Reviewed by the Smart Insurance 101 Editorial Team

Our Take

For most working adults with dependents, individual term life insurance should be your primary coverage, not group life through work. Employer plans are capped (typically 1-2x salary), disappear when you leave your job, and trigger IRS imputed income taxes on any employer-paid coverage above $50,000. The case for relying on group coverage alone is narrow: if you’re young, single, and early in your career, the free basic layer is fine for now. Once you have a mortgage, a spouse, or children, individual term is the foundation your family actually needs.

Here’s the question most people don’t ask until it’s too late: if you lost your job tomorrow, would your family still have life insurance? According to the U.S. Bureau of Labor Statistics’ 2025 Employee Benefits Survey, 62% of private industry workers have access to life insurance through their employer, but access and adequate coverage are two very different things. For most of those workers, the day their employment ends is the day their life insurance stops.

This article is for employees who want to understand the real tradeoffs in the term life vs group life insurance debate before a layoff, a health change, or a growing family forces the decision. Whether your employer’s plan is a useful free benefit or a dangerous false sense of security depends on a handful of specific factors, and we’ll walk through each one plainly.

Key Takeaways

- 62% of private industry workers have access to employer-provided life insurance, per BLS data from March 2025, but access doesn’t mean sufficient coverage.

- An estimated 118 million Americans held group life insurance in 2024, according to Forbes Advisor citing LIMRA research, making it the most common form of life insurance in the country.

- The IRS taxes employees on the value of employer-paid group coverage above $50,000 as imputed income, a cost most employees never see coming until it shows up on their W-2.

- Individual term premiums lock in for 10 to 30 years, while group voluntary rates typically reset every 5 years as you age into a higher rate band, often without notice.

- In my experience reviewing reader questions about coverage gaps, the single most overlooked risk is job loss during a health event, the moment you most need continuity of coverage is also when converting or buying new individual coverage is hardest.

What Exactly Is Group Life Insurance Through Work?

Group life insurance is employer-sponsored term coverage provided as a workplace benefit, and almost every plan follows the same basic structure. Your employer pays the premium for a base amount, usually one to two times your annual salary, and you’re enrolled without a medical exam. No blood draw, no questions about your health history. That’s the appeal.

Basic Coverage vs. Voluntary Supplemental Options

Beyond the free base layer, most employers offer voluntary supplemental group life, additional coverage you can buy through your employer’s group plan, often at group rates that seem competitive at first glance. Employees can typically purchase coverage up to a guaranteed issue limit (often $100,000 to $500,000 depending on the employer) without underwriting. Above that limit, they face simplified or full medical underwriting.

What makes all of it “term” insurance is the structure: there’s no cash value accumulation, no permanent policy building in the background. Coverage runs year to year and renews automatically with your employment. If you want a fuller grounding in how different life insurance structures compare, the Life Insurance 101 guide on this site covers the distinctions between term, whole, and universal policies clearly.

What I see in practice: Most employees assume their group coverage amount adjusts automatically as their salary grows. It often does for base coverage, but voluntary supplemental amounts are usually fixed unless you actively re-enroll. A reader making $120,000 who enrolled at $80,000 may still have their old supplemental amount sitting quietly on file.

How Individual Term Life Insurance Differs in Ways That Matter

The core difference between individual term and group coverage isn’t price, it’s ownership and permanence. An individual term policy belongs to you, follows you through every job change, and locks in a level premium for the entire policy term.

Portability and Rate Stability

When you buy a 20-year term policy at age 32, your premium is set on day one and doesn’t move for two decades. Group plans don’t work that way. Employer group rates are typically structured in age bands, your premium resets every five years, and the jump from your 40s to your 50s can be significant. By the time you’re 55, what looked like affordable group coverage may cost more per thousand dollars of coverage than an individual policy you could have locked in years earlier.

Individual policies also require medical underwriting, a full application, often a paramedical exam, and a review of your health history. That process sounds like a barrier, but it’s actually what earns you lower rates if you’re healthy. The group plan’s no-exam convenience is a tradeoff: healthy individuals subsidize the pool’s overall risk, and they never see the savings their health profile would have unlocked on the open market.

What You Can Customize

Individual term policies offer riders that are rarely available or meaningfully comparable in group plans. An accelerated death benefit rider, which lets you access a portion of the death benefit if diagnosed with a terminal illness, is standard on most individual policies but inconsistently available in group contracts. Child rider coverage, waiver of premium if disabled, and return-of-premium options give individual policyholders flexibility that group plans simply don’t match.

If you’re shopping individual options, the Best Term Life Insurance Companies for 2026 review on this site is a useful starting point for comparing carriers, underwriting reputation, and rider availability.

