Fact-checked by the Smart Insurance 101 editorial team

The Verdict

A home inventory for insurance is worth doing if you own more than $10,000 in personal property, which covers most households. It is not optional if you live in a high-risk area for fire, flood, or severe weather. Skip it only if you rent with minimal belongings and carry a low personal property limit.

The single factor that separates a fast insurance claim from a drawn-out dispute is documentation. A home inventory for insurance gives your adjuster a verified list of what you owned, what it cost, and when you bought it, removing the guesswork that stalls settlements. According to the Texas Department of Insurance, not having one could delay your claims payment, because most insurance companies will ask for a detailed record of lost or damaged items before cutting a check.

That delay matters more now. Home replacement costs have surged, and insurers are scrutinizing personal property claims more closely. If you cannot prove you owned a $3,000 camera or a $1,500 laptop, you may not get paid for it. The time to build that proof is before a loss, not after.

| Factor | Reasons to Build a Home Inventory | Reasons You Might Put It Off |

|---|---|---|

| Claim speed | Adjusters can verify items immediately rather than requesting follow-up documentation | Most people assume their memory will be good enough in a crisis |

| Payout accuracy | Prevents undervaluation; you can prove replacement cost with receipts and serial numbers | Takes 2–4 hours for an average home if done item by item |

| Coverage review | Reveals gaps between what you own and your current personal property limit | Apps and cloud storage add a minor learning curve |

| High-value items | Scheduled items like jewelry, art, and electronics require documented proof for separate riders | Renters with sparse belongings may find the effort disproportionate |

| Tax documentation | Supports casualty loss deductions if a federally declared disaster occurs | IRS casualty deduction rules limit who actually qualifies |

| Dispute prevention | Reduces back-and-forth with the insurer on quantities, brand, and model specifics | Insurers rarely deny a claim solely due to a missing inventory for simple losses |

Key Takeaways

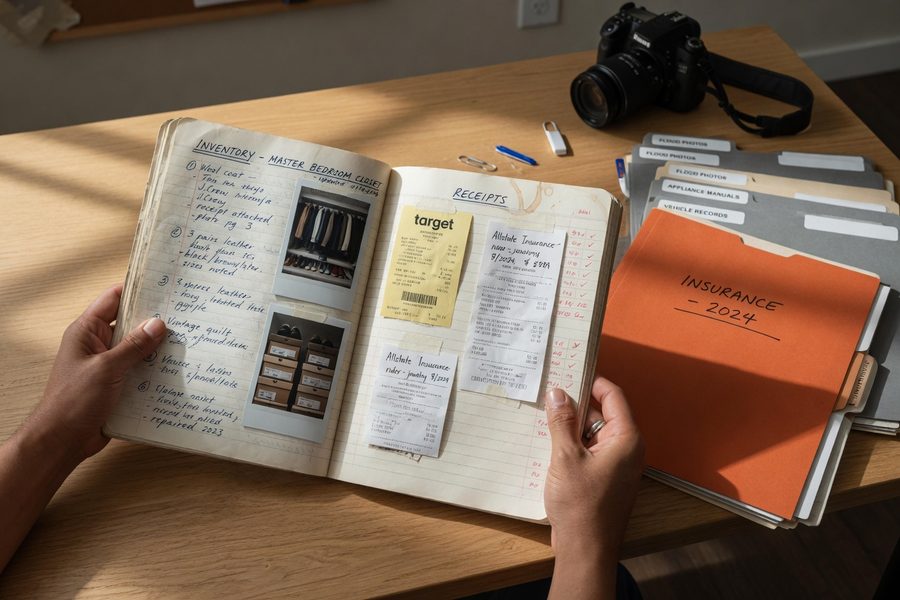

- Your inventory should cover every room, with item descriptions, purchase dates, serial numbers, and estimated current replacement values, not just purchase prices.

- A video walkthrough of a multi-story home plus garage takes roughly 30 minutes and captures visual proof of ownership and condition in one pass.

