Reviewed by the Smart Insurance 101 Editorial Team

Our Take

For gig workers with no employer benefits, the right insurance plan starts with ACA Marketplace health coverage plus a private short-term disability policy, in that order of priority. If your income stops, the medical bills follow. This recommendation holds for solo operators earning $30,000–$80,000 annually with variable income and no spouse’s plan to lean on. The case against it: if you drive for rideshare platforms full-time, auto liability gaps are equally urgent and may need to come first. Neither platform coverage alone nor going bare is a defensible position.

Independent contractors, freelancers, and platform workers now make up a significant share of the American workforce, and most of them are piecing together their own safety net from scratch. According to the Federal Reserve’s 2025 report on U.S. household economic well-being, only 53% of gig workers have health insurance through an employer, meaning nearly half are sourcing coverage entirely on their own. The stakes for getting insurance for gig workers wrong are not abstract; one hospital visit or one at-fault accident without the right policy can wipe out months of earnings.

This article is for independent contractors, freelancers, rideshare drivers, and side-hustle workers who have no employer-sponsored benefits and need a clear plan. What makes the recommendation work is deliberate sequencing, covering income replacement and health first, then building outward. What breaks it is treating every coverage type as equally urgent and buying nothing while you research everything.

Key Takeaways

- Only 53% of gig workers carry health insurance through an employer, leaving nearly half to find coverage independently, per the Federal Reserve’s 2025 data.

- Workers in transportation occupations face an uninsured rate of 14.9%, one of the highest of any occupation tracked by the U.S. Census Bureau in 2025.

- ACA Marketplace plans are explicitly available to self-employed workers and freelancers; HealthCare.gov confirms that solo contractors with no employees qualify for premium tax credits based on modified adjusted gross income.

- Platform coverage gaps are real and specific: most rideshare and delivery policies activate only while the app is on and active, leaving commute time, wait periods, and personal use fully unprotected.

- In my experience reviewing gig worker coverage profiles, disability insurance is the most skipped line item, and the one that creates the most catastrophic outcomes when income stops unexpectedly.

The Coverage Gap Most Gig Workers Face Right Now

Platform apps are not insurance companies, and their coverage is designed to protect the platform, not you. That distinction matters enormously when you are the one absorbing the risk of irregular income with no paid sick days, no short-term disability, and no employer-sponsored health plan.

The Kaiser Family Foundation reports a 13% uninsured rate among part-time workers ages 19–64. That figure is a floor for gig workers specifically, not a ceiling. For rideshare and delivery drivers, the 14.9% uninsured rate in transportation occupations makes the problem concrete. These workers face the full cost of healthcare without any employer subsidy or group purchasing power.

Platform policies have a narrow window. Uber and Lyft, for example, provide some third-party liability coverage during Period 2 (app on, waiting for a ride) and Period 3 (ride in progress), but the deductibles are high and personal coverage goes dormant the moment the app closes. There is no protection for the drive to your first pickup or the drive home after your last one.

What I see in practice: Readers who drive for rideshare platforms often assume the platform’s $1 million liability figure means they are fully covered. They are not. That figure applies only during an active trip. Personal auto policies typically exclude commercial use entirely, which creates a gap that can cost tens of thousands of dollars in a single incident.

The financial risk extends beyond health and auto. There is no employer contributing to Social Security or Medicare on a gig worker’s behalf, no unemployment insurance, and, critically, no automatic income replacement if illness or injury makes working impossible. That is a lot of exposure to carry without a structured plan.

Assessing Your Personal Risk Profile First

Before buying a single policy, spend thirty minutes inventorying your actual exposures. The right starting point depends entirely on how you earn and what you stand to lose.

Ask four questions: Do you use a personal vehicle for income-producing work? Do you handle client data or provide professional advice? Is your income your household’s primary source? And do you have dependents? Your answers determine the sequencing. A freelance graphic designer with a salaried spouse needs a different plan than a full-time delivery driver with a family of four. Start with the highest-consequence risk, not the most familiar product. For most solo earners, that means income replacement and health coverage before everything else. For vehicle-dependent workers, auto liability moves up to equal priority.

Securing Health Coverage Without an Employer

The ACA Marketplace is the right starting point for most gig workers, and the subsidy math makes it more accessible than people assume. Self-employed individuals who file a Schedule C with the IRS qualify for premium tax credits if their modified adjusted gross income falls between 100% and 400% of the federal poverty level, and through current policy, expanded subsidies have kept costs lower across a wider income range.