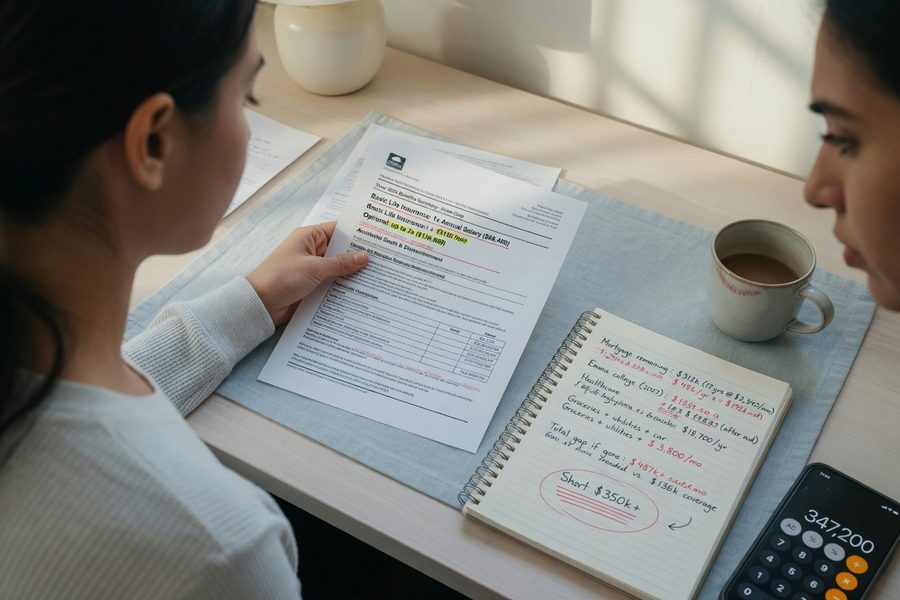

Is Your Work Coverage Actually Enough?

For most families, no. The standard employer plan provides one to two times annual salary, a $90,000 earner gets $90,000 to $180,000 in coverage. Standard financial planning guidance (including recommendations from organizations like the Insurance Information Institute) suggests 10 to 12 times income as a starting benchmark for a primary earner with a family. That’s a gap of roughly $700,000 to $900,000 for that same earner.

The coverage gap becomes a coverage cliff the moment you leave your employer. Group coverage typically ends on your last day of employment or within 30 days. You may have conversion rights, meaning you can convert the group policy to an individual permanent policy without a medical exam, but conversion policies are priced for people who can’t get coverage elsewhere. They are expensive, and the coverage type shifts from term to whole life, which most families don’t need. In practice, conversion is a last resort, not a plan.

The Hidden Costs of Depending Only on Group Coverage

Two costs catch employees off guard: imputed income taxes and voluntary rate band increases. Both are real, and neither gets explained clearly during open enrollment.

The IRS $50,000 Threshold

Under IRS Publication 15-B, the value of employer-paid group term life insurance above $50,000 of coverage is treated as taxable imputed income for the employee. The IRS calculates this value using a rate table based on your age, and the older you are, the higher the imputed income per $1,000 of excess coverage. A 48-year-old with $200,000 in employer-paid group coverage would owe income tax on the value of the $150,000 above the threshold. It shows up on your W-2 in Box 12, code C. Most employees see it and have no idea what it means.

Voluntary Rate Bands and the Real Comparison

Here’s where the math gets instructive. An employee buying $200,000 of supplemental group coverage at age 45 through their employer might pay around $30 to $40 per month in their current age band. By age 55, the same coverage in a group plan could exceed $60 to $80 per month, rates vary, but age-band jumps are a consistent feature of group contracts. A healthy 45-year-old buying a 20-year individual term policy for $250,000 could lock in rates in the $25 to $45 per month range through age 65, depending on health class.

Where this gets tricky: When I walk through this comparison with readers, the sticker shock usually comes when they see the age-55 group rate alongside what they could have locked in at 45. The five-year delay in buying individual term doesn’t just cost more in premiums, it also means buying at an older age with potentially worse health, which compounds the rate difference.

| Feature | Group Life (Employer) | Individual Term Life |

|---|---|---|

| Typical coverage amount | 1-2x annual salary (base); up to 3-5x with voluntary | Any amount; commonly $250,000-$2,000,000 |

| Portability | Ends at job termination (30-day grace typical) | Owned by you; follows you regardless of employment |

| Premium structure | Age-banded; resets every 5 years | Level for full term (10, 20, or 30 years) |

| Medical underwriting | None for basic; simplified for supplemental to limit | Full underwriting; rewards healthy applicants |

| IRS imputed income | Applies on employer-paid coverage above $50,000 | Not applicable (policyholder pays premiums) |

| Riders (e.g., accelerated death benefit) | Limited or unavailable | Widely available; customizable |

| Cost at age 45, $250,000 coverage (approx.) | $30-$40/mo (rises to $60-$80/mo by age 55) | $25-$45/mo locked in for 20 years |

When Group Life Is Genuinely Useful, and When to Layer on Top

Free basic group coverage is worth taking. There’s no rational argument for declining employer-paid life insurance, even if the amount is modest. The question is whether it’s sufficient, and for most people with dependents, it isn’t.

Group coverage works well as a starting point for employees who are young and single, whose employer covers the full premium for meaningful base coverage, or who have a health condition that makes individual underwriting difficult or expensive. In those cases, the no-exam group benefit is genuinely valuable, not just convenient.

