Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

Health insurance mental health coverage is federally required for most plans in 2026. ACA Marketplace plans must cover mental health and substance use disorder services as one of 10 essential health benefits, and the Mental Health Parity and Addiction Equity Act (MHPAEA) prohibits plans from imposing stricter limits on mental health care than on physical health care. Short-term and grandfathered plans are exempt.

What does your health plan actually pay for when you need a therapist, a psychiatric hospitalization, or addiction treatment? It’s a fair question, and the gap between what the law promises and what insurers deliver is real. Health insurance mental health coverage is mandated for most Americans under the Affordable Care Act’s essential health benefits framework, which requires all Marketplace plans to include behavioral health treatment, inpatient psychiatric care, and substance use disorder services. That mandate has not changed in 2026.

What has changed is the enforcement environment around parity rules, the funding trajectory of Medicaid, and the practical barriers millions of people still face when trying to use the benefits they’re paying for. This guide breaks down exactly which services are covered, how coverage differs by plan type, what parity actually looks like in practice, and what to do when a claim gets denied.

Key Takeaways

- All ACA Marketplace plans must cover mental health and substance use disorder services as one of 10 essential health benefits, with no annual or lifetime dollar caps (HealthCare.gov).

- An estimated 4.4 million ACA Marketplace enrollees had at least one mental health diagnosis on a health care claim in 2025, representing roughly 18.2% of all enrollees (KFF, 2025).

- The MHPAEA parity law remains enforceable in 2026, but the administration announced in May 2025 it would not enforce the strengthened 2024 final rules, leaving comparative analyses of non-quantitative treatment limitations largely unchecked (CMS).

- Only 70% of employers offering health benefits believe their largest-enrollment plan provides enough providers for timely mental health access, meaning roughly 3 in 10 acknowledge a network gap (KFF 2025 Employer Health Benefits Survey).

- Medicaid finances roughly one-quarter of all U.S. mental health and substance use disorder spending; federal Medicaid funding cuts enacted in 2025 could reduce behavioral health access for tens of millions of beneficiaries (Medicaid.gov).

In This Guide

What Federal Law Requires in 2026

Two federal laws define the floor for mental health coverage: the Affordable Care Act and the Mental Health Parity and Addiction Equity Act. Together, they determine what plans must cover and how restrictive the rules around that coverage can be.

The ACA’s Essential Health Benefits Mandate

Under the ACA, all individual and small-group health plans sold on or off the Marketplace must cover 10 essential health benefits, and mental health and substance use disorder services are one of them. According to HealthCare.gov, covered services include behavioral health treatment such as psychotherapy and counseling, mental and behavioral health inpatient services, and substance use disorder treatment. No plan subject to this requirement can impose annual or lifetime dollar caps on these benefits.

Large-group employer plans are not required to offer mental health benefits under the ACA, but if they do offer them, MHPAEA parity rules apply. That’s a critical distinction affecting roughly 150 million Americans with employer-sponsored coverage.

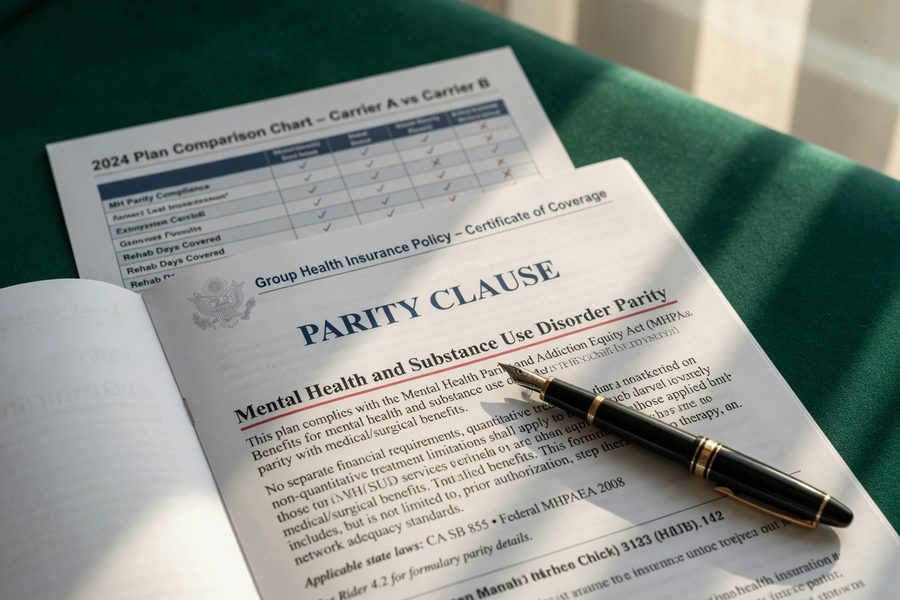

MHPAEA Parity Rules: What Still Applies

The Mental Health Parity and Addiction Equity Act, as explained by the U.S. Department of Labor, prohibits group health plans from imposing financial requirements or treatment limitations on mental health or substance use disorder benefits that are more restrictive than those applied to medical and surgical benefits. This covers copays, deductibles, prior authorization requirements, and medical necessity criteria.

