Reviewed by the Smart Insurance 101 Editorial Team

Our Take

For most first-time homebuyers, the single costliest mistake is setting dwelling coverage based on purchase price instead of true rebuild cost, and it shows up at the worst possible moment: during a claim. Buy a replacement cost policy, verify the rebuild estimate against your area’s current construction costs, and add flood coverage separately unless your lender and FEMA both confirm you’re in a minimal-risk zone. Two in three U.S. homes are already underinsured. The case for skipping this extra due diligence is only valid if you have the cash reserves to cover a six-figure gap yourself.

Buying a home is the largest financial commitment most people make, and the insurance decision that comes with it is often rushed. The Consumer Financial Protection Bureau notes that lenders require homeowners insurance as a condition of most mortgages, which means new buyers are under pressure to produce a policy quickly, not necessarily a good one. Premiums have climbed sharply too: average U.S. homeowners insurance premiums jumped 11.2% from 2021 to 2022 alone, according to Insurance Information Institute data from the NAIC, and costs have continued rising since.

This article is for buyers who are closing within the next 60 days or who just closed and haven’t reviewed their coverage since. What makes the recommendation work is understanding three specific gaps that standard first policies leave open, and knowing which one to close first.

Key Takeaways

- Two in three U.S. homes are underinsured, with first-time buyers most at risk because they set dwelling limits based on purchase price rather than actual rebuild costs.

- Only 4% of U.S. homeowners carry flood insurance, according to the Joint Economic Committee (2024), yet standard homeowners policies exclude flood damage entirely.

- Average deductibles rose 22% in 2025, meaning buyers who chose high deductibles to lower premiums now face steeper out-of-pocket costs at claim time, a tradeoff first-timers rarely model in advance.

- 5.3% of insured homes filed a claim in 2023, per Insurance Information Institute, which means roughly 1 in 19 homeowners will test their coverage in any given year.

- In my observation, buyers who get competing quotes with identical coverage terms, not just identical prices, consistently find better-matched policies; price-only comparisons almost always hide deductible and limit differences.

Why First-Time Buyers So Often End Up Underprotected

The rush to close is the root cause. Buyers are juggling inspections, appraisals, title work, and lender demands simultaneously, and homeowners insurance gets treated as one more checkbox. Lenders require proof of coverage before funding, which creates real deadline pressure, but that pressure rewards speed, not thoroughness.

Escrow accounts make this worse. When your mortgage servicer pays the annual premium out of escrow, you stop thinking of insurance as a bill you manage. The cost disappears into your monthly payment, and the motivation to shop or review coverage quietly evaporates. That’s a problem, because the Consumer Federation of America found that 7.4% of U.S. homeowners have no homeowners insurance at all, and many more carry policies with limits that haven’t been updated since the policy was first written.

What I see in practice: New homeowners who accepted the first quote their real estate agent recommended often don’t discover their coverage gaps until year two or three, when they try to add a fence or file a water damage claim. The policy they bought worked for the lender, it didn’t necessarily work for them.

Our beginner’s guide to homeowners insurance covers the foundational concepts, but this article focuses specifically on where the first policy tends to go wrong.

Replacement Cost vs. Market Value: The Costliest Misunderstanding in a First Homeowners Insurance Policy

Here’s the thing: your home’s market value and its rebuild cost are two entirely different numbers, and confusing them is expensive. Market value reflects land, location, and comparable sales. Rebuild cost reflects labor, materials, debris removal, and contractor fees, and construction costs have climbed sharply since 2023, widening the gap in many markets.

Why purchase price is the wrong benchmark

Many buyers set their dwelling limit at or near the purchase price because it feels like a logical ceiling. It isn’t. If your home is destroyed, you don’t need to buy the land again, but you do need to pay for skilled trades at current rates. In high-cost metros, that number can exceed the purchase price; in many Midwest markets, it can be lower. Either way, the purchase price is the wrong input.

