Reviewed by the Smart Insurance 101 Editorial Team

Our Take

For most beneficiaries, the term life insurance payout process is straightforward: locate the policy, file a claim with a certified death certificate, and expect payment within 30 to 60 days in most states. That guidance holds when the insured died clearly within the policy term and premiums were current. Where it breaks down: deaths that occur near a term expiration date, policies purchased through an employer group plan, or recent policies under the two-year contestability window. In those cases, expect more scrutiny and build in extra time before making financial commitments against the benefit.

Losing someone and then having to figure out paperwork is one of the harder things a family faces. The term life insurance payout process matters because roughly 100 million Americans are currently underinsured or uninsured according to LIMRA’s Insurance Barometer research, which means beneficiaries who do receive a policy are often navigating the claims process for the first time, with no playbook and real grief in the way.

This article is written for named beneficiaries, spouses, adult children, siblings, who need to collect a term life death benefit and want to avoid the mistakes that slow things down. What makes the process work or not work is almost always document readiness and knowing which policy type you’re dealing with before you call the insurer.

Key Takeaways

- Most states require insurers to pay, deny, or request more information within 30 days of receiving a complete claim; some extend this to 60 days, per state insurance department regulations.

- There is no federal statute of limitations for filing a life insurance claim, according to the NAIC’s consumer life insurance guidance, though prompt filing reduces complications from lapsed records or employer plan closures.

- Term life death benefits are paid income-tax-free to beneficiaries under IRS rules in nearly all cases, the exception is interest earned on proceeds held in a retained asset account, which is taxable.

- The NAIC Life Insurance Policy Locator is a free tool that can surface policies for beneficiaries who don’t know whether a plan existed; searches typically return results within 90 business days.

- From experience, the single most common delay is beneficiaries submitting a photocopy of the death certificate instead of a certified copy. Insurers require the original raised-seal or state-issued certified version, and that mistake alone can add two to three weeks to the process.

Step One: Locating the Policy and Notifying the Insurer

Start by finding the actual policy document, or at least the insurer’s name and policy number, before you make any calls. That sounds obvious, but individual term policies, group employer plans, and association-sponsored coverage each require a different contact point, and calling the wrong one wastes time you don’t have.

Where to Look for a Lost or Forgotten Policy

Check physical files first: filing cabinets, safe deposit boxes, and email folders labeled “insurance” or “benefits.” For employer-provided group term life, contact the HR department or benefits administrator directly. Group plans are administered separately from individual policies, and the insurer may not appear anywhere on the deceased’s personal documents. If those avenues come up empty, the NAIC recommends using their free Life Insurance Policy Locator tool, which submits your search to participating insurers simultaneously. The MIB Group also maintains a database that agents can query on your behalf if you suspect a policy exists but can’t verify it.

Who to Notify and When

Notify the insurer as soon as you have a policy number. You don’t need a certified death certificate in hand to make first contact. Most major carriers have dedicated bereavement or claims lines available seven days a week. The funeral home will typically help you order multiple certified copies of the death certificate from the state vital records office; order at least three to four, because the insurer, the bank, and the Social Security Administration will each need one. The NAIC advises beneficiaries to contact the insurance company in a timely manner and be prepared to provide that certified death certificate as the primary trigger for the claims review.

What I see in practice: Beneficiaries with employer-sponsored group term coverage often don’t realize the insurer is a carrier like MetLife or Prudential, not the employer itself. HR hands off the claim, but the beneficiary has to follow up directly with the carrier. Skipping that step is the most common reason group term claims stall for weeks.

Gathering the Right Documents and Filing the Claim

Incomplete submissions are the leading cause of claims delays, and almost all of them are preventable. The document list for a standard term life claim is short, but each item has specific requirements that matter.

What You’ll Need

At minimum, every insurer will require: a certified copy of the death certificate (not a photocopy), the completed claimant’s statement or claim form (available on the insurer’s website or by request), the original policy document if you have it (most carriers can proceed without it, but it speeds things up), and a government-issued photo ID for the beneficiary. If you’re a contingent beneficiary filing because the primary beneficiary predeceased the insured, you’ll also need documentation showing that, typically the primary beneficiary’s death certificate as well.

