Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

Guaranteed issue term life insurance is extremely rare, most carriers offer only guaranteed issue whole life, not term. Where GI term exists (typically through group or association plans), coverage is usually capped at $25,000 or less, premiums run significantly higher than underwritten alternatives, and a 2-3 year graded benefit period limits early payouts.

Who actually benefits from guaranteed issue term life, and who ends up overpaying for coverage they barely need? That question matters more than most people realize, because the products marketed under this label are frequently misunderstood, and sometimes mislabeled. A surprising number of policies advertised as “guaranteed issue term life” are either graded whole life products or simplified issue policies in thin disguise. Knowing the difference can save a buyer hundreds of dollars a year.

The demand for no-questions-asked coverage is real and growing. According to LIMRA’s 2025 Life Insurers Council survey, final expense life insurance new annualized premium hit $1.05 billion in 2024, up 16% year over year, with roughly 1.06 million policies sold. Yet guaranteed-issue products made up only 15% of those policies, meaning the vast majority of buyers still qualified for simplified-issue coverage with at least some health screening. That context is important: GI coverage serves a specific, narrower market than the advertising implies.

This guide explains exactly what guaranteed issue term life is (and what it is not), who it genuinely protects, the real costs and limitations you need to see before signing anything, and the alternatives worth checking first. The goal is a clear decision framework, not a product pitch.

Key Takeaways

- True guaranteed issue term life insurance is rarely offered by major carriers, most GI products are whole life or graded-benefit final expense policies, not term (South Carolina Department of Insurance, 2025).

- Final expense GI policies averaged a face amount of $9,786 in the 2024 LIMRA-LIC survey (LIMRA, 2025), well below the $25,000 cap common across the category.

- Guaranteed-issue policies made up only 15% of final expense sales in 2024; the other 85% were simplified-issue products requiring at least basic health questions (LIMRA, 2025).

- A 2-3 year graded benefit waiting period applies to most GI policies, beneficiaries typically receive only premiums paid plus interest if the insured dies from illness in that window (North Carolina Department of Insurance, 2025).

- Only 51% of Americans reported having any life insurance in 2024, and 42% said they needed more coverage, showing the coverage gap that GI products attempt to fill (LIMRA Insurance Barometer Study, 2025).

- When GI term coverage does exist through group or association plans, it typically cannot be ported if membership ends, making it an unreliable long-term solution for most buyers.

In This Guide

- What Guaranteed Issue Term Life Insurance Actually Is

- Who Benefits Most from These Policies

- The Real Cost: Premiums Versus Coverage Value

- Limitations and Graded Benefits That Can Hurt Buyers

- Is It Really GI Term? The Mislabeling Problem

- Common Scenarios Where It Helps or Backfires

- Group and Association GI Term Plans

- Better Alternatives When GI Term Falls Short

- How to Compare GI Policies Before You Buy

- A Clear-Eyed Assessment

What Guaranteed Issue Term Life Insurance Actually Is

A guaranteed issue term life policy accepts any eligible applicant, no medical exam, no health questions, for a defined coverage term. The critical word is “term,” and that is precisely where most people run into a wall: no major U.S. life insurer currently offers a standard individual guaranteed issue term product the way they sell 10-, 20-, or 30-year fully underwritten term policies.

The National Association of Insurance Commissioners (NAIC) defines a guaranteed issue life insurance policy as one “where the applicant must be accepted for coverage if the applicant is eligible, with eligibility requirements that may include being within a specified age range.” That definition technically covers both whole life and term structures, but in practice, carriers find GI term actuarially difficult to price profitably. When someone with a terminal diagnosis can lock in a 20-year term with no medical questions, the insurer’s expected loss ratio spikes fast. Whole life products handle this risk better because premiums accumulate cash value and the payout is certain regardless of timing.

How GI Term Differs from GI Whole Life

GI whole life, the dominant form sold in the final expense market, builds a small cash value, has level premiums, and remains in force for life as long as premiums are paid. GI term, where it exists, covers a fixed period and then expires. That sounds appealing because term is generally cheaper. But the GI pricing overlay erases much of the cost advantage that makes term attractive in the first place.

