Quick Answer

You need automobile insurance to protect yourself from financial loss, legal liability, and medical expenses after an accident. Nearly every U.S. state legally requires drivers to carry minimum liability coverage, and the average annual cost of full coverage auto insurance is approximately $2,150 per year according to recent industry data.

Buying a car is a significant milestone. For many people, it represents financial achievement, personal independence, and convenience in everyday life. Because a vehicle is such a valuable asset, protecting it, and yourself, against unexpected events becomes essential. One of the most reliable ways to safeguard that investment is by purchasing automobile insurance. The right insurance policy does far more than simply pay for repairs; it can provide financial protection, legal support, and peace of mind. Understanding how automobile insurance works, as well as knowing the different types of available coverage, can help you make an informed decision and comply with the requirements of your state.

Key Takeaways

- Automobile insurance is legally required in 49 out of 50 U.S. states, with minimum liability limits set by each state’s department of insurance, according to the Insurance Information Institute.

- The average full coverage auto insurance premium in the United States is approximately $2,150 per year–2026, per Bankrate’s auto insurance research.

- Uninsured drivers represent roughly 1 in 8 motorists on U.S. roads, making uninsured motorist coverage a critical protection layer, according to the Insurance Information Institute.

- Liability coverage typically includes two components: bodily injury liability and property damage liability, both of which are mandatory in most states per the National Association of Insurance Commissioners (NAIC).

- Drivers who bundle home and auto insurance can save an average of 16% on their premiums, according to Policygenius bundling data.

- Personal Injury Protection (PIP) is required in 12 no-fault states including Florida, Michigan, and New York, as outlined by the NAIC.

How Automobile Insurance Works: The Basics

Automobile insurance is a contractual agreement between you and an insurance company. You pay a recurring fee known as a premium, and in return, the insurer agrees to cover specific losses or expenses outlined in your policy. These losses may arise from accidents, theft, natural disasters, or other unforeseen incidents. Major insurers such as State Farm, GEICO, and Progressive are among the largest providers of personal auto insurance in the United States, collectively covering tens of millions of policyholders.

Most auto insurance policies cover three primary areas:

1. Property Coverage

This portion of your policy pays for damage to your car or covers you in the event your vehicle is stolen. Depending on the type of policy, it may apply to repairs, replacements, or other associated costs.

2. Liability Coverage

Liability insurance protects you if you are responsible for harming another person or damaging someone else’s property while driving. It can cover medical expenses, repair bills, and even legal judgments if you are sued after an accident.

3. Medical Coverage

Medical coverage helps pay for hospital visits, rehabilitation, and surgery. It may apply to you, your passengers, and in some situations, family members driving your vehicle.

Although nearly every U.S. state requires drivers to carry some form of auto insurance, the exact requirements vary widely. The National Association of Insurance Commissioners (NAIC) provides a detailed overview of state-by-state minimum coverage requirements. State laws typically include minimum liability limits, but the recommended amount of coverage often exceeds these minimums to ensure sufficient protection. Most insurance policies are issued for six-month or one-year terms, and your provider will notify you when it is time to renew.

One honest limitation worth knowing: carrying only the state minimum is cheap, but it frequently leaves real gaps. The average bodily injury liability claim exceeds $20,000, according to the Insurance Information Institute, and state minimums in many jurisdictions are set well below that threshold. If you cause a serious accident and your coverage is exhausted, your personal assets, savings, home equity, wages, can be targeted in a lawsuit. Minimum coverage is better than nothing, but it is not a strategy for anyone with meaningful assets to protect.