The 2024 final MHPAEA rules, strengthened by the Centers for Medicare & Medicaid Services (CMS), required plans to conduct comparative analyses of non-quantitative treatment limitations (NQTLs) and demonstrate that restrictions on mental health care are not materially more burdensome than on physical health care. In May 2025, the current administration announced it would not enforce those 2024 enhancements. The original MHPAEA framework, however, remains fully in effect and legally enforceable. Plans cannot simply ignore parity; they can no longer be required to produce the specific documentation the 2024 rules mandated.

One honest caveat: short-term health plans, grandfathered plans, and certain church or government plans are exempt from both the ACA essential benefit requirements and MHPAEA. If your plan falls into one of these categories, behavioral health coverage may be minimal or absent entirely.

Short-term health plans, which can now extend up to 364 days in many states, are not required to cover mental health services at all. If you enrolled in one for cost savings, check your Summary of Benefits and Coverage before assuming behavioral health care is included.

Which Services Most Plans Must Cover

For plans subject to the ACA’s essential health benefits rules, the list of covered mental health services is broader than most people realize. The challenge is usually access and cost, not the legal mandate itself.

Outpatient and Preventive Mental Health Services

Outpatient services form the backbone of what most people actually use: individual therapy, group therapy, psychiatric evaluations, and medication management visits with a psychiatrist or prescribing provider. These must be covered, and under MHPAEA, the copays and deductibles applied to these visits cannot be more restrictive than what the plan charges for a comparable medical specialist visit.

Preventive screenings go further. Under the ACA’s preventive care mandate, adult depression screenings and adolescent behavioral health assessments performed by an in-network provider must be covered at $0 cost-sharing, whether or not the patient has met their deductible. Note that the Supreme Court’s 2024 ruling in Braidwood v. Becerra created some uncertainty around preventive care mandates tied to U.S. Preventive Services Task Force (USPSTF) recommendations issued after 2010, but depression screenings recommended before that date remain on firmer legal ground.

Inpatient, Intensive, and Substance Use Services

Plans must also cover inpatient psychiatric hospitalization, partial hospitalization programs (PHP), and intensive outpatient programs (IOP). Substance use disorder treatment, including medically supervised detox, residential rehab, and outpatient counseling, falls under the same coverage requirement.

Residential treatment is where things get complicated. Plans frequently apply medical necessity criteria to determine whether residential care is covered rather than a lower level of care. These criteria vary by plan and are one of the primary mechanisms through which coverage is restricted in practice. More on this in the parity section below. Emergency behavioral health services, including psychiatric crisis care, must also be covered, generally at in-network cost-sharing levels even when provided out-of-network.

Before scheduling an intensive outpatient or residential program, call your insurer and ask for written confirmation of coverage and the specific medical necessity criteria they use. A verbal “yes” from a customer service rep is not a guarantee of payment. A written pre-authorization is.

How Coverage Differs by Insurance Type

Your plan type matters as much as federal law when it comes to what mental health care you can actually access and afford.

Marketplace Plans, Employer Plans, and Telehealth

ACA Marketplace plans offer the most consistent mental health benefit floors. All Marketplace enrollees are guaranteed coverage for mental health and substance use disorder services with no dollar caps. The network, however, is where variation creeps in. A Silver plan from one carrier in your state may have three times as many in-network therapists as a Gold plan from another.

Employer-sponsored plans, which cover the majority of privately insured Americans, must comply with MHPAEA if they offer any mental health benefits. Most large employers do offer these benefits, but plan design varies widely. Some employer plans use carve-out behavioral health networks managed by a separate vendor, meaning your in-network therapist may not be in the same network as your primary care doctor. This is worth checking before assuming your existing providers are covered. For a deeper look at how plan structure affects care access, comparing HMO and PPO plan types can help clarify which model gives you more flexibility for specialist access.

Telehealth mental health services expanded significantly during the COVID-19 public health emergency and have largely remained available through 2026. Most Marketplace and employer plans cover video-based therapy and psychiatry at the same cost-sharing as in-person visits, though some plans have started narrowing telehealth parity in states that do not mandate it. Platforms such as Teladoc Health and Optum’s behavioral health division have become common telehealth vendors for employer-sponsored plans, which means the quality and provider network depth of virtual care can vary depending on which vendor your employer contracts with.