Key features common to both structures include: no medical exam required, age eligibility windows (most commonly 45-85), coverage amounts capped well below what underwritten policies offer, and a graded death benefit during the first two to three years of the policy. If you are shopping because traditional coverage was denied, understanding these features is the starting point, not the sales brochure.

The South Carolina Department of Insurance notes that insurers offering guaranteed issue products “balance the risk by charging higher premiums or by limiting the amount of insurance you can buy”, because they accept applicants without knowing their health history.

Who Benefits Most from These Policies

GI coverage exists for one primary group: people who have been declined for, or cannot qualify for, any other type of life insurance. That is a real population with a real need, and dismissing GI products entirely would be wrong.

The clearest beneficiaries are adults aged 45 to 85 with serious, documented health conditions, advanced heart disease, prior cancer, HIV, recent strokes, or organ transplants, who want to leave money to cover final expenses like funeral costs, small debts, or medical bills. For this group, a policy that pays even $10,000 to a surviving spouse is meaningfully better than no coverage at all. People who have been uninsurable for years and are primarily concerned with the financial burden their death places on family members fit this profile precisely.

The Real Cost: Premiums Versus Coverage Value

The premium-to-benefit ratio on GI policies is the sharpest honest criticism of this product category. Premiums are higher than on any comparable underwritten product, and the face amounts are small.

To put real numbers to it: the average face amount for guaranteed-issue final expense policies sold in 2024 was $9,786, according to LIMRA’s 2025 LIC survey. A 65-year-old male nonsmoker buying a $10,000 GI whole life policy from a carrier like Mutual of Omaha or Gerber Life might pay $80-$100 per month depending on the carrier. That is $960-$1,200 per year for a benefit that covers roughly one modest funeral. A fully underwritten 10-year term policy for the same amount, assuming the buyer is in decent health, would cost a fraction of that. The GI premium load is the actuarial cost of accepting all comers.

Worked Example: Monthly Cost Difference

Consider a practical comparison. The 2024 LIMRA data shows the average GI face amount of $9,786. At a typical GI monthly premium of $90, a buyer pays $1,080 per year. Over 10 years, that is $10,800 in total premiums, which already exceeds the average face amount. A simplified-issue policy with basic health questions for a similar coverage amount might cost $45-$55 per month for a healthy 65-year-old, totaling roughly $540-$660 per year. The GI buyer pays approximately $420-$540 more per year for the privilege of skipping the health questions. That arithmetic is worth running before you decide which product to buy.

Final expense new annualized premium hit $1.05 billion in 2024, up 16% year over year, according to LIMRA’s 2025 Life Insurers Council survey. This is one of the fastest-growing segments in the U.S. life insurance market.

Coverage Cap Problem

Most GI products cap coverage at $25,000, and many sit far below that. The average 2024 GI face amount of $9,786 barely covers a mid-range funeral, which the National Funeral Directors Association estimates at roughly $8,000-$12,000 with burial. Anyone expecting to replace income, pay off a mortgage, or fund a college education with a GI policy is looking at the wrong product entirely. That coverage gap is not a flaw in the product for its intended audience, but it is a serious problem if buyers misjudge what they are getting.

Limitations and Graded Benefits That Can Hurt Buyers

The graded death benefit is the most consequential limitation in guaranteed issue coverage, and it is also the one most frequently glossed over in sales materials. Understanding it is non-negotiable before buying.