The case against stacking up on voluntary supplemental group coverage is stronger. If you’re in good health and under 50, shopping the open market for additional individual term will frequently produce better long-term value than buying heavily into your employer’s voluntary plan. The group rate may look similar today, but it doesn’t stay similar.

What clients often miss: Layering individual term on top of your free group base, rather than replacing it, is almost always the right move. Keep the employer’s free coverage, buy individual term to close the income-replacement gap, and revisit the voluntary supplemental question only if your health limits individual options.

Given the current job market instability in 2026, this is also a practical risk moment. Layoffs in tech, media, and financial services have accelerated since 2023, and workers who relied entirely on group coverage have discovered the gap between their last day of work and their ability to secure affordable individual coverage, especially if they had a health event during that stretch. For self-employed workers or those considering a transition, the guide to health insurance for self-employed workers in 2026 covers related coverage continuity issues worth reading alongside this article.

Where This Recommendation Falls Short

The recommendation to prioritize individual term over group coverage assumes you can qualify for individual coverage at a reasonable rate. That assumption has real limits, and being honest about them is what separates a useful recommendation from a sales pitch.

The catch is health. If you’ve been diagnosed with a serious condition, Type 2 diabetes, a cardiac history, cancer in remission, or a mental health condition requiring certain medications, individual underwriting may classify you at a rated premium, push you into a higher risk class, or result in an outright decline. In those cases, your employer’s group plan, with its no-exam enrollment, may be the only life insurance you can realistically obtain at a workable cost. Relying solely on group coverage isn’t a mistake in this scenario; it’s the only practical option available.

The tradeoff for healthy people is a different kind: early in a career, when income is lower and dependents are fewer, the cost of an individual term premium may not fit comfortably into a budget. A 24-year-old with no dependents and $40,000 in student loans doesn’t necessarily need a 30-year term policy right now. Letting the employer’s free coverage serve as a placeholder for a few years isn’t reckless, it becomes reckless only when family obligations grow without a corresponding coverage review.

There’s also the question of voluntary supplemental group coverage purchased before a health change. If you enrolled in a large supplemental group amount when you were healthy and have since developed a condition that would affect individual underwriting, that group coverage becomes more valuable than the rates alone suggest. Dropping it to buy individual term might not be possible at comparable coverage amounts or rates. This is where a licensed insurance advisor adds real value, the general guidance here points in the right direction, but individual circumstances can flip the math.

Finally, where this falls short is in the specifics of each employer’s plan. Some large employers negotiate genuinely competitive voluntary rates that hold up well against the individual market for employees in their 30s. Some plans include portability provisions, not just conversion rights, that let employees maintain group term rates after leaving. Those cases are the exception, not the rule, but they exist and deserve a direct comparison before making a decision. Understanding how different types of insurance and their benefits stack up can help frame that evaluation.

How We Sourced This

This article draws on the U.S. Bureau of Labor Statistics’ 2025 National Compensation Survey (Employee Benefits in the United States, March 2025), Forbes Advisor’s 2024 life insurance statistics citing LIMRA industry data, and IRS Publication 15-B (updated annually) for imputed income rules. Rate range estimates for group voluntary and individual term premiums are based on publicly available insurer rate tables and aggregator data current as of early 2026; exact premiums vary by age, health class, and carrier. The IRS $50,000 threshold and imputed income calculation method are governed by IRC Section 79 and have not changed materially in recent years. This article was last verified in April 2026. Premium figures cited are illustrative approximations intended to show directional comparisons, not guaranteed quotes.

Frequently Asked Questions

Can I keep my group life insurance if I leave my job?

In most cases, your group life insurance ends within 30 days of your employment termination. You generally have the right to convert it to an individual permanent policy without a medical exam, but conversion policies are priced as a last resort, premiums are substantially higher than what a healthy person would pay on the open market, and the product shifts from term to whole life.

Is the free life insurance through work worth taking?

Yes, always. Employer-paid basic group life insurance costs you nothing and provides a real benefit, even if the coverage amount is modest. The issue isn’t whether to take it, it’s whether to treat it as your only coverage. For anyone with dependents, it almost never covers the full income-replacement need.

What does imputed income on life insurance mean?

When your employer pays for more than $50,000 of group term life insurance on your behalf, the IRS requires you to treat the cost of the excess coverage as taxable income. The value is calculated using an IRS rate table based on your age and appears on your W-2 in Box 12, code C. It’s a relatively small dollar amount for most employees, but it’s often a surprise the first time someone sees it.

How much life insurance do I actually need?

A common starting benchmark is 10 to 12 times your annual income, with adjustments for mortgage balances, number of dependents, spouse’s income, and outstanding debts. A $90,000 earner with a family and a mortgage likely needs $900,000 to $1,000,000 or more in total coverage, far beyond what any typical employer group plan provides on its own.

Are voluntary group life rates through work competitive with individual term rates?

At younger ages, group voluntary rates can look competitