Fact-checked by the Smart Insurance 101 editorial team

The Verdict

Understanding prescription drug coverage tiers is worth the effort if your medication sits on Tier 3 or higher, where costs can jump from a $10 copay to 25–33% coinsurance on a drug costing hundreds per fill. It matters less if all your prescriptions are generics on Tier 1 or Tier 2. The single biggest lever: check your plan’s formulary before open enrollment ends, not after you get a surprise bill at the pharmacy counter.

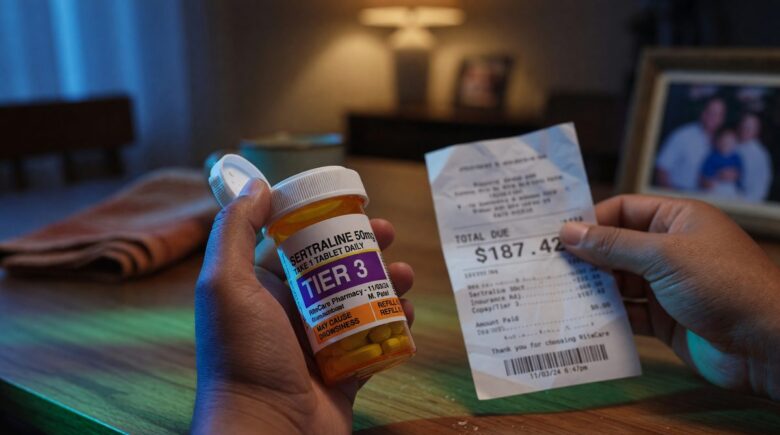

Why does a drug your doctor prescribed cost $180 at the pharmacy when you expected to pay $40? The answer almost always comes back to prescription drug coverage tiers, the system insurers use to rank medications by cost-sharing level, and the single factor that determines more of your out-of-pocket drug spend than your deductible, your premium, or even the drug’s list price. One statistic tells the story clearly: according to KFF’s 2025 analysis of Medicare Part D, 83% of Prescription Drug Plan enrollees are now in plans that charge coinsurance rather than flat copayments for preferred brand drugs, meaning your cost moves with the drug’s price, not a fixed dollar amount.

That shift matters right now because 2025 brought a meaningful restructuring of how both Medicare and commercial plans price drugs through tiers. If you haven’t checked where your specific medications land since last open enrollment, there’s a real chance your costs changed without any notice.

| Reason to Understand Your Tiers | Detail | Reason to Worry Less |

|---|---|---|

| Tier placement directly sets your cost | Tier 1 generics often carry $0–$10 copays; Tier 4/5 specialty drugs require 25–33% coinsurance | All your drugs are generic (Tier 1–2) |

| Plans can re-tier mid-year | Formulary updates tied to new generics or rebate changes can move your drug with limited notice | Your plan is stable and hasn’t changed formularies in two years |

| Coinsurance tiers are spreading fast | 76% of Prescription Drug Plan drugs were on coinsurance tiers in 2025, up from 69% in 2024 | Your plan still uses flat copayments on all brand tiers |

| PBM rebates decide preferred status | Two clinically similar drugs can land in completely different tiers based on manufacturer rebate contracts, not clinical merit | Only one medication in your drug class exists |

| Exceptions process can lower your cost | A formulary exception with a letter of medical necessity can move you to a lower tier if alternatives are documented as ineffective | A lower-tier alternative works as well for your condition |

| Specialty tier exposure is high | Specialty drugs (often Tier 4 or 5) drive a disproportionate share of total drug spend even though they represent a small share of all prescriptions | You take no specialty or biologic medications |

Key Takeaways

- Your medication is likely worth a tier review if it costs more than $50 per fill and sits on Tier 3 or higher on your current formulary.

- Check whether your plan uses coinsurance (a percentage of the drug’s price) rather than a flat copay on brand tiers, the distinction can mean hundreds of dollars annually.

- Pull your plan’s formulary document before open enrollment closes each year; formulary changes take effect January 1 without individual notification in most plans.