- Store at least one copy offsite or in cloud storage so a fire or flood that destroys your home does not also destroy your inventory.

- Update your inventory within 30 days of any purchase over $200, after a renovation, or following a major life event like inheritance or marriage.

- High-value items worth more than $1,500 individually, jewelry, instruments, art, collectibles, should have appraisals attached, not just receipts.

- If you lack a full inventory at claim time, pull from email receipts, retailer order histories (Amazon, Best Buy), credit card statements, and social media photos showing your belongings.

- The basics of homeowners insurance coverage define what personal property protection actually pays, knowing your limits before a loss is the only way to know if you are underinsured.

Why a Detailed Home Inventory Speeds Up Insurance Claims

The bottleneck in most personal property claims is not the adjuster’s schedule. It is missing documentation. When you submit a complete itemized list with photos, serial numbers, and receipts, the adjuster can begin valuations the same day rather than sending repeated requests for more information.

The North Carolina Department of Insurance states directly that the information you place in your home inventory file can make insurance claim settlements faster and easier, and that having a record of your property helps you make an accurate claim. That is not marketing language; it reflects how adjusters actually work. Without an inventory, they must rely on your memory of what you owned, cross-reference whatever proof you can gather after the fact, and often negotiate disputed values.

A thorough inventory also reveals whether your personal property coverage limit is actually high enough. Many homeowners discover mid-claim that their limit is $50,000 or $75,000 but their documented belongings total significantly more. In federally declared disaster areas, the IRS requires proof of items lost and their fair market value before allowing casualty loss deductions. Catching that coverage gap before a loss, when you can still adjust your policy, is one of the strongest practical arguments for doing this work now.

One honest caveat worth stating: an inventory does not guarantee a fast claim. If your insurer disputes the replacement cost value itself, or if your policy contains sublimits on specific categories, documentation speeds the process but does not resolve every disagreement. State insurance regulators, including the California Department of Insurance and the Oregon Division of Financial Regulation, both note that policyholders may still need to file complaints or request appraisals even after submitting complete records.

What Actually Makes a Home Inventory Effective

An effective inventory is not a rough list of categories. Insurers expect specific data points, and the more of them you supply, the less room there is for a dispute over what something is worth.

The Iowa Insurance Division describes a home inventory as a detailed list of personal belongings with descriptions, receipts, photographs, and estimated values, calling it an invaluable tool that simplifies the claims process and ensures fair compensation. That four-part combination is what separates an inventory that pays out quickly from one that triggers follow-up requests.

For each item, capture a plain-language description (brand, model, color), the purchase date and price, the serial or model number where applicable, and one or two photos showing its condition. Group entries by room or category, living room, kitchen, bedroom, garage, because that mirrors how adjusters walk through a loss.

Standard household goods and high-value or scheduled items need to be tracked differently. A $300 blender gets a receipt and a photo. A $4,000 engagement ring or a signed piece of art needs a professional appraisal attached to the file, because most standard homeowners policies cap jewelry coverage at $1,500 or less without a separate rider. If you are not sure what your current policy covers, reviewing the key homeowners insurance policy types can clarify where standard coverage ends and scheduled coverage begins.

Video, Apps, or Spreadsheets: Choosing Your Method

Start with a video walkthrough. It is the fastest way to capture proof of ownership and condition across an entire home. A complete walk-through of a multi-story home plus garage takes roughly 30 minutes. Narrate as you go: open drawers, show serial number stickers on electronics, pan across closets slowly. This creates a timestamped visual record that is hard to dispute.

For itemized data, apps close the gap that video leaves open. The NAIC (National Association of Insurance Commissioners) offers an official Home Inventory App with barcode scanning, room grouping, and direct export features along with built-in claim filing tips. It is free and works on both iOS and Android. For households that want AI assistance, Bevel was built specifically in the wake of the 2025 Los Angeles wildfires to help survivors generate itemized insurance lists from existing photos and video footage. InventAI offers voice-entry documentation, letting you speak item details aloud while walking through a room rather than typing each entry.