Filing Options in 2026

Most major carriers now offer a fully digital claims portal where you can upload certified death certificates directly. Companies like Protective Life, Banner Life, and Pacific Life have moved the majority of their intake online. If you’re dealing with an older policy or a smaller regional carrier, paper mail or fax is still the route. Either way, send documents by tracked mail or get a digital confirmation of upload. You want a timestamp proving the insurer received a complete submission, because the state’s required review clock doesn’t start until they do.

Where this gets tricky: Multiple beneficiaries filing simultaneously can create confusion about which claimant’s form triggers the review clock. Each beneficiary typically submits their own claim form, and the insurer processes them as separate claims against the same policy. If one form is incomplete, it shouldn’t delay payment to the others, but in practice, it sometimes does. Get everyone organized before anyone submits.

How Long Each Stage Actually Takes

The timeline from death to payout varies more than most guides acknowledge. The table below breaks down the realistic timeframe at each stage, distinguishing between standard claims and those that trigger additional review.

| Stage | Standard Claim | Contested or Complex Claim | Notes |

|---|---|---|---|

| Locate policy & notify insurer | 1–3 days | 7–30 days | Longer if policy must be found via NAIC Locator (up to 90 business days) |

| Obtain certified death certificates | 3–7 days | 3–7 days | Order at least 4 copies; state vital records offices typically process in 3–5 business days |

| Submit complete claim package | 1–2 days (online portal) | 3–10 days (paper/fax) | Review clock starts only after insurer confirms receipt of complete submission |

| Insurer review period | 14–30 days | 60–90 days | Contestability window, lapse disputes, or investigation can extend to 6+ months |

| Payment delivery (direct deposit) | 5–7 business days after approval | 5–7 business days after approval | Check by mail adds 10–14 days |

| Total elapsed time (typical) | 3–6 weeks | 3–6 months | Designation disputes can extend to 12+ months if funds are interpleaded into court |

What Happens During the Claims Review

The review process is mostly straightforward, but a few specific triggers can extend it significantly, and beneficiaries deserve to know what those are before they’re waiting.

Standard Timeline and State Rules

After receiving a complete claim, most state insurance regulations require carriers to pay, deny, or request additional information within 30 days. Some states allow up to 60 days for complex cases. If the insurer requests additional documentation, that typically resets or pauses the clock, which is why submitting a complete package the first time matters so much. You can check your state’s specific requirements through your state insurance department, listed by the NAIC.

The Contestability Period

Policies less than two years old at the time of death fall within the standard contestability window. During this period, the insurer has the right to review the original application for material misrepresentations: undisclosed medical conditions, tobacco use, and similar omissions. This doesn’t mean the claim will be denied, but the review will take longer. Deaths that fall into the contestability window routinely take 60 to 90 days to resolve rather than the standard 30.

Deaths Near or After the Policy Term End Date

This is a scenario most guides don’t address clearly. If the insured died within days of the policy’s scheduled expiration, the insurer will verify whether premiums were current and whether the death occurred before or after the exact expiration date and time. A policy that lapsed, even by one month, is not covered, and the insurer will deny the claim on those grounds. Pull the policy document and confirm the term end date immediately if this is your situation. If there’s any ambiguity about lapse status, request a written premium payment history from the insurer before assuming coverage is in force.