The Texas Department of Insurance recommends replacement cost policies specifically because most mortgage companies require them, and because actual cash value policies subtract depreciation from payouts, meaning a 15-year-old roof pays out far less than it costs to replace. Request a replacement cost estimate from your insurer, then cross-check it with a free online estimator like CoreLogic or Marshall & Swift. Don’t rely solely on the agent’s figure.

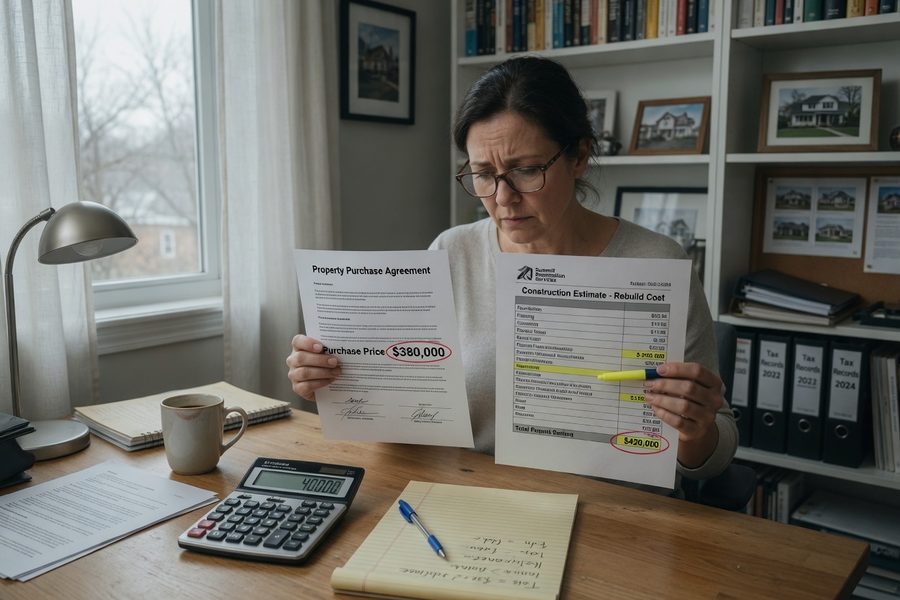

A worked example

Say a home is purchased for $380,000 in a market where rebuild cost is $420,000. The buyer sets dwelling coverage at $380,000. After a total loss, the insurer pays $380,000. The actual rebuild invoice comes to $420,000. That buyer absorbs a $40,000 out-of-pocket gap, roughly 10.5% of the total rebuild cost, not because of a policy dispute, but because the wrong number was used from the start.

What Standard Policies Exclude That New Owners Assume Are Covered

Standard homeowners policies exclude flood damage, earthquake damage, and sewer backup. Full stop. These are not edge cases, they are predictable gaps that catch first-time buyers off guard because no one explains the exclusions during the sales process.

Flood coverage requires a separate policy, typically through the National Flood Insurance Program (NFIP) or a private flood carrier. Yet only 4% of U.S. homeowners carry flood insurance, per the Joint Economic Committee. Many buyers assume flood coverage exists because they live outside a FEMA-designated high-risk zone. That’s a misread: flood damage from heavy rain, drainage failures, or storm surge can occur anywhere, and the standard policy won’t pay for it.

The Washington State Office of the Insurance Commissioner emphasizes understanding what a policy does and does not cover before purchasing, sound advice that most first-time buyers follow only after a claim denial. Sewer backup is another common miss: it’s excluded from most standard forms but available as an inexpensive endorsement, often under $50 per year. Add it.

What clients often miss: Named-peril policies only pay for losses specifically listed in the policy. Open-peril (or “all-risk”) policies cover everything except what’s explicitly excluded. First-time buyers frequently don’t know which type they purchased, and named-peril forms are more common in lower-priced policies.