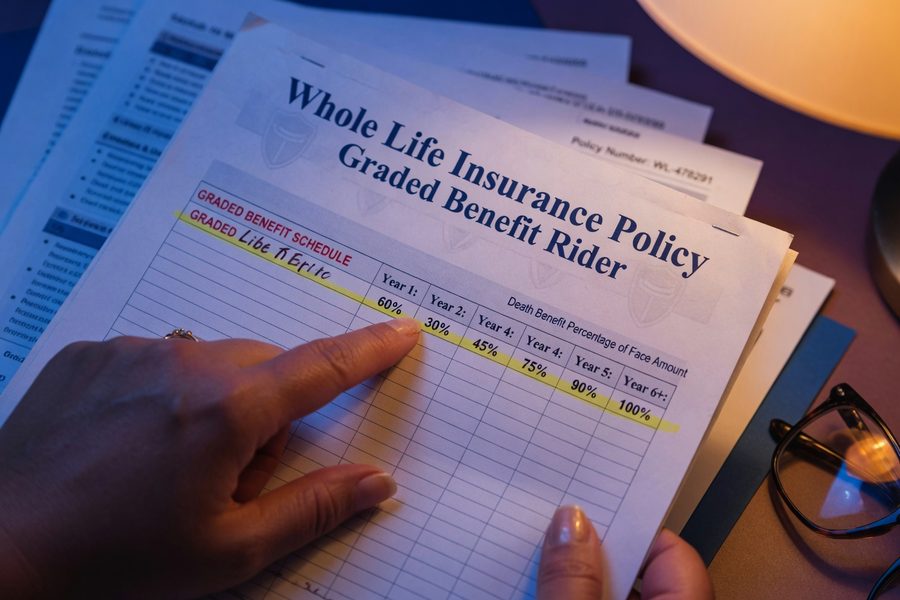

Under a graded death benefit structure, which the North Carolina Department of Insurance confirms must be sold on a guaranteed-issue basis, beneficiaries do not receive the full face amount if the insured dies from illness within the first two to three years of the policy. Instead, they typically receive only the premiums paid, sometimes with 10% interest added. The full face amount pays out only after the waiting period ends, or immediately if death results from an accident.

What Graded Benefits Mean in Practice

Say a policyholder buys a $15,000 GI policy and dies from heart failure 18 months in, having paid $1,440 in premiums. The beneficiary receives $1,440 (plus any stated interest), not $15,000. That is a material difference. Buyers with serious illness who purchase GI coverage hoping to protect a spouse should be clear-eyed: if death comes early, the policy provides minimal financial protection beyond a return of premium.

Term-specific limitations add another layer. If a GI term policy has a 10-year term and the insured survives, they lose coverage at expiration with nothing to show for the premiums paid. Whole life GI policies at least retain cash value. This is one reason actuaries and insurers have historically preferred structuring GI products as whole life rather than term.

A graded benefit means your beneficiary could receive only premiums paid, not the full face amount, if you die from illness within the first 2-3 years of a GI policy. Always read the graded benefit schedule before signing any application.

Is It Really GI Term? The Mislabeling Problem

A significant share of products marketed as “guaranteed issue term life” are not term policies at all. This is one of the most important gaps that most articles on this topic fail to address directly.

Insurers and marketers use the phrase “guaranteed issue” loosely. Many products labeled this way are graded whole life policies with fixed premiums and a death benefit that lasts for life, not a set term. Others are simplified-issue products that ask a short list of health questions (typically 3-10 yes/no questions about major conditions) rather than requiring a full medical exam. Simplified issue is not the same as guaranteed issue: a simplified-issue policy can still decline or rate up an applicant based on answers.

Why the Distinction Matters Financially

A buyer who thinks they are purchasing a temporary term policy for final expense coverage may actually be buying permanent whole life, which has different premium structures, cash value implications, and long-term costs. Conversely, a buyer who thinks they are buying guaranteed acceptance may be surprised when a simplified-issue application is declined due to a recent diagnosis. Reading the policy type on the declarations page, not just the marketing headline, is the only reliable check.

The fundamental differences between life insurance types matter significantly here: term, whole life, and universal life are distinct product structures with different cost profiles, and conflating them leads to poor purchasing decisions.

According to the 2024 LIMRA-LIC survey, 85% of final expense policies sold were simplified-issue, not guaranteed issue. Many buyers who think they purchased a GI policy may have gone through light underwriting without realizing it.