Medicaid, Medicare, and State Variations

Medicaid is the single largest payer of mental health and substance use disorder services in the United States, covering roughly one-quarter of all such spending. Under CMS parity requirements for Medicaid and CHIP, coverage restrictions cannot be more limiting than for comparable medical conditions. This applies to copays, coinsurance, out-of-pocket maximums, and medical necessity criteria alike.

The federal Medicaid funding reductions enacted in 2025, projected to cut roughly 15% of federal Medicaid funding over 10 years, threaten to reduce provider reimbursement rates and enrollment capacity, particularly in expansion states with the most active behavioral health programs. The practical effect on access will vary significantly by state, as some states are absorbing cuts differently from others. Medicare covers outpatient mental health at 80% after the Part B deductible, and inpatient psychiatric care under Part A, though specialized psychiatric facilities carry a 190-day lifetime limit for inpatient stays.

An estimated 4.4 million ACA Marketplace enrollees had at least one mental health diagnosis recorded on a health care claim in 2025, roughly 18.2% of total enrollment. Any significant disruption to Marketplace access would affect this group disproportionately. (KFF, 2025)

The Reality of Parity: Equal on Paper, Unequal in Practice

Federal parity law is enforceable, but enforcement gaps and structural incentives mean mental health care is still harder to access than physical health care for many patients.

One persistent gap is provider reimbursement. Behavioral health providers have historically been reimbursed at lower rates than medical and surgical providers. An RTI International study found rates approximately 22% lower for behavioral health visits compared to equivalent medical visits. Lower reimbursement means fewer providers are willing to accept insurance at all, which shrinks in-network availability and pushes patients toward out-of-pocket costs. The KFF 2025 Employer Health Benefits Survey found that only 70% of employers believe their largest plan provides a sufficient number of providers for timely mental health access, roughly 3 in 10 effectively acknowledge a network adequacy problem.

Prior authorization is another pressure point. Plans may require pre-approval for inpatient psychiatric care, residential treatment, and some outpatient services. Under the original MHPAEA, these requirements must not be more restrictive than what applies to comparable medical services, but comparative analysis of those requirements is precisely what the non-enforced 2024 rules would have mandated. The result is that plan-level restrictions remain inconsistent and are harder to challenge in 2026 than they were projected to be.

The American Medical Association (AMA) has documented these parity gaps using insurer-reported data, finding systematic disparities in prior authorization rates and denial rates between behavioral health and medical claims. The AMA’s analysis, along with DOL enforcement data, makes clear that the problem is structural, not incidental.

Out-of-Pocket Costs, Deductibles, and Hidden Limits

Knowing what your plan covers is step one. Knowing what you’ll actually pay is equally important.

Typical Cost-Sharing for Mental Health Visits

For in-network outpatient therapy, most plans charge either a flat copay (typically $20–$60 per visit for ACA plans after the deductible is met) or coinsurance of 20–40%. High-deductible health plans (HDHPs) require you to meet the full deductible first, which averaged $1,735 for single coverage in employer plans in 2024, before cost-sharing kicks in. That means the first several therapy sessions of the year may be billed at the full contracted rate, often $100–$200 per visit.

Here’s a worked example: if you have a $1,500 deductible and see an in-network therapist at a contracted rate of $150 per session, you’ll pay the full $150 for your first 10 sessions before insurance contributes anything. After that, a 20% coinsurance rate means you pay $30 per session until you hit your out-of-pocket maximum. Understanding how your deductible interacts with mental health visits is explained in more depth in our guide on deductibles versus out-of-pocket maximums.

Residential and Intensive Outpatient Program Costs

Residential psychiatric treatment and intensive outpatient programs carry the highest cost exposure. Even when a plan covers these services, medical necessity denials are common, and the appeals process takes time most people in crisis don’t have. Annual or lifetime dollar caps on mental health benefits are prohibited under the ACA for compliant plans, but visit limits, for example, a maximum of 30 inpatient days per year, may still appear in some grandfathered or exempt plans. If you’re self-employed and shopping for coverage, the cost structure and mental health benefit design of your plan matters significantly. See our overview of health insurance options for self-employed workers in 2026 for plan-type comparisons that factor in behavioral health access.

| Service Type | Typical In-Network Cost | Key Restriction to Watch |

|---|---|---|

| Outpatient Therapy (per visit) | $20–$60 copay or 20–40% coinsurance after deductible | Must meet deductible first on HDHPs |

| Psychiatric Evaluation | $50–$150 copay or 20–40% coinsurance | Prior authorization sometimes required |

| Inpatient Psychiatric (per day) | $250–$500/day or 20–40% coinsurance; subject to deductible | Prior authorization and day limits common |

| Intensive Outpatient Program (IOP) | $50–$150/day or 20–40% coinsurance | Medical necessity review typically required |

| Residential Treatment | 20–40% coinsurance after deductible; can reach out-of-pocket max | Medical necessity denial rate is high; appeal promptly |

| Depression Screening (preventive) | $0 when in-network | Must be billed as preventive, not diagnostic |

How to Check Your Benefits and Appeal a Denial

Start with your plan’s Summary of Benefits and Coverage (SBC) document, which all plans are required to provide. The SBC will list cost-sharing for mental health services in plain language, and it must clearly state whether the plan covers inpatient psychiatric care, substance use disorder treatment, and outpatient behavioral health visits.