- If a lower-tier alternative exists for your condition, ask your prescriber whether it is clinically appropriate before assuming you must pay the higher tier cost.

- Request a formulary exception in writing if your doctor can document that Tier 1 or Tier 2 alternatives are contraindicated or have been tried and failed, plans are required to have an exceptions process under CMS formulary guidance.

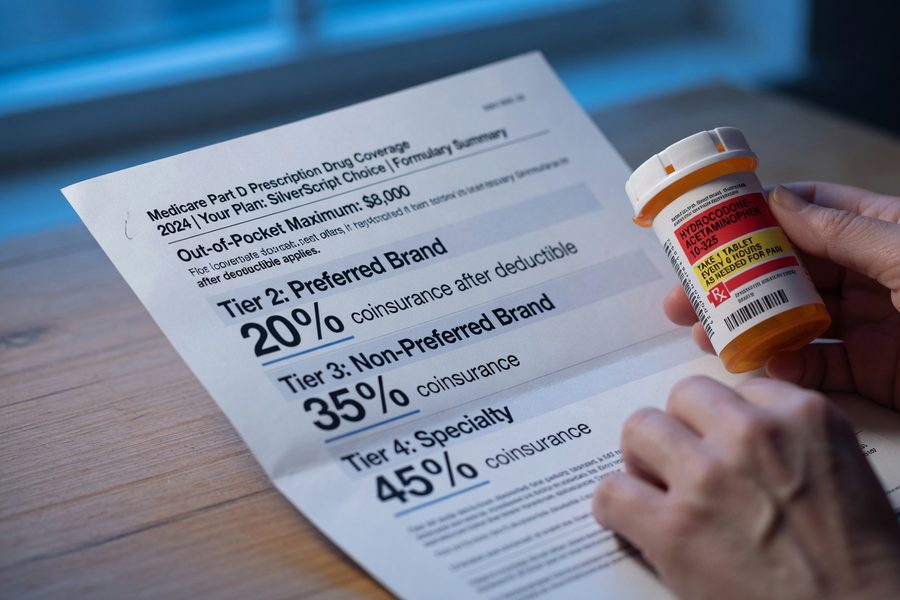

- If you are a Medicare beneficiary, confirm whether your plan charges a Part D deductible: 60% of MA-PD enrollees in 2025 are in plans that now include a Part D deductible, up from 21% in 2024.

- Biosimilars and new generics actively shift the tier landscape; a drug that was Tier 4 last year may now have a Tier 1 biosimilar equivalent on the same formulary.

What Prescription Drug Coverage Tiers Actually Mean

Tiers are not just a label. Each tier maps to a specific cost-sharing structure, either a flat copayment or a coinsurance percentage, and that structure determines what you hand over at the pharmacy counter every single month.

Most commercial and Medicare Part D plans use four or five tiers. Tier 1 covers preferred generics at the lowest cost, typically $0–$10. Tier 2 covers non-preferred generics or lower-cost brands, usually in the $15–$40 range. Tier 3 covers preferred brand-name drugs, often running $45–$100. Tier 4 covers non-preferred brands, frequently with coinsurance rather than a flat dollar amount. Tier 5, the specialty tier, handles the most complex and expensive medications, with coinsurance rates commonly set at 25–33% of the drug’s plan cost. On a specialty biologic priced at $8,000 per month, that percentage translates to $2,000 out of pocket before any additional cost protections kick in.

According to Medicare.gov’s explanation of how drug plans work, a drug in a lower tier generally costs the beneficiary less than one placed in a higher tier, a straightforward principle that becomes complicated when you realize the same drug can land in different tiers depending on which plan you’re enrolled in. Insurers are not using a shared standard; each plan negotiates separately with pharmacy benefit managers and manufacturers, producing different tier assignments for the same medication across competing plans.

Understanding this system sits alongside other coverage decisions. If you’re weighing plan types, our guide on HMO vs. PPO health insurance plans explains how network restrictions also affect which pharmacies will honor your tier-based cost sharing.