Common Scenarios Where It Helps or Backfires

GI coverage does genuine good in specific situations. It also causes real financial harm when buyers use it as a substitute for underwritten coverage they could have qualified for.

When GI Coverage Actually Helps

A 72-year-old with stage 3 kidney disease who was declined for every other policy they applied for has a narrow set of options. A $10,000-$15,000 GI final expense policy from a carrier like Foresters Financial or New York Life genuinely solves a problem for that person. The premiums are high relative to the benefit, but the alternative is no coverage. For buyers who have exhausted other options and want to spare family members from funeral costs, the product delivers what it promises, as long as the graded benefit period is understood upfront.

When It Backfires

GI coverage backfires most often when buyers who could qualify for simplified-issue or even fully underwritten policies default to GI because the application seems easier. Someone with well-controlled type 2 diabetes, for example, may qualify for a 20-year term policy at a standard or slightly rated premium, which would provide dramatically higher coverage at lower cost than a GI product. Skipping the health questions out of anxiety or convenience, in that case, is an expensive mistake. The best term life insurance companies have expanded their underwriting criteria in recent years, and conditions that once meant automatic decline now often qualify for coverage. Carriers like Legal & General America and Bestow have made particular progress in accepting applicants with managed chronic conditions.

| Buyer Situation | GI Policy Outcome | Better Alternative? |

|---|---|---|

| Terminal illness diagnosis | GI may be only option; graded benefit applies | No practical alternative if recently diagnosed |

| Declined twice for underwritten coverage | GI provides some protection; high premium cost | Try simplified-issue with a different carrier |

| Well-controlled chronic condition | GI overpays by $420-$540+/year | Simplified-issue or rated underwritten term |

| Healthy buyer, age 55-65 | GI is unnecessary and costly | Standard underwritten 10- or 15-year term |

| Needs income replacement ($250k+) | GI coverage cap makes it unsuitable | Underwritten term or group employer coverage |

Group and Association GI Term Plans

The closest thing to true guaranteed issue term life insurance available to most individuals comes through group plans offered by employers, unions, or professional associations. These plans sometimes offer genuine GI enrollment windows, usually when you first join the group, and the coverage is structured as term rather than whole life.

How These Plans Work

A union or professional association might offer members term coverage up to $50,000, term-to-age-70, on a guaranteed-issue basis during open enrollment or within 30 days of joining. Premiums are typically group-rated, making them more competitive than individual GI policies. Employer-sponsored group term life insurance plans governed by ERISA also commonly include a GI component for new hires up to a base coverage threshold, often one or two times annual salary. The tax treatment of these plans falls under Section 79 of the Internal Revenue Code, which allows employers to deduct premium costs and provides favorable tax treatment to employees on the first $50,000 of coverage.

The catch: these plans are not portable in most cases. Leave the job, retire early, or let your association membership lapse, and the coverage ends. Converting to an individual policy at that point usually means either passing simplified-issue underwriting or paying individual GI rates, which are substantially higher. That dependence on continued membership makes group GI term a bridge, not a permanent solution.

State-Level Eligibility Limits

State regulations also shape what GI term looks like in practice. Some states impose maximum age cutoffs for GI term products. New York, for example, has historically capped eligibility at 75 for certain policy types, a restriction enforced through the New York Department of Financial Services. When a term policy has a 10-year term and the buyer is 72, the math creates a problem: the term expires at 82, which is within the eligibility window, but the coverage gap in the buyer’s mid-70s is real if the term lapses and they cannot re-qualify. These age-and-term interactions deserve attention before purchase.

Only 51% of Americans reported having life insurance in 2024, and 42% said they needed more or needed to get coverage, per the LIMRA Insurance Barometer Study. The uninsured gap drives demand for no-questions products even when other options may exist.

Better Alternatives When GI Term Falls Short

For most buyers, at least one alternative to guaranteed issue coverage is worth investigating before settling on a GI product.