High-value items, jewelry, collectibles, firearms, art, face sublimits under most standard policies, often capped at $1,500 to $2,500 per category. A scheduled endorsement or floater closes that gap. For more context on coverage types and what each protects, see our overview of important homeowners insurance policies to know.

Shopping the Lowest Quote Is Not the Same as Shopping for Value

Choosing the cheapest premium is the most common shopping error first-time buyers make. Low premiums are almost always explained by higher deductibles, lower limits, or both, and neither shows up obviously in a price comparison.

| Factor | Budget Policy Example | Value Policy Example |

|---|---|---|

| Annual Premium | $1,100 | $1,480 |

| Dwelling Deductible | $5,000 | $2,500 |

| Dwelling Limit | $300,000 | $420,000 |

| Personal Property | ACV (depreciated) | Replacement Cost |

| Liability Limit | $100,000 | $300,000 |

| Sewer Backup | Not included | Included |

The $380 annual premium difference, roughly $32 per month, looks like savings. But if a pipe bursts and causes $8,000 in damage, the budget policy’s $5,000 deductible leaves the buyer paying $5,000 out of pocket versus $2,500 under the value policy. The “savings” evaporate on the first mid-size claim.

The Illinois Department of Insurance advises shopping for quotes with identical coverages before comparing prices, get the same dwelling limit, deductible, and liability limit from every carrier, then compare. Also ask about discounts: bundling home and auto with one carrier, installing monitored security systems, or adding smoke detectors can reduce premiums by 5% to 15% at many insurers. First-time buyers rarely ask. For specific strategies, our guide on how to save money on your homeowners insurance covers bundling and discount tactics in detail.

Carrier financial strength matters too. Check AM Best ratings before binding. A carrier rated A or better has the capital to pay large claims; a lower-rated carrier may not. Liability coverage is also where buyers routinely shortchange themselves. Our article on why liability lawsuits are quietly getting more expensive explains the trend.

Timing Coverage Around Closing: A Step Most Buyers Handle Wrong

Start shopping at least 30 days before your projected closing date. That’s not a conservative suggestion, it’s the practical minimum for getting accurate rebuild estimates, comparing carriers, and coordinating the binder with your lender’s requirements.

Your lender will require a declarations page or binder before funding. If you wait until the week before closing, you’re forced into whatever is available fast, not whatever is best. Once you’ve closed, confirm the transition from binder to final policy and verify that your first-year premium is either paid directly or rolled into escrow correctly. A coverage gap between binder expiration and policy issuance is rare but real, and it’s the buyer’s responsibility to confirm it doesn’t exist.

Where This Recommendation Falls Short

The advice in this article pushes toward higher coverage limits, replacement cost policies, and supplemental flood endorsements. That’s the right direction for most buyers. But there are genuine tradeoffs worth naming.

The biggest drawback is cost. In high-risk zip codes, coastal Florida, wildfire-prone California counties, Gulf Coast Texas, premiums for fully adequate replacement cost coverage with flood can exceed $5,000 to $8,000 per year. For buyers already stretched by down payment and closing costs, adding another $200 to $400 per month to escrow is a real strain. The catch is that this isn’t a reason to skip coverage; it’s a reason to budget for it earlier in the homebuying process, before the purchase price is already set.

There’s also a non-renewal risk that’s gotten worse in 2025 and 2026. Insurers have pulled back from high-risk markets, and some buyers who loaded their policies with endorsements and high limits have triggered non-renewal reviews at renewal time. This is not the norm, but it’s real in states like California and Florida where carriers are actively managing exposure. The tradeoff here: buying the maximum coverage is still correct, but buyers in high-risk zones should also ask their agent directly about the carrier’s appetite for their zip code before binding.

The flood insurance recommendation also has an exception: if your lender confirms you’re in FEMA Flood Zone X (minimal risk) and you’re in an inland region with no recent flood history, the probability-adjusted cost of flood coverage may not justify the premium. That’s a legitimate case for skipping it. For everyone else, especially anyone within a few miles of any body of water, skipping flood coverage is the risk.