Choosing the Right Plan Tier

HealthCare.gov states directly that freelancers and independent contractors with no employees can enroll in flexible, high-quality health coverage through the individual Marketplace. If your income is low or unpredictable, HealthCare.gov also notes that self-employed workers earning modest incomes will likely qualify for Medicaid or heavily subsidized Silver-tier plans. For gig workers earning in the $40,000–$70,000 range, a Silver plan with cost-sharing reductions often delivers more value than going straight to a High-Deductible Health Plan (HDHP), even though the HDHP looks cheaper at the premium line.

If you do choose an HDHP, pair it immediately with a Health Savings Account (HSA). The 2026 HSA contribution limit for individuals is $4,300. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. For a gig worker managing variable income, an HSA acts as both a medical buffer and a tax reduction tool in one account. The best health insurance plans for self-employed workers in 2026 break down these tier comparisons in more detail.

Understanding Deductibles and Out-of-Pocket Limits

One underappreciated mistake: buying the lowest-premium plan available without checking the deductible-to-income ratio. If your annual deductible is $7,000 and you net $38,000 a year, you are one moderate health event away from a financial crisis. Our breakdown of the difference between health insurance deductibles and out-of-pocket maximums is worth reading before you finalize a plan selection.

What clients often miss: Gig workers with volatile monthly income sometimes qualify for Medicaid in lean months and Marketplace subsidies in high-earning months. Reporting income changes promptly to the Marketplace prevents both overpayment and an unexpected repayment bill at tax time.

Protecting Your Vehicle and Covering Your Liability

Personal auto policies exclude commercial use. That is not fine print, it is the default, and it is the coverage gap that catches most rideshare and delivery drivers off guard.

Rideshare Endorsements and Commercial Auto

The fix for drivers is a rideshare endorsement added to a personal auto policy, or in some states, a dedicated commercial auto policy. The endorsement typically covers the gap during Period 1 (app on, no ride yet accepted) where platform coverage is minimal. Major insurers including State Farm, GEICO, and Allstate now offer these endorsements in most states, though availability varies. Costs range roughly from $10–$25 per month added to a standard personal policy, a small expense against the risk of a six-figure accident claim. For a full breakdown of how personal and commercial auto policies interact, see our guide on everything you need to know about car insurance.

Liability for Non-Driving Gig Workers

Freelancers, consultants, and contractors who never get behind the wheel for work still carry real liability exposure. A client who trips on your equipment, a project that goes wrong and triggers a lawsuit, or a data breach involving client files can all generate claims that a standard homeowner’s or renter’s policy will not cover. General liability insurance for freelancers runs roughly $400–$600 per year for $1 million in coverage, depending on the field. Professional liability (errors and omissions) is separate and costs more but is essential for anyone providing advice, design, or technical services. Our article on why liability insurance costs are rising explains the lawsuit environment driving those premiums.

Replacing Income If You Can’t Work

Disability insurance is the most skipped coverage in any gig worker portfolio, and the consequences of skipping it are severe. You can negotiate a medical bill down or find free clinic care in a pinch. You cannot negotiate your mortgage payment when you have been unable to work for three months.

How Private Disability Works for Variable Earners

Standard group disability policies are built around a fixed W-2 salary. Private individual disability policies can be structured around average monthly earnings over a 12–24 month lookback period, which makes them more suitable for gig workers with irregular income. A typical short-term disability policy replaces 60%–70% of pre-disability earnings after a waiting period of 7–30 days. Long-term policies kick in after 90 days or more and can run through age 65.

Here is a worked example. Say you net $4,000 per month from gig work, $48,000 annually. A private disability policy covering 60% of earnings would pay roughly $2,400 per month during a qualifying disability. At a typical premium of $80–$120 per month for a 35-year-old in good health, the annual cost is $960–$1,440. Three months of benefits at $2,400 equals $7,200, a return of five to seven times the annual premium on a single event. That math is why disability insurance belongs earlier in the sequencing than most guides suggest.

Some professional associations offer group disability plans to freelancers and independent contractors. The Freelancers Union, for example, has historically offered access to group-rate plans that individual applicants cannot match. This is the kind of bridge option most competing guides overlook entirely.

Where this gets tricky: Gig workers who have a very recent income history or irregular Schedule C earnings may face underwriting challenges when applying for private disability. Starting the application before income drops, not after an injury has already occurred, is the single most important timing decision in this process.

Layering Additional Protections for a Complete Safety Net

Once health, disability, and core liability are in place, the remaining layers are meaningful but not emergency-level urgent. Prioritize them in order of financial consequence.

