Fact-checked by the Smart Insurance 101 editorial team

Quick Answer

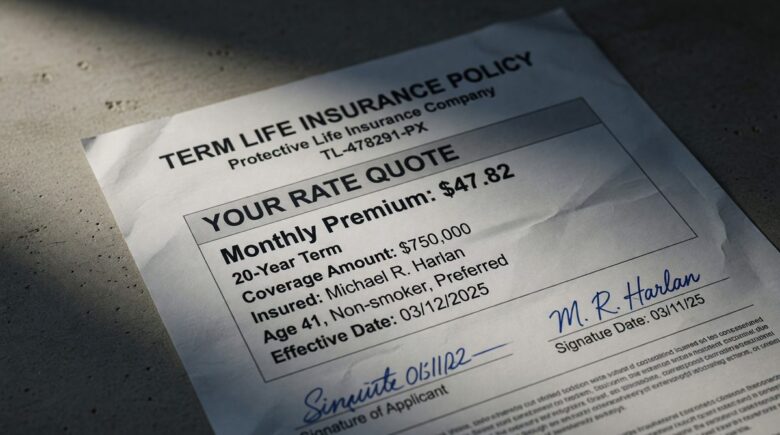

New parents lock in the lowest term life rate by applying before age 35 and before any post-pregnancy health changes are flagged in underwriting. A healthy 30-year-old male pays roughly $213 per year for a $500,000 20-year policy; waiting until 40 raises that to $321 per year, a permanent increase on every future premium.

The real question new parents face is not whether to buy term life insurance, but whether waiting even two or three years after a baby arrives will cost them significantly more, and the answer is yes. The term life rate new parent window is narrower than most people assume, because insurers price premiums based on your age and health class at the moment you apply, and both tend to move in the wrong direction after childbirth. According to LIMRA’s 2025 Insurance Barometer Study, healthy adults aged 18–30 overestimate the cost of a $250,000 20-year term policy by 10–12 times its actual price, meaning sticker shock is keeping many parents from acting when rates are still low.

Timing is the one underwriting factor entirely within your control. Everything else, your health history, your family’s medical record, your weight at exam time, can shift after a baby is born. Acting early is the clearest way to protect your family at the lowest permanent cost.

Why Do Term Life Rates Rise After a Child Is Born?

Age is the single largest driver of term life premiums, and it moves in only one direction. Insurers price risk by actuarial age bands, so a policy bought at 30 is permanently cheaper than the same policy bought at 33, even if nothing else about your health has changed. The cost difference is not trivial.

Look at the numbers side by side. NerdWallet’s 2026 rate data shows a preferred nonsmoking 30-year-old male pays an average of $213 per year for a $500,000 20-year term policy. The same preferred nonsmoking male at 40 pays $321 per year, a difference of $108 annually. Over a 20-year term, that gap compounds to $2,160 paid for an identical benefit, simply because of a decade’s delay.

The age jump is only part of the problem. Pregnancy and the postpartum period can introduce new health factors that affect underwriting classification. Gestational diabetes, elevated blood pressure recorded during prenatal visits, C-section complications, or postpartum thyroid changes can all appear in your medical records. Insurers pull those records during underwriting, and a condition noted even as “resolved” can move an applicant from a preferred rate class to a standard or substandard class, raising premiums by 25–50% or more over preferred rates. The risk is not hypothetical, it is baked into how medical underwriting works.

For a fuller grounding in how life insurance products are structured and why term coverage fits most young families, the overview at Life Insurance 101: Types, Features, and Principles Explained is a useful starting point before you request quotes.

Key Takeaway: Age and post-pregnancy health changes are the two main forces pushing term life premiums higher after a baby arrives. A $108 annual difference between buying at 30 vs. 40, per NerdWallet’s 2026 data, totals more than $2,000 over a 20-year term for an identical benefit.

How Insurers Calculate and Lock In Your Term Life Rate

Your premium is set once at application and never changes for the life of the policy, which is precisely why the date you apply matters so much. Insurers assign applicants to a health class during underwriting, and that class, combined with your age, determines every payment you will make for the next 20 or 30 years.