Finally, the advice to choose the highest AM Best-rated carrier assumes similar pricing between carriers of different ratings. Where a highly rated carrier is materially more expensive, an A-rated carrier (not just A+) is still a sound choice. The goal is financial strength, not perfection.

How We Sourced This

This article draws from verified institutional sources including the Consumer Financial Protection Bureau, the Texas Department of Insurance, the Illinois Department of Insurance, the Washington State Office of the Insurance Commissioner, the Oklahoma Insurance Department, and the Joint Economic Committee of the U.S. Senate. Statistical data comes from the Insurance Information Institute (citing NAIC figures), the Consumer Federation of America, and Joint Economic Committee research, all published between 2022 and 2024. Deductible trend figures reflect 2025 market reporting from industry analysis available. Sources were selected based on institutional authority, recency, and direct relevance to first-time homebuyer coverage decisions. All URLs were verified as active and accurate at time of publication.

Frequently Asked Questions

How much dwelling coverage do I actually need for my first homeowners insurance policy?

You need enough to rebuild the home from the ground up at current labor and materials costs, not the purchase price, and not the market value. Request a replacement cost estimate from your insurer and cross-check it with an independent estimator like CoreLogic’s rebuild calculator. Many first-time policies are underinsured by 20% to 40%.

Does a standard homeowners policy cover flood damage?

No. Flood is explicitly excluded from virtually all standard homeowners policies. You need a separate flood policy, either through the NFIP or a private insurer. Only 4% of U.S. homeowners carry flood coverage, which means most are exposed to a risk their standard policy won’t pay for.

What’s the difference between replacement cost and actual cash value coverage?

Replacement cost pays what it actually costs to repair or replace the damaged item at current prices. Actual cash value subtracts depreciation first, so a 12-year-old roof that costs $18,000 to replace might pay out $7,000 under an ACV policy. For most first-time buyers, replacement cost coverage is worth the higher premium.

When should I start shopping for homeowners insurance before closing?

Start at least 30 days before your projected closing date. You’ll need time to get accurate dwelling estimates, compare carrier ratings, and deliver a binder or declarations page to your lender before funding. Waiting until the final week leaves you with no real negotiating position.

Can I just go with the insurance company my real estate agent or lender recommends?

You can, but compare it against at least two other quotes with identical coverage terms before accepting. The Oklahoma Insurance Department advises consumers to shop independently before committing. Agent-referred carriers may be perfectly good, the point is to verify that on your own terms.

Is personal liability coverage really necessary for a new homeowner?

Yes, and $100,000 is almost never enough. If someone is injured on your property and sues, medical costs and legal fees can exceed that limit quickly. The standard recommendation is $300,000 minimum, with a personal umbrella policy layered on top if you have a pool, dog, or trampoline.

How often should I review my homeowners policy after the first year?

At minimum, review it annually at renewal and any time you complete a significant improvement, a kitchen remodel, an addition, a new deck. Construction costs have risen enough in recent years that a policy written two years ago may already be underinsured. Ask your insurer about an inflation guard endorsement that automatically adjusts limits each year.

Sources

- Consumer Financial Protection Bureau, What Is Homeowners Insurance and Why Is It Required?

- Insurance Information Institute, Facts + Statistics: Homeowners and Renters Insurance

- Consumer Federation of America, Millions of Consumers Lack Vital Homeowners Insurance (2024)

- Joint Economic Committee, U.S. Senate, Climate Risks and the U.S. Insurance and Housing Markets (2024)

- Texas Department of Insurance, Tips for Shopping Homeowners Insurance

- Illinois Department of Insurance, Shopping Tips and Information for Homeowners Insurance

- Oklahoma Insurance Department, Choosing Your Homeowners Insurance Policy

- Washington State Office of the Insurance Commissioner, How Home Insurance Works

- Smart Insurance 101, Homeowners Insurance Guide: A Beginner’s Overview