Simplified Issue Term and Whole Life

Simplified issue policies ask a short health questionnaire, typically 5-15 questions, but do not require a medical exam or blood draw. Applicants with many chronic conditions still qualify, and premiums are meaningfully lower than GI products because the insurer has at least some health information to price against. Simplified issue term policies from carriers like Bestow, Ladder, or Legal & General America can offer coverage up to $1 million for healthy applicants, with issue ages extending into the mid-60s. Comparison platforms such as Policygenius can surface quotes from multiple simplified-issue carriers simultaneously, which is useful for applicants with borderline health histories.

Employer and Group Coverage

Employer-sponsored group term life insurance under Section 79 of the tax code provides a GI element during initial enrollment and often costs less than individual coverage because of the group risk pool. If your employer offers group term and you have not enrolled, that is almost certainly the cheapest guaranteed coverage available to you. The downside, portability, is the same as with association plans.

Traditional Underwriting for Borderline Cases

Underwriting standards vary significantly by carrier. A condition that disqualifies an applicant at one carrier may be rated (accepted at a higher premium) or even standard-rated at another. Working with an independent broker who places business across multiple carriers is often the most effective strategy for applicants with health issues. The right insurance broker can match your health profile to carriers with more favorable underwriting for specific conditions. Brokers who specialize in high-risk or impaired-risk cases maintain relationships with carriers, including Prudential, Pacific Life, and Principal Financial Group, that have historically shown flexibility on conditions like controlled hypertension or diabetes in remission.

For buyers wondering whether to skip life insurance entirely: if the only dependent is a financially independent adult and there are no co-signed debts or funeral-cost concerns, that is a legitimate decision. Life insurance should solve a specific financial problem, not simply exist because someone sold you a policy.

| Product Type | Health Questions | Typical Coverage Cap | Relative Premium Cost | Portability |

|---|---|---|---|---|

| GI Individual (Whole Life) | None | $25,000 | Highest | Yes, individual policy |

| GI Group/Association Term | None (during window) | $50,000-$100,000 | Moderate | No, ends with membership |

| Simplified Issue Term | 5-15 yes/no | $300,000-$500,000 | Moderate-low | Yes, individual policy |

| Simplified Issue Whole Life | 5-15 yes/no | $50,000-$100,000 | Moderate | Yes, individual policy |

| Fully Underwritten Term | Full exam + history | $5,000,000+ | Lowest | Yes, individual policy |

How to Compare GI Policies Before You Buy

Not all guaranteed issue products are created equal, and the differences between carriers on price and contract terms can be substantial for the same coverage amount.

Factors That Matter Most

Start with the graded benefit schedule. Some carriers offer a two-year waiting period; others extend it to three years. Some return 100% of premiums plus 10% interest if the insured dies during the graded period; others return only premiums paid. That difference in terms can be worth hundreds of dollars to a beneficiary. Read the exact graded benefit language in the policy document, not the marketing summary.

Next, check the age eligibility window and whether the policy renews or converts. A GI term policy that expires at age 80 with no conversion option leaves the buyer uninsured at a high-mortality age. A GI whole life policy that remains in force is a different risk profile entirely. Premium stability matters too, guaranteed level premiums are far preferable to annually renewable policies that escalate with age.

Carriers known for GI final expense products include Mutual of Omaha, Foresters Financial, Gerber Life, and New York Life. Financial strength grades from AM Best and Standard & Poor’s are a useful check on insurer stability before committing to a long-term premium stream. You can also check complaint ratios through the NAIC’s Consumer Insurance Search tool to gauge how carriers handle claims.

Before accepting a GI policy as your only option, ask an independent broker to run your health profile past three or four carriers offering simplified-issue term. Many applicants with chronic conditions qualify for simplified-issue coverage at premiums 30-50% lower than comparable GI products.

A Clear-Eyed Assessment

GI term fills a narrow but legitimate need. For someone who genuinely cannot qualify for anything else, a GI final expense policy, even with its high premiums, low face amounts, and graded benefit period, is better than leaving family members with a funeral bill and no coverage. That is the honest case for the product.