Why You Need Auto Insurance

1. Protect Your Vehicle

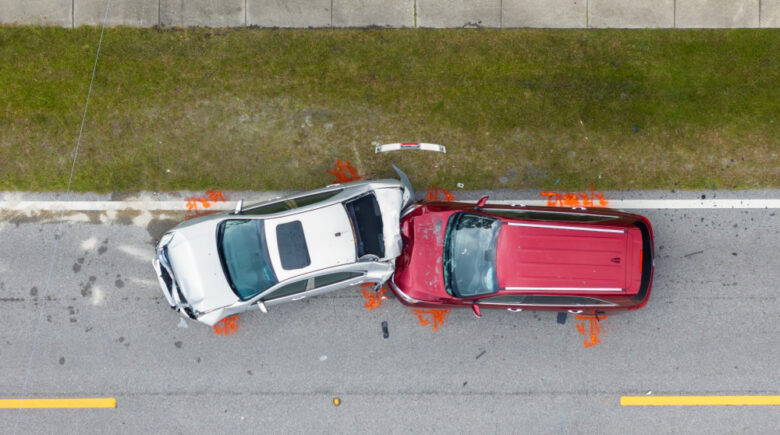

A primary reason to purchase auto insurance is to shield your vehicle from financial loss. Even the most experienced driver can face unexpected hazards, icy roads, distracted motorists, or falling tree branches. A well-chosen insurance policy can cover the cost of repairs or replacement after a collision or incident. According to the Insurance Information Institute, motor vehicle theft remains a significant concern, with hundreds of thousands of vehicles stolen each year in the United States. Beyond accidents, coverage for non-collision events can protect your vehicle against fire, vandalism, theft, and damage caused by floods or storms. Without insurance, these costs fall entirely on you.

2. Protect Yourself and Others

Accidents can happen in seconds, but the consequences may last much longer. Medical expenses following a crash can be substantial, even a minor accident may require X-rays, emergency room visits, or physical therapy. More serious collisions may involve surgeries, long-term rehabilitation, or extended hospital stays. According to the National Highway Traffic Safety Administration (NHTSA), the economic cost of motor vehicle crashes in the United States runs into hundreds of billions of dollars annually when medical expenses, lost productivity, and property damage are combined. Auto insurance can help cover these expenses for both you and your passengers, reducing the financial strain during an already stressful time.

3. Cover Third-Party Damages

Third-party damages can be especially costly. If you damage someone else’s vehicle, property, or injure a pedestrian or motorist, you may be held financially responsible. Liability insurance ensures these expenses are covered without draining your personal savings. This type of coverage is essential for meeting legal requirements in most states and for protecting your financial future. Without it, even a single mistake on the road could lead to hundreds of thousands of dollars in liability. The Insurance Information Institute notes that the average bodily injury liability claim exceeds $20,000, which is why carrying only the state minimum is often insufficient.

4. Protect Yourself From Legal Expenses

Lawsuits related to car accidents are increasingly common. If another party decides to sue you for damages, your insurance policy can cover legal fees, settlements, and other court-related costs. Attorney fees and court expenses can add up quickly, making legal protection one of the most valuable aspects of a solid auto insurance policy. The Insurance Information Institute emphasizes that liability coverage provides a critical legal defense layer that most drivers cannot afford to be without. Knowing you are protected can give you greater confidence every time you drive.

Types of Automobile Insurance Coverage You May Need

| Coverage Type | What It Covers | Required by Law? | Average Annual Cost (2025–2026) |

|---|---|---|---|

| Liability (Bodily Injury & Property Damage) | Injuries and property damage you cause to others | Yes, in 49 states | $650 – $900 |

| Collision | Damage to your vehicle from crashes with cars or objects | Required by most lenders | $400 – $700 |

| Comprehensive | Theft, vandalism, natural disasters, animal strikes | Required by most lenders | $160 – $300 |

| Personal Injury Protection (PIP) | Medical bills, lost wages, rehabilitation (regardless of fault) | Required in 12 no-fault states | $100 – $250 |

| Medical Payments (MedPay) | Medical expenses for you, household members, and passengers | Optional in most states | $50 – $120 |

| Uninsured/Underinsured Motorist | Your costs when the at-fault driver has no or insufficient insurance | Required in 22 states | $80 – $200 |

Liability Coverage

Liability coverage is mandatory in most states, except New Hampshire and Virginia, which allow alternative financial responsibility options. It covers the costs associated with injuring another person or damaging their property in an accident that you cause. This includes medical bills, car repairs, and legal judgments. Liability insurance is typically offered as a package consisting of bodily injury liability and property damage liability. The NAIC recommends carrying liability limits well above state minimums, as minimum limits often fail to cover the full cost of serious accidents.