The Four Main Health Classifications

Most major carriers use four tiers: Preferred Plus (also called Preferred Elite or Super Preferred), Preferred, Standard, and Substandard (rated). Preferred Plus is reserved for applicants with near-perfect health metrics, ideal cholesterol, blood pressure, no tobacco, no chronic conditions, and a clean family history. Preferred accepts slightly wider parameters. Standard is where most Americans land, and substandard applies when medical history raises the insurer’s assessed risk.

The practical gap between Preferred Plus and Standard can be substantial. For a $500,000 20-year policy on a 32-year-old male, the difference between those two classes often runs 30–40% in annual premium. For new parents, this means a gestational diabetes diagnosis, even one that fully resolved after delivery, can push an otherwise Preferred applicant into Standard territory until a waiting period passes, often 12 months post-delivery with normal A1C readings documented.

Worked Example: The True Cost of Waiting Two Years

Suppose a parent is 30 years old today and qualifies for preferred rates. At $213 per year for a $500,000 20-year policy, that is $17.75 per month. If that same parent waits until age 32 and still qualifies for preferred rates, industry data suggests a monthly cost closer to $21–$22. Over the full 20-year term, the two-year delay adds roughly $800–$1,000 in total premiums paid, for identical coverage. Waiting until 35 widens the gap further still.

| Age at Application | Health Class | Est. Annual Premium (Male, $500K 20-yr) | 20-Year Total Cost |

|---|---|---|---|

| Age 30 | Preferred | $213 | $4,260 |

| Age 35 | Preferred | ~$260 | ~$5,200 |

| Age 40 | Preferred | $321 | $6,420 |

| Age 30 | Standard (post-pregnancy reclassification) | ~$300–$320 | ~$6,000–$6,400 |

Sources: NerdWallet 2026 rate averages; age 35 estimated from published band data. Standard-class adjustment based on typical 30–40% uplift over preferred rates.

Key Takeaway: A term life rate is locked permanently at application. Preferred-class buyers at age 30 pay $213 per year for $500,000 in coverage, per NerdWallet, while a standard-class reclassification from a resolved pregnancy condition can push that same buyer to $300-plus annually, the same cost as waiting a full decade.

Optimal Timing: Before Pregnancy, During, or After Birth?

Pre-pregnancy is the lowest-rate window, full stop. Applying before conception locks in your current health class with no pregnancy-related medical records in play. Most parents do not plan their insurance timeline around a future pregnancy, so the more common question is: when is the next best moment after a baby arrives?

Active pregnancy is a complicated window. Insurers treat pregnancy as a standard exclusion for certain additional coverage types, and medical underwriting during pregnancy may flag elevated blood pressure, weight gain beyond normal ranges, or gestational conditions. Several carriers will defer a final decision or issue only standard rates until after delivery and recovery. New York Life and Guardian both advise clients to lock in coverage before pregnancy for this reason, though they will underwrite during pregnancy at standard or higher rates depending on the course of the pregnancy.

After delivery, the practical guidance is to apply within 6–12 months of birth, once the medical record reflects a clean post-partum recovery. If gestational diabetes was diagnosed, most carriers want to see a normal A1C (typically below 5.7%) documented at a follow-up visit before restoring preferred classification. C-section recovery alone generally does not affect rate class once the applicant is fully healed and there are no lingering complications.

The no-exam accelerated underwriting products available in 2026, offered by carriers including Ladder, Haven Life (backed by MassMutual), and Bestow, can compress the approval timeline to 24–72 hours for applicants under 45 who meet algorithmic health thresholds. For a new parent in good health who wants speed, these products are a legitimate option. The trade-off: coverage caps typically top out at $1 million to $3 million, and the carrier’s algorithm may decline applicants with recent pregnancy-related diagnoses even if those conditions resolved cleanly.

Key Takeaway: Pre-pregnancy is the lowest-rate application window, but parents who miss it should apply within 12 months of delivery once recovery is documented. Accelerated underwriting from carriers like Ladder or Haven Life can return a decision in as little as 24 hours, though recent pregnancy flags may still trigger a full medical review.

How Much Coverage Do New Parents Actually Need?