The honest case against it is equally direct. The product is routinely oversold to buyers who could qualify for better coverage if they tried. At an average face amount of $9,786 and premiums that can exceed total benefits over a 10-year period, GI coverage is an expensive last resort that should be treated as such. The marketing is aggressive precisely because commissions are high and the buyer pool is anxious. That combination warrants careful scrutiny.

True GI term products, where coverage expires after a set number of years, are rare, structurally problematic from an actuarial standpoint, and largely absent from major carrier product lines. What you are most likely to find advertised as “guaranteed issue term” is either a GI whole life product, a simplified-issue policy, or a group plan with portability limitations. Knowing the product you are actually buying is the single most important step in this process.

For a broader view of how different insurance types interact with your overall financial protection, the overview of insurance types and their benefits is a useful reference point.

Real-World Example: The Cost of Choosing GI Over Simplified Issue

Consider an illustrative example: a 67-year-old woman with well-managed hypertension and type 2 diabetes purchases a guaranteed issue whole life policy with a $15,000 face amount after seeing a television advertisement. Her monthly premium is $95, or $1,140 per year. She chose the GI policy because she assumed her diabetes would disqualify her elsewhere.

An independent broker later shows her that two simplified-issue carriers would have offered her a $15,000 permanent policy at $55-$60 per month given her controlled condition history, a difference of $35-$40 per month, or $420-$480 per year in savings at the low end and $540-$720 per year at the high end. Over 10 years, her GI choice costs her approximately $4,200-$7,200 more in premiums for identical coverage, depending on which simplified-issue rate she qualified for. The graded benefit period on both products is two years, so there is no meaningful protection difference. The only difference is the application process: the simplified-issue carrier asked eight yes/no health questions; the GI carrier asked none. That convenience carries a steep price.

This scenario is not unusual. The LIMRA data showing 85% of final expense buyers qualified for simplified issue suggests that most people buying GI coverage could have answered a short health questionnaire and saved meaningfully on premiums.

Your Action Plan

-

Check your actual insurability before assuming GI is your only option

Use an independent broker marketplace like Policygenius or contact a direct independent broker to submit your health profile to three or more simplified-issue carriers. Many chronic conditions, controlled diabetes, treated hypertension, past cancer in remission, qualify for simplified-issue products at substantially lower premiums.

-

Verify whether the policy is truly “guaranteed issue” or simplified issue

Ask the carrier directly: “Will any health answer disqualify me?” If the answer is yes, it is simplified issue. Pull the actual policy or specimen contract, not the marketing brochure, and look for the words “guaranteed issue” in the contract language itself. The NAIC’s consumer guide to life insurance explains the terminology and your rights as an applicant.

-

Read the graded death benefit schedule in full before signing

Locate the section of the policy that describes what your beneficiary receives if you die in years one and two (and year three if applicable). Note whether the return is premiums only or premiums plus interest. Note the exact date the graded period ends and the full face amount becomes payable. Write the end date on your policy documents.

-

Compare at least three GI carriers on price and contract terms if GI is genuinely your best option

Request quotes from carriers rated A- or better by AM Best. Compare on: monthly premium, face amount, graded benefit terms, conversion options (if any), and renewal provisions. Check complaint ratios at the NAIC Consumer Insurance Search to identify carriers with a history of claims disputes.

-

Check employer and association group coverage first

If you are employed or belong to a professional association, union, or alumni organization, call your HR department or association benefits coordinator and ask whether a GI enrollment window is open. Group term rates are almost always lower than individual GI rates, and the acceptance is truly guaranteed during open enrollment periods. Note any portability limitations in writing.

-

Revisit your coverage needs in 12-24 months

Health conditions change. If you purchased a GI policy because of a recent diagnosis that has since been treated or stabilized, re-apply for simplified-issue or underwritten coverage annually for two to three years. Remission, successful treatment, or improved health markers can open doors to better-priced coverage that did not exist when you first applied. Set a calendar reminder and check the current top-rated term life carriers for updated underwriting guidelines.

Frequently Asked Questions

Does any major carrier actually offer guaranteed issue term life insurance?