Uninsured and Underinsured Motorist Coverage

Not all drivers carry adequate insurance, despite legal requirements. According to the Insurance Information Institute, approximately 1 in 8 drivers in the United States is uninsured. If an uninsured driver hits your vehicle, uninsured motorist coverage can pay for your medical bills or repair costs. Underinsured motorist coverage applies when the at-fault driver has insurance, but their policy limits are too low to cover all your expenses. Several states require these coverages, but even where they’re optional, they are highly recommended for added protection.

Comprehensive and Collision Coverage

Collision and non-collision (comprehensive) coverage are usually sold together and provide broad protection for your vehicle. Collision coverage pays for damage resulting from crashes with other cars or fixed objects. Comprehensive coverage applies to non-collision events like theft, natural disasters, vandalism, floods, or animal strikes. If your car is financed or leased, your lender will likely require both. Lenders such as Chase Auto and other major financial institutions typically include mandatory coverage requirements in their loan agreements to protect the value of the collateral.

Personal Injury Protection (PIP)

PIP covers medical expenses for you and your passengers regardless of who is at fault. Beyond medical bills, it may reimburse lost wages and rehabilitation costs, expenses that traditional health insurance sometimes excludes. Some states require PIP, while in others it is optional. In states with no-fault insurance laws, such as Florida, Michigan, New York, and New Jersey, PIP is a mandatory component of every auto policy, as explained by the Insurance Information Institute’s no-fault insurance guide.

Medical Payments Coverage (MedPay)

Similar to PIP but more limited, Medical Payments Coverage helps pay for medical expenses such as hospital visits, X-rays, and surgery. It applies to you, your household members, and passengers in your vehicle. MedPay does not cover lost wages or rehabilitation services, which is what distinguishes it from PIP. For drivers in states where PIP is not available, MedPay can serve as a useful supplement to existing health insurance coverage.

How to Purchase Auto Insurance

When shopping for auto insurance, avoid focusing solely on the cheapest price. Insurance companies use different formulas to calculate premiums, so costs can vary significantly among providers. Comparison tools from platforms such as Policygenius and NerdWallet’s auto insurance comparison tool allow you to evaluate multiple insurers side by side. To find the best value, request quotes from multiple insurers or work with a licensed insurance broker who can help you compare your options. Your premium may also be influenced by your driving record, the type of vehicle you drive, your ZIP code, and in some states, your credit score, a metric that major credit bureaus such as Experian and Equifax help insurers assess.

Ask about available discounts as well. Many insurers offer savings for safe drivers, students with good grades, vehicles with advanced safety features, and bundling home and auto policies. Taking advantage of these discounts can reduce your insurance costs while maintaining strong protection. According to Policygenius, bundling home and auto insurance can save drivers an average of 16% on their combined premiums.

Frequently Asked Questions

Is automobile insurance legally required in every U.S. state?

Almost universally, yes. 49 out of 50 states require drivers to carry minimum liability coverage. New Hampshire and Virginia allow alternatives to traditional insurance, such as posting a financial security bond, but even these states impose strict financial responsibility requirements. Driving without proof of insurance in states that require it can result in fines, license suspension, and vehicle impoundment.

What is the minimum auto insurance coverage I need?

Minimum requirements vary by state and are set by each state’s department of insurance. Most states require at minimum a specific dollar threshold of bodily injury liability per person, a higher limit per accident, and a property damage liability amount. A common minimum is 25/50/25, meaning $25,000 per injured person, $50,000 per accident, and $25,000 for property damage. Experts strongly recommend carrying limits well above these minimums, as real-world accident costs frequently exceed them.

How is my auto insurance premium calculated?

Insurers use a combination of factors to calculate your premium, including your driving record, age, vehicle make and model, annual mileage, ZIP code, and in most states, your credit-based insurance score. Credit bureaus such as Experian and Equifax provide data that insurers use to assess financial risk. Safe driving history, newer vehicles with safety features, and good credit can all contribute to lower premiums.

What is the difference between comprehensive and collision coverage?