Reading Your Plan Documents

Beyond the SBC, request the full Evidence of Coverage or plan booklet to find the specific medical necessity criteria your plan uses for inpatient or residential mental health care. These criteria define when a higher level of care will be approved. If you cannot find them, your insurer is required to provide them upon request under existing MHPAEA regulations. The CMS MHPAEA guidance page outlines what information plans must disclose.

If your claim is denied, you have the right to appeal, first through an internal review by the insurer, then through an external independent review. For mental health claims, explicitly cite MHPAEA in your appeal letter if the denial appears to apply a stricter standard than the plan would apply to an equivalent medical condition. Your state insurance department can provide external review resources, and many states have consumer assistance programs that help with the appeals process at no cost. The DOL’s MHPAEA resources page links to state insurance department contacts.

“As a psychologist, I’ve seen how easily wellbeing falls to the bottom of our ‘to-do’ lists, but I’ve also seen how systemic barriers can make care feel out of reach. We must build a system that truly prioritizes mental health as essential healthcare, not simply an optional benefit.”

For people who’ve had claims denied multiple times or who suspect systematic parity violations, the broader trend of shrinking medical coverage has made appeals more important than ever. Keep records of every call, denial letter, and correspondence, you’ll need them if you escalate to state or federal regulators. Working with a licensed insurance broker who specializes in health coverage can save significant time. Our guide on choosing an insurance broker covers what to look for.

Under federal law, if your insurer denies a mental health claim, you can request the specific reason and the clinical criteria used to make that decision. If those criteria are stricter than what the plan applies to comparable medical or surgical care, that is a parity violation, and grounds for a formal appeal or state complaint.

Frequently Asked Questions

Does my health insurance have to cover therapy?

If you have an ACA Marketplace plan or a small-group employer plan, yes, outpatient therapy is a required essential health benefit. Large-group employer plans are not required to offer mental health benefits, but if they do, those benefits must comply with MHPAEA parity rules. Short-term and grandfathered plans may not cover therapy at all.

Can my insurer limit how many therapy sessions I can use?

Session limits are allowed, but only if the plan applies equivalent limits to comparable medical or surgical services. A plan cannot cap therapy visits at 20 per year if it does not impose a similar cap on visits to a cardiologist or orthopedic specialist, that would be a parity violation under MHPAEA. If you hit a session limit, file an internal appeal and cite parity law explicitly.

Is substance use disorder treatment covered the same as mental health care?

Yes, under both the ACA and MHPAEA, substance use disorder (SUD) treatment is treated in the same category as mental health benefits. Coverage must include medically supervised detox, inpatient and outpatient rehab, and counseling. The same parity rules apply: your plan cannot impose more restrictive prior authorization or visit limits on SUD treatment than on other medical care.

What happens if my in-network therapist stops accepting my insurance?

Network instability is a real problem, driven largely by low reimbursement rates for behavioral health providers. If your therapist leaves your network mid-treatment, most plans offer a continuity-of-care provision allowing you to continue seeing that provider at in-network rates for a transition period, typically 30 to 90 days. Ask your insurer immediately when you learn of the change. This window is time-limited and rarely automatic.

Does Medicaid cover mental health treatment?

Medicaid covers a broad range of mental health and substance use disorder services, and federal parity rules apply to Medicaid managed care plans and CHIP programs. Coverage specifics, including which providers are in network, what prior authorization is required, and which programs are available, vary by state. With federal Medicaid funding reductions enacted in 2025 still working through state budgets, access may be narrowing in some states even while remaining stable in others.

Sources

- HealthCare.gov, Mental Health and Substance Abuse Coverage

- Centers for Medicare & Medicaid Services, Mental Health Parity and Addiction Equity

- U.S. Department of Labor, Mental Health and Substance Use Disorder Parity

- Medicaid.gov, Behavioral Health Services Parity

- KFF, How Might Changes to the ACA Marketplace Impact Enrollees with Mental Health Conditions (2025)

- KFF, 2025 Employer Health Benefits Survey

- American Medical Association, New Insurer Data Shows Parity Gaps: Mental vs. Physical Health Care

- SAMHSA, National Helpline and Treatment Locator