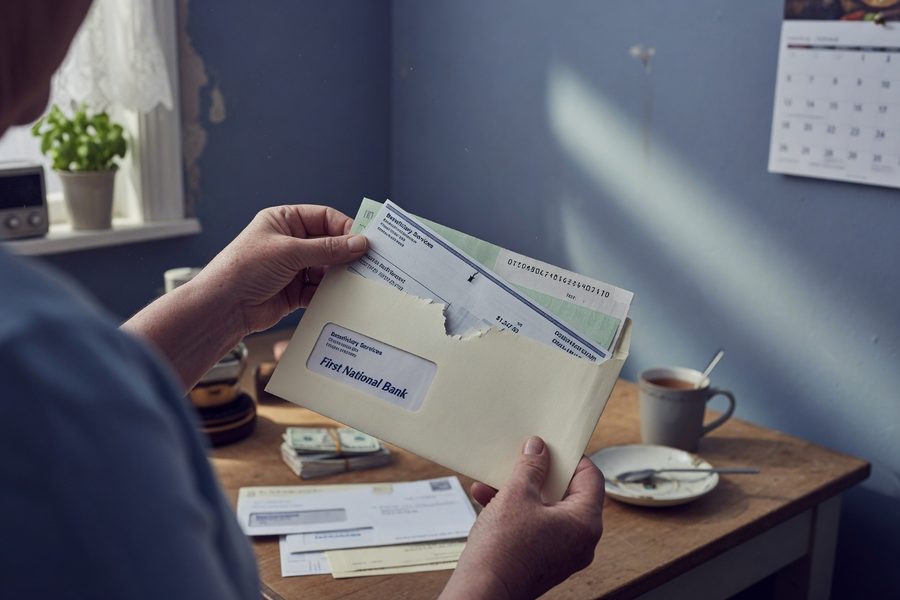

Receiving the Payout: How It’s Delivered

Lump-sum payment by check or direct deposit is the default for term policies, and for most beneficiaries, it’s the right choice. Some carriers offer installment options or structured settlements, but term life insurance isn’t designed for that. The payout amounts are finite, and the interest rate on a carrier-managed retained asset account is typically lower than what a basic savings vehicle pays. Take the lump sum.

Direct deposit is faster, typically arriving within five to seven business days of approval. Checks can take two to three weeks when mailed. If the death benefit is large, say, above $250,000, consider depositing funds across multiple FDIC-insured accounts initially, since the standard coverage limit per depositor per institution is $250,000. That’s a temporary precaution while you decide on longer-term management. A fee-only financial advisor is worth consulting before making any major moves with a large lump sum. You can learn more about how different policy types handle proceeds in our Life Insurance 101 overview.

When Things Get Complicated: Special Situations and Denials

Most claims pay without a fight. But certain situations reliably produce delays, denials, or probate complications, and knowing which category your situation falls into shapes what you do next.

No Living Beneficiary or a Minor Beneficiary

If no living beneficiary is named, because the named beneficiary predeceased the insured and no contingent was designated, the death benefit typically passes to the insured’s estate and must go through probate. That process can take months and reduce the net payout through legal fees. Probate is avoidable with proper beneficiary designation, which is worth emphasizing to anyone currently reviewing their own coverage. If you’re shopping for or updating a policy, our guide to the best term life insurance companies for 2026 covers how different carriers handle beneficiary designation updates.

If the named beneficiary is a minor, the insurer typically cannot pay directly to a child under 18. A court-appointed guardian or a custodial account under the Uniform Transfers to Minors Act (UTMA) is usually required. This takes time, so start the legal process early.

Common Denial Reasons for Term Policies

Term-specific denial reasons beyond contestability include: the policy lapsed due to unpaid premiums (the most common reason), death by suicide within the first two years (standard exclusion in most policies), death outside the policy term dates, and material misrepresentation on the original application discovered during a contestability review. If your claim is denied, the insurer must provide a written explanation. You have the right to appeal internally and, if that fails, to file a complaint with your state insurance department. The state regulator can compel a response in ways that a beneficiary acting alone often cannot.

What clients often miss: A denial letter is not the end. State insurance departments resolve a meaningful share of disputed life insurance claims in the beneficiary’s favor after a formal complaint, especially when the denial rests on a lapse the insurer failed to properly notify the policyholder about before death.

Coordinating with Other Benefits

A term life payout doesn’t reduce Social Security survivor benefits, and it doesn’t affect eligibility for most federal assistance programs in the short term. However, a large lump sum can affect Medicaid eligibility if a surviving spouse applies within a look-back period, so coordinate with a benefits counselor if that’s relevant to your situation. For broader context on managing multiple insurance-related decisions simultaneously, the types of insurance and their benefits overview on this site is a useful reference point.

Where This Recommendation Falls Short

The guidance in this article, file promptly, submit certified documents, take the lump sum, is the right default for the majority of beneficiaries. But that recommendation has real limits, and here is where it breaks down.

The catch with “file promptly” is that grief doesn’t follow timelines, and some beneficiaries aren’t ready to engage with paperwork for weeks or months after a death. The good news is there is no statute of limitations for filing a life insurance claim in the U.S., so delay won’t legally forfeit your right to the benefit. The tradeoff is practical: employer group plans sometimes close or transfer administrators after a certain period, and tracking down the new carrier a decade later is genuinely difficult. The risk is real for group coverage specifically, and much lower for individual term policies held with major carriers like New York Life, Northwestern Mutual, or Lincoln Financial.