Spreadsheets still outperform apps in one specific situation: large collections. If you own dozens of books, tools, or kitchen appliances that need to be listed individually, a spreadsheet gives you bulk editing and filtering that most apps cannot match. United Policyholders, a nonprofit consumer advocacy group, publishes a free spreadsheet template compiled from actual lists submitted by disaster survivors who achieved full claim payouts. That real-world provenance makes it more practically aligned with what insurers want than a generic template.

A hybrid approach works well for most households: a video walkthrough for quick visual proof, combined with an app or spreadsheet for the line-item detail that adjusters need for valuations. Export the final inventory as a PDF or Excel file, formats that most insurer portals and adjusters can accept without conversion. Some newer apps also export to JSON, which integrates with claims management systems directly.

The California Department of Insurance recommends keeping a copy of your home inventory and supporting documentation in a safe place outside the home, and updating it at least once per year.

Who Should and Who Should Not

Good candidates

A home inventory pays off most when the financial stakes are high and documentation is the difference between a full payout and a partial one.

- Homeowners in fire-prone, flood-prone, or hurricane-risk areas, where total loss claims are common and documentation disputes are most consequential

- Anyone whose personal property total exceeds their policy’s standard limit, including collectors, musicians, or people with significant electronics or art

- Renters carrying personal property coverage of $30,000 or more, the same documentation rules apply as for homeowners

- Households that have recently renovated, inherited property, or made major purchases and have not updated their coverage since

- Anyone considering whether to reduce their homeowners insurance costs by adjusting personal property limits, the inventory shows exactly what you would be cutting

Who should skip it

The effort is genuinely disproportionate for a narrow group of renters and property owners with low exposure.

- Renters with minimal furnishings and a personal property limit under $15,000, where a quick photo set is sufficient

- Second homeowners who keep the property mostly empty and carry only a bare-bones dwelling policy without personal property coverage

- People who have already suffered a recent loss, filed a claim, and received a full settlement, their adjuster file already contains a documented list that serves as a baseline

Frequently Asked Questions

How long does it take to build a home inventory?

A video walkthrough of an average home takes about 30 minutes. Adding itemized entries with serial numbers and photos for every room typically runs 3 to 5 hours total, though breaking it into one room per day makes it manageable without a large time block.

What if I already had a loss and do not have an inventory?

Start reconstructing from every digital trail available: Amazon and other retailer order histories, credit card statements, email receipts, and social media or cloud photos showing your home and belongings. The Oregon Division of Financial Regulation notes that after a major loss your insurer will ask for a detailed list of personal property, so anything you can compile after the fact is still worth submitting. Insurers can also accept sworn statements for items under certain value thresholds.

Where should I store my home inventory?

Store at least two copies: one in a cloud service (Google Drive, iCloud, or Dropbox) and one on an external drive kept offsite, such as a safe deposit box or a trusted family member’s home. A copy stored only on your home computer is useless if a fire destroys the house and the computer with it.

Does a home inventory affect my insurance premium?

No, having or not having an inventory does not change your premium. Its value is entirely on the claims side, it affects whether you get paid quickly and fully, not what you pay monthly.

How often should I update my home inventory?

Update within 30 days of any significant purchase, after a renovation that adds built-in items to your property, after receiving inherited goods, or following a major life event like marriage. A full annual review, as recommended by the California Department of Insurance, catches cumulative additions you may have overlooked throughout the year.

Is a video walkthrough good enough on its own?

For proving ownership and general condition, yes, a timestamped video is strong evidence. For high-value claims, it is not enough on its own. Adjusters need serial numbers, model details, and purchase prices to calculate replacement cost accurately, and video rarely captures those clearly enough to stand alone.

Sources

- Texas Department of Insurance, Home Inventory Tips

- North Carolina Department of Insurance, Home Inventory Calculator

- California Department of Insurance, Home Inventory Guide

- Oregon Division of Financial Regulation, Home Inventory

- Iowa Insurance Division, Importance of Home Inventory for Disaster or Insurance Claim