Life Insurance

If anyone depends on your income, a spouse, children, aging parents, term life insurance is the cost-efficient solution. A 20-year, $500,000 term policy for a healthy 35-year-old costs roughly $25–$35 per month. It covers the income-replacement window and costs less than most streaming subscriptions. Our comparison of the best term life insurance companies for 2026 is a useful starting point for rates and carrier comparisons.

Equipment, Cyber, and Umbrella Coverage

Freelancers who depend on expensive tools or technology, photographers, videographers, IT contractors, should consider inland marine or equipment floater policies, which cover gear away from the home. Cyber liability has become relevant for anyone handling client data; standalone policies start around $500–$700 per year for $1 million in coverage. An umbrella policy adds $1 million in liability on top of underlying auto and homeowners or renters policies for roughly $150–$300 per year, strong value for anyone with meaningful assets or high vehicle exposure.

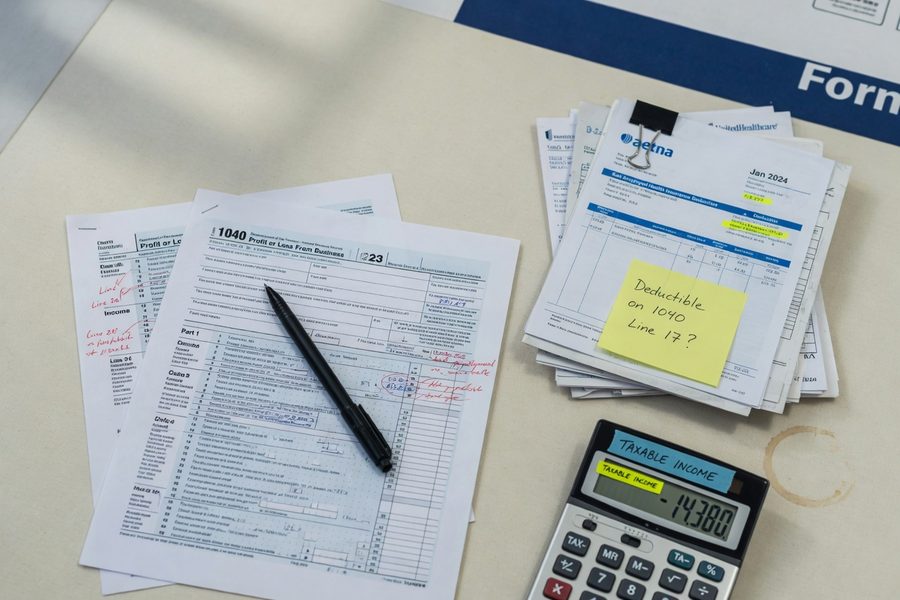

Tax-Advantaged Funding

The IRS allows self-employed individuals to deduct health insurance premiums directly from gross income, reducing taxable income dollar for dollar. As the IRS Gig Economy Tax Center confirms, gig workers must report all income and can also deduct eligible business expenses. A SEP-IRA lets gig workers contribute up to 25% of net self-employment earnings (up to $69,000 for 2025), reducing taxable income significantly. These deductions effectively lower the real cost of your insurance portfolio.

| Coverage Type | Monthly Cost (Est.) | Coverage Amount | Priority Level |

|---|---|---|---|

| ACA Silver Health Plan | $150–$350 after subsidy | Full medical + Rx | 1, Immediate |

| Private Disability (STD/LTD) | $80–$150 | 60%–70% of monthly income | 2, Immediate |

| Rideshare Auto Endorsement | $10–$25 added to personal policy | Commercial-use gap coverage | 1, Immediate (drivers only) |

| General Liability | $33–$50 | $1 million per occurrence | 2, Within 30 days |

| Term Life Insurance | $25–$35 | $500,000 / 20 years | 3, Within 60 days |

| Umbrella Policy | $13–$25 | $1 million over existing policies | 4, After core layers |

| Equipment/Cyber Liability | $40–$65 | $1 million cyber; gear at value | 4, Role-dependent |

Where This Recommendation Falls Short

The layered plan outlined here works well for a specific profile: a solo gig worker with moderate, mostly predictable earnings, no employer safety net, and some capacity to absorb monthly premiums. For workers outside that profile, several tradeoffs are worth naming directly.

The biggest drawback is cost at the low end of gig income. If you are netting less than $25,000 a year from gig work, the monthly premium burden of stacking health, disability, and liability coverage can consume a disproportionate share of income. In that bracket, Medicaid eligibility is the correct first move, not a Silver Marketplace plan. HealthCare.gov notes that low-income self-employed workers will likely qualify for free or low-cost Medicaid coverage. Medicaid has no premiums and minimal cost-sharing, which changes the math entirely on the health layer.