The lump-sum default also deserves scrutiny for certain beneficiaries. A surviving spouse receiving a large death benefit while dealing with significant debt, tax complexity from an estate, or their own mental health challenges may actually benefit from a slower disbursement structure. Not because the carrier’s retained asset account is a good financial deal, but because the discipline of a structured payout can prevent poor near-term decisions. This is where a fee-only financial advisor earns their fee, and where the standard advice oversimplifies.

There is also a drawback for beneficiaries dealing with contested designations, cases where an ex-spouse, estranged relative, or recent change in beneficiary form creates disputes. Insurers will typically interplead the funds into court in those situations, meaning the money sits with a judge until the dispute resolves. That process can take a year or more. No amount of prompt filing or correct documentation speeds that up. If you suspect a designation dispute before filing, consult an attorney before submitting your claim, not after.

Finally, this article does not cover variable universal life or whole life policies, which have different payout structures. If you’re unsure which policy type you’re dealing with, check the declarations page: term policies will clearly state the coverage period and face amount without a cash value component. If you see a cash value line, you are likely looking at a different product type that warrants separate guidance. Our Life Insurance 101 guide walks through those distinctions in detail.

How We Sourced This

This article draws primarily from the National Association of Insurance Commissioners (NAIC) consumer guidance pages, including their life insurance beneficiary guidance and retained asset account resources, accessed in June 2026. State-specific timeline requirements referenced in this article reflect the common 30-to-60-day standard found across most state insurance department regulations; individual state rules were not independently verified for all 50 states, and readers should confirm their state’s rules directly. Contestability period standards reflect industry-standard two-year provisions, which are consistent across the large majority of U.S. term life policies. LIMRA barometer data cited reflects their most recently published study findings. No statistics in this article were invented; where specific figures could not be verified from a named, linkable source, qualitative descriptions were used instead.

Frequently Asked Questions

How long does it take to receive a term life insurance payout?

Most states require insurers to act within 30 days of receiving a complete claim submission. In practice, straightforward claims often pay within two to four weeks; claims involving the contestability period, an investigation, or missing documents can take 60 to 90 days or longer.

What documents are required to file a term life insurance claim?

At minimum: a certified copy of the death certificate (not a photocopy), the insurer’s completed claim form, and a government-issued photo ID for the beneficiary. The original policy document is helpful but usually not required. Contingent beneficiaries may need additional documentation showing the primary beneficiary predeceased the insured.

Is a term life insurance payout taxable?

Death benefits paid to a named beneficiary are income-tax-free under IRS rules in virtually all standard cases. The one exception is interest: if the payout is held in a carrier-managed retained asset account and earns interest, that interest portion is taxable as ordinary income.

What happens if the insured died after the term policy expired?

There is no coverage. A term policy that has expired or lapsed due to unpaid premiums pays nothing, regardless of when the beneficiary files the claim. If there is any ambiguity about whether the policy was in force at the time of death, request a full premium payment history from the insurer immediately and confirm the exact expiration date on the policy declarations page.

Can I file a claim if I can’t find the original policy document?

Yes. Insurers can process claims without the original policy as long as you can provide the policy number or enough identifying information to locate the account. If you can’t find any record of a policy, use the free NAIC Life Insurance Policy Locator to search participating carriers simultaneously.

What should I do if my term life claim is denied?

Request the denial in writing and review the stated reason carefully. File an internal appeal with the insurer first; many denials based on missing information are reversible at this stage. If the internal appeal fails, file a formal complaint with your state insurance department. State regulators have authority to compel the insurer to justify the denial and can overturn decisions where the denial was procedurally improper.

Sources

- NAIC, Consumer Insight: Retained Asset Accounts and Life Insurance

- NAIC, Consumer Insight: What to Know About Life Insurance Beneficiaries

- NAIC, Life Insurance Consumer Resource Page

- LIMRA, 2022 Insurance Barometer Study

- FDIC, Deposit Insurance Coverage Limits

- MIB Group, Request Your MIB Consumer File