No major U.S. carrier currently offers a standard individual guaranteed issue term life product comparable to a 10-, 20-, or 30-year underwritten term policy. What exists is primarily GI whole life (final expense) for individuals, and GI term through select group or association plans. Products marketed as “GI term” in individual channels are typically either whole life or simplified-issue products.

What is the difference between guaranteed issue and simplified issue life insurance?

Guaranteed issue accepts all eligible applicants with no health questions, period. Simplified issue asks a short list of health questions (typically 5-15 yes/no items) but requires no medical exam; an unfavorable answer can still result in a decline or higher premium. Simplified issue is not guaranteed acceptance, though it is far less rigorous than full underwriting.

How does the graded death benefit work, and when does it not apply?

A graded death benefit means that if the insured dies from illness within the first two to three years of the policy, the beneficiary receives only premiums paid (sometimes plus 10% interest), not the full face amount. The graded period does not apply to accidental death, that typically pays the full face amount from day one. After the graded period ends, all causes of death pay the full benefit.

Can I get a guaranteed issue policy if I am under 45?

Most individual GI products set the minimum eligibility age at 45-50. A small number of carriers offer GI products starting at 40, but these are uncommon. Applicants under 45 with health conditions that make standard underwriting difficult are better served by simplified-issue products, employer group coverage, or working with a broker who specializes in high-risk cases.

Is the premium I pay for a GI policy ever returned if I outlive the term?

No, not in a standard GI policy. As with any term insurance, premiums pay for coverage during the term period; if the insured outlives the term, coverage ends and premiums are not returned. Some products include a “return of premium” rider that refunds paid premiums at term expiration, but this increases monthly costs significantly and is uncommon in the GI space.

Are premiums for guaranteed issue life insurance tax-deductible?

Generally, no. Premiums paid on personal life insurance policies, including GI products, are not deductible as a personal expense under IRS rules. The death benefit, however, is generally received by beneficiaries income-tax-free under IRC Section 101(a). Consult a tax professional for situations involving business-owned policies or key-person coverage.

What happens to my GI group term coverage if I leave my employer or association?

In most cases, group term coverage ends when membership ends. Some group plans offer a conversion right, allowing you to convert group coverage to an individual policy without new underwriting, but converted individual policies are typically priced at standard individual GI rates, which are higher. Check your group plan’s conversion provision and any portability options before assuming coverage will continue.

Our Methodology

This article was researched using primary data from LIMRA’s 2025 Life Insurers Council Final Expense Survey, state insurance department regulatory guidance from South Carolina and North Carolina, and the NAIC’s official Valuation Manual definitions. Product category analysis draws on publicly available carrier product guides and independent broker market observations. Statistics are cited with direct hyperlinks to their source documents. No carrier paid for inclusion or favorable treatment in this article. Premium estimate ranges reflect publicly available rate illustrations from multiple carriers as of mid-2025 and are provided for illustrative comparison only; actual premiums depend on applicant age, state of residence, health status, and carrier. Coverage cap figures reflect the standard market range documented in LIMRA survey data. Carrier financial strength references reflect AM Best ratings publicly available as of the publication date.

Sources

- LIMRA, Life Insurers Council Final Expense Insurance New Annualized Premium Increased 16% in 2024

- MarketWatch, Life Insurance Statistics (LIMRA Insurance Barometer Study, 2025)

- South Carolina Department of Insurance, Guaranteed Issue Life Insurance FAQ

- North Carolina Department of Insurance, Individual Term Life / Graded Death Benefit Requirements

- National Association of Insurance Commissioners (NAIC), Valuation Manual 2020 Edition (GI Definition)

- NAIC, Consumer’s Guide to Life Insurance

- NAIC, Consumer Insurance Search (Complaint Ratios)

- National Funeral Directors Association, Funeral Cost Statistics

- Internal Revenue Service, Publication 525: Taxable and Nontaxable Income (Life Insurance Benefits)

- AM Best, Life Insurance Financial Strength Ratings