in an HDHP does make you ineligible for a general-purpose FSA, though a limited-purpose FSA for dental and vision expenses is still permitted.

Sources

- Internal Revenue Service, Publication 969: Health Savings Accounts and Other Tax-Favored Health Plans

- Kaiser Family Foundation, 2025 Employer Health Benefits Survey

- Kaiser Family Foundation, Policy Changes Bring Renewed Focus on High-Deductible Health Plans

- Centers for Medicare and Medicaid Services, Expanding Access to Health Insurance: Consumers Gain Access to Catastrophic Health Insurance Plans for 2026

- U.S. Bureau of Labor Statistics, High-Deductible Health Plans and Health Savings Accounts (2024)

- Smart Insurance 101, Health Insurance Deductible vs. Out-of-Pocket Maximum: What Is the Real Difference?