Why Your Drug Ended Up in a Higher Tier

Rebates, not clinical value, are frequently the deciding factor in whether a brand drug gets preferred or non-preferred status. This is the detail most plan summaries quietly omit.

Pharmacy benefit managers, or PBMs, large intermediaries like CVS Caremark, Express Scripts, and OptumRx, negotiate rebates with drug manufacturers on behalf of insurers. A manufacturer willing to pay a larger rebate can secure a lower tier placement for its drug even if a competitor’s product has a similar or slightly better clinical profile. The insurer’s net cost after that rebate may actually be lower for the preferred drug, which is how the arrangement gets justified. But from a patient’s perspective, the preferred drug may not be the one their doctor would have chosen on clinical grounds alone.

Step therapy requirements compound the problem. Many plans require patients to try and fail on a lower-tier alternative before the plan will cover the higher-tier drug, even when a prescriber believes the higher-tier option is clearly better for that patient. According to the CMS Part D Benefits Manual, Chapter 6, Part D sponsors must develop formulary tier structures using standard industry practices, designating Tier 1 as the lowest cost-sharing tier, and must review tier placement to avoid substantially discouraging enrollment. That last phrase carries real weight: plans cannot tier a drug so high that it effectively excludes people with certain conditions from enrolling.

Biosimilar entry is reshaping tiers in specific drug classes, though not as uniformly as patients might hope. A 2025 report from the U.S. Department of Health and Human Services Office of Inspector General found that 96% of Part D Prescription Drug Plans covered at least one of ten Humira biosimilars on their 2025 formulary. That’s meaningful progress. The catch: manufacturer rebates from AbbVie (Humira’s maker) have been substantial enough that some plans still place original Humira on a preferred tier alongside or above its biosimilars, rather than steering patients toward the lower-cost alternative. The biosimilar exists on the formulary, but tier placement may not make it cheaper.

The 2025 Coinsurance Shift: A Cost You May Not Have Seen Coming

Coinsurance tiers are now the norm in Medicare Part D, and they work very differently from the flat copays most people are used to.

When a plan charges a flat $45 copay for a Tier 3 drug, your cost is predictable regardless of the drug’s price. When a plan charges 25% coinsurance on the same tier, your cost moves with the drug’s negotiated price. For a $300 brand drug, that’s $75. For a $1,200 specialty drug, it’s $300. The difference between copay and coinsurance structures is one of the least-discussed cost traps in health insurance, and it’s spreading fast. According to Avalere Health’s 2025 formulary analysis, 76% of all drugs on PDP formularies are now on coinsurance tiers, up from 69% in 2024. For Medicare Advantage Prescription Drug plans (MA-PDs), the share jumped from 30% to 50% in a single year.

The practical impact: 28% of MA-PD enrollees are now in plans that charge coinsurance rather than copayments for preferred brand drugs, up from just 2% in 2024, per KFF’s 2025 analysis. If you were enrolled in an MA-PD plan last year and didn’t switch, there’s a real chance your preferred brand drug now triggers coinsurance instead of a flat dollar amount, with no change to the drug itself and minimal direct notification from your plan.

A quick example shows what this means in dollars. Suppose your Tier 3 preferred brand drug costs $400 per fill. Under a flat $50 copay, your annual cost for 12 fills is $600. Under 25% coinsurance on the same drug, your annual cost is $1,200, exactly double. That $600 annual gap is real money, and it appears not because your drug got more expensive but because your plan’s cost-sharing structure changed. This connects directly to the broader trend of medical coverage shrinking as costs explode nationwide, where cost-sharing shifts are quietly transferring more financial risk to patients.

Who Should and Who Should Not Prioritize Tier Research

Good candidates

Tier research pays off most for people whose prescriptions are expensive, chronic, or on the borderline between tiers.

- Anyone taking a brand-name or specialty drug who hasn’t reviewed their formulary since last open enrollment, tier assignments change annually and sometimes mid-year.