Coverage amount and term length are decisions that directly shape your monthly payment, so getting them right matters as much as timing. Most financial planners point to a range of 10–12 times annual income as a starting benchmark for life insurance coverage, but new parents have additional layers to account for: outstanding mortgage balance, student loan debt that a co-signer would inherit, and the actual cost of raising a child to adulthood.

The U.S. Department of Agriculture’s most recent child-rearing cost estimates, before updating for post-pandemic inflation, placed the cost of raising one child from birth to age 17 at over $310,000 for a middle-income family. Add the income replacement your household needs for 15–20 years, and a $500,000 policy may be the floor for many dual-income households, not the ceiling.

20-Year vs. 30-Year Term: The Trade-Off

A 20-year term is the most commonly purchased length, and it aligns well with most families’ major financial obligations: the mortgage, the years before a child reaches college, and peak income-replacement needs. A 30-year term provides longer protection but at a higher monthly cost. For a 30-year-old paying $17.75 per month on a 20-year preferred-class policy, the 30-year equivalent may run $27–$32 per month from the same carrier, a meaningful difference over three decades.

Conversion riders are worth requesting when buying any term policy as a new parent. A conversion rider lets you convert part or all of your term coverage to a permanent policy later without a new medical exam. If your health declines in year 12 of a 20-year term, you will not be able to buy new coverage at preferred rates, but a conversion rider preserves that option. Not every carrier includes it at no cost; ask about it explicitly before signing. For a broader view of how coverage types compare, the guide to types of insurance and their benefits breaks down the differences in plain language.

Key Takeaway: New parents should target coverage of at least 10–12 times annual income plus outstanding debts. A 20-year $500,000 policy costs roughly $26 per month for a 40-year-old preferred buyer; requesting a conversion rider at purchase preserves the option to extend coverage without new medical underwriting if health declines later.

Frequently Asked Questions

What is the best time for a new parent to buy term life insurance?

Before pregnancy is the lowest-rate window because no prenatal health records are in the underwriting file. If that window has passed, apply within 12 months of delivery once post-partum recovery is documented, ideally before any birthday that moves you into a new actuarial age band.

Does gestational diabetes affect my term life insurance rate?

Yes, it can. Most carriers will not issue preferred-class rates if gestational diabetes appears in recent medical records, even if it resolved after delivery. The standard waiting period before reclassification to preferred is roughly 12 months of documented normal blood sugar levels, typically an A1C below 5.7%.

How much does a $500,000 term life policy cost for a 30-year-old parent?

A preferred nonsmoking 30-year-old male pays an average of $213 per year, about $17.75 per month, for a $500,000 20-year term policy, per NerdWallet’s 2026 rate data. Rates for women tend to run 10–20% lower at the same age and health class. Standard-class rates can be 30–40% higher than preferred for either sex.

Can I get term life insurance while pregnant?

Most major carriers will underwrite during pregnancy, but preferred-class approval is unlikely until after delivery and recovery. Some carriers issue standard rates during an uncomplicated pregnancy; others defer the decision until post-partum. Applying while pregnant is better than not applying at all, but the rates may be higher than if you had applied before conception.

Should I use a no-exam policy as a new parent to get covered faster?

No-exam accelerated underwriting from carriers like Ladder and Haven Life can approve coverage in 24–72 hours, a genuine advantage for parents who need protection quickly. The downside is that algorithmic screening may reject applicants with recent pregnancy-related diagnoses, and coverage is usually capped below $3 million. If you are in clean health and the coverage limit fits your needs, it is a sound option. If your situation is more complex, a fully underwritten policy with a licensed agent is the safer path, and comparing options across carriers is essential either way, as shown in our review of the best term life insurance companies for 2026.

Sources

- LIMRA, 2025 Insurance Barometer Study: Adults Age 30 and Younger Overestimate Life Insurance Cost by 10-12 Times

- NerdWallet, Average Life Insurance Rates (2026)

- Insurance Information Institute, Types of Term Life Insurance Policies

- National Association of Insurance Commissioners, Life Insurance Topic Overview

- Smart Insurance 101, Best Term Life Insurance Companies for 2026