Collision coverage pays for damage to your vehicle caused by a crash with another vehicle or a stationary object. Comprehensive coverage covers losses from non-collision events such as theft, fire, vandalism, hail, flooding, or striking an animal. Both are typically required by lenders when a vehicle is financed or leased. Together, they are often referred to as “full coverage” alongside liability insurance.

What happens if an uninsured driver hits me?

Uninsured motorist coverage is specifically designed to protect you in this scenario. It pays for your medical bills, lost wages, and vehicle repair costs when the at-fault driver has no insurance. If the at-fault driver has insurance but insufficient limits to cover your damages, underinsured motorist coverage fills that financial gap. The Insurance Information Institute estimates that approximately 1 in 8 U.S. drivers is currently uninsured, making this coverage particularly valuable.

Does auto insurance cover a rental car?

It depends on your policy. Many standard auto insurance policies extend your existing liability, collision, and comprehensive coverage to rental vehicles used for personal purposes. However, this extension is not universal, and coverage limits may differ. Some drivers also have rental car coverage through their credit cards. Review your policy details or call your insurer before declining rental car coverage at the rental counter.

What is Personal Injury Protection (PIP) and do I need it?

Personal Injury Protection (PIP) covers medical expenses, lost wages, and certain rehabilitation costs for you and your passengers regardless of fault. It is mandatory in the 12 no-fault insurance states, which include Florida, Michigan, New York, New Jersey, Pennsylvania, Hawaii, Kansas, Kentucky, Massachusetts, Minnesota, North Dakota, and Utah. In states where PIP is optional, it can be a valuable supplement to your health insurance, especially if your health plan carries high deductibles or gaps in coverage.

How can I lower my auto insurance premiums?

Several proven strategies can reduce your premium without sacrificing important coverage. Maintaining a clean driving record and increasing your deductible are the two most reliable levers. Bundling home and auto policies saves drivers an average of 16%, according to Policygenius. Completing a defensive driving course, driving a vehicle with advanced safety features, and shopping quotes from multiple insurers annually all help as well. Comparison platforms like Policygenius and NerdWallet make multi-quote comparisons straightforward.

What is the difference between PIP and MedPay?

Both Personal Injury Protection (PIP) and Medical Payments Coverage (MedPay) pay for medical expenses after an accident regardless of fault. However, PIP is broader, it can also reimburse lost wages, childcare costs during recovery, and other non-medical expenses. MedPay is narrower and is limited strictly to medical and funeral expenses. PIP is required in no-fault states, whereas MedPay is an optional add-on in most states.

Does my credit score affect my auto insurance rate?

In most U.S. states, yes. Insurers use a credit-based insurance score, which draws on data from credit bureaus such as Experian, Equifax, and TransUnion, to help predict the likelihood of future claims. Drivers with lower credit scores often pay significantly higher premiums than those with strong credit. A handful of states, including California, Hawaii, and Massachusetts, prohibit insurers from using credit scores in auto insurance pricing. The Federal Trade Commission (FTC) has studied the relationship between credit scores and insurance risk in detail.

Is auto insurance worth carrying if I drive very little?

Yes, though the math changes. Liability coverage is legally required regardless of how many miles you drive, so you cannot opt out simply because you rarely use your car. Low-mileage drivers may qualify for pay-per-mile or usage-based insurance programs offered by carriers such as Progressive and others. These programs can produce meaningful savings for drivers who log under 7,500 miles annually. Dropping collision or comprehensive on an older, fully paid-off vehicle with low market value is another way to trim costs, just recognize you absorb any repair or replacement bill yourself if something goes wrong.

Sources

- Insurance Information Institute, Auto Insurance Basics

- National Association of Insurance Commissioners (NAIC), Auto Insurance Consumer Guide

- NerdWallet, Auto Insurance Guide and Comparison Tool

- Policygenius, Auto Insurance Overview

- Insurance Information Institute, Facts and Statistics: Uninsured Motorists

- Insurance Information Institute, Facts and Statistics: Auto Theft

- Insurance Information Institute, No-Fault Auto Insurance Explained

- Insurance Information Institute, Liability Coverage Overview

- State Farm, Auto Insurance Coverage Options

- Progressive, Auto Insurance Overview