- Medicare Part D or MA-PD enrollees whose plans switched from copayments to coinsurance for brand drugs in 2025, a shift that affected a large share of the enrolled population.

- People managing chronic conditions like rheumatoid arthritis, multiple sclerosis, or diabetes who rely on biologics or brand medications where Tier 4/5 coinsurance creates real adherence pressure.

- Self-employed individuals and marketplace plan shoppers comparing plan options, where a drug that’s Tier 2 on one plan may be Tier 4 on another at the same premium. Our guide on health insurance for self-employed workers covers how to evaluate these trade-offs across plans.

Who should skip it

Not everyone needs to spend time on tier analysis, for some, the math simply won’t move.

- People whose only medications are well-established generics on Tier 1, their cost is already at or near the floor, and tier reviews won’t change that.

- Patients whose employer plan has a flat benefit design with identical copays across all non-specialty tiers, making tier placement irrelevant in practice.

- Individuals within a single-option plan environment, if your employer or state marketplace offers only one drug plan, comparing formularies across plans is academic.

Frequently Asked Questions

Why did my prescription cost more than my copay card said it would?

Your drug probably moved to a higher tier, or you’re now in the deductible phase where full drug costs apply before any cost-sharing kicks in. Plans can update formularies in ways that change your tier assignment mid-year, and many patients only discover this when the pharmacy rings up a different total. Pull up your plan’s current formulary online and search for your drug’s current tier status.

Can my insurance plan move my medication to a higher tier after I already enrolled?

Yes, plans can re-tier medications mid-year when lower-cost alternatives become available, such as a new generic or biosimilar entering the market. Medicare Part D plans are generally required to provide advance notice, but the window is limited and easy to miss. Outside of Medicare, commercial plan rules on mid-year formulary changes vary by state and plan type.

What is a formulary exception and how do I request one?

A formulary exception is a formal request to have a non-covered or higher-tier drug covered at a lower cost-sharing level. Your prescriber must submit a letter of medical necessity documenting that lower-tier alternatives were tried and failed, or are medically contraindicated. CMS requires Medicare Part D plans to have an exceptions and appeals process, and commercial plans typically offer similar procedures under their plan documents.

How do prescription drug tiers work differently in Medicare versus employer plans?

Medicare Part D plans follow CMS guidelines that designate Tier 1 as the lowest cost-sharing tier and set rules on how plans can structure specialty tiers, which limits some of the more aggressive tiering practices. Employer-sponsored plans, especially self-funded plans not subject to state insurance regulations, have more flexibility to design tiers, which means you may see non-standard structures like four-tier designs with very high coinsurance on Tier 4. Understanding your deductible versus out-of-pocket maximum is equally important here, since drug costs often count toward both.

Do biosimilars automatically cost less than the original biologic on my plan?

Not automatically. While biosimilars are designed to be lower-cost alternatives, tier placement depends on your plan’s specific formulary and the rebate contracts in place., most Medicare Part D plans do cover Humira biosimilars, but whether a biosimilar lands in a lower tier than the original brand depends entirely on how your plan structured its formulary that year. Always compare the specific tier of both options in your plan document before assuming the biosimilar is cheaper for you.

Sources

- Centers for Medicare & Medicaid Services, Formulary Guidance for Medicare Prescription Drug Plans

- Medicare.gov, How Medicare Drug Plans Work

- Centers for Medicare & Medicaid Services, Part D Benefits Manual, Chapter 6: Part D Drugs and Formulary Requirements

- KFF, Medicare Part D in 2025: A First Look at Prescription Drug Plan Availability, Premiums, and Cost Sharing

- Avalere Health, 2025 Part D Formularies Shift to More Coinsurance and Utilization Management

- U.S. Department of Health and Human Services Office of Inspector General, Most Medicare Part D Plans’ Formularies Included Humira Biosimilars for 2025

- Centers for Medicare & Medicaid Services, Prescription Drug Coverage Contracts