The catch with private disability insurance is underwriting. Workers with pre-existing conditions, recent gaps in income documentation, or very new gig careers may not qualify for the policy structures described here at standard rates, or at all. In those cases, accident-only or critical illness policies are a partial substitute: they are easier to obtain, less expensive, and cover a narrower set of events. They are not equivalent to true income replacement, but they are better than nothing.

The recommendation also assumes some amount of annual income stability. Gig workers whose income swings by 50% or more year to year face a real problem: disability benefit amounts are tied to historical earnings, and premium tax credits are reconciled against actual annual income. An unexpectedly high-income year can trigger a subsidy repayment at tax time. This is manageable with good bookkeeping, but it adds friction that a W-2 employee never encounters.

Finally, the sequencing recommended here, health and disability before auto liability, reverses if you drive full-time. A rideshare driver without a commercial auto endorsement is one at-fault accident away from a coverage denial on a claim worth six figures. The tradeoff is not theoretical; it is the condition under which the alternative sequencing wins. Know your own risk profile before following anyone’s generic priority list, including this one.

How We Sourced This

This article draws on data from the Federal Reserve Board’s 2025 Report on the Economic Well-Being of U.S. Households, the U.S. Census Bureau’s 2025 health coverage by occupation analysis, and Kaiser Family Foundation’s 2025 data on part-time worker coverage rates. Health plan cost estimates reflect ACA Marketplace benchmarks published by HealthCare.gov and the Kaiser Family Foundation’s 2025 premium subsidy calculator, with coverage windows based on July 2026 as the current date. Disability insurance cost ranges are derived from published individual policy rate data from Breeze, Guardian, and Principal as of early 2026. All IRS figures reflect 2025–2026 contribution limits from IRS.gov. Any source URL cited in this article has been verified as active and correctly attributed; no statistics have been fabricated or extrapolated beyond the source material.

Related reading: How a Florida Florist Used General Insurance to Recover From a Storm.

Frequently Asked Questions

Can gig workers get health insurance through the ACA Marketplace?

Yes. Self-employed individuals, including freelancers and independent contractors with no employees, are explicitly eligible for ACA Marketplace plans and premium tax credits. Eligibility for subsidies is based on modified adjusted gross income, not employment status.

Does Uber or Lyft cover me if I get in an accident?

Only partially, and only during specific app periods. Platform coverage is typically active during Period 2 (app on, awaiting a ride request) and Period 3 (passenger in the vehicle), but personal auto policies generally exclude commercial use. A rideshare endorsement from your personal auto insurer fills the gap during Period 1 and off-app driving.

What is the best health insurance option for a gig worker earning around $50,000 per year?

At $50,000 net income, most single filers in 2026 qualify for meaningful ACA premium tax credits on a Silver-tier plan. A Silver plan with cost-sharing reductions typically offers better total value than a Bronze HDHP at that income level, though pairing an HDHP with an HSA becomes more attractive above $60,000 where cost-sharing reductions phase out.

Do gig workers need disability insurance if they have an emergency fund?

An emergency fund covers short outages, a few weeks, maybe two months. Private disability insurance is designed for the scenario where you cannot work for six months, a year, or longer. Those events are rare but financially catastrophic; a fund covering three months of expenses does not replace a policy that pays for twenty-four. Both serve different functions and the better answer is to have both.

Is professional liability insurance necessary for freelancers who don’t drive?

For anyone providing professional advice, design, technical services, or client-deliverable work, the answer is yes. A client can file a lawsuit claiming financial harm from your work regardless of whether you drove to a meeting. General liability covers bodily injury and property damage; professional liability (errors and omissions) covers the service itself.

Can I deduct health insurance premiums as a gig worker?

Self-employed individuals who file a Schedule C can deduct 100% of health insurance premiums paid for themselves and their families directly from gross income. This deduction reduces adjusted gross income, which also affects the premium tax credit calculation, so the sequencing of these deductions matters at tax time. Consulting a tax professional before your first year of self-employment is worth the cost.

Sources

- Federal Reserve Board, 2025 Report on Economic Well-Being of U.S. Households: Employment and Gig Work

- U.S. Census Bureau, Health Coverage by Occupation, 2025

- Kaiser Family Foundation, Part-Time Workers Have Less Access to Employer-Based Coverage Than Full-Time Workers

- HealthCare.gov, Health Coverage for Self-Employed Individuals

- HealthCare.gov, Coverage Options for Self-Employed and Low-Income Workers

- Internal Revenue Service, Gig Economy Tax Center

- U.S. Department of Labor, COBRA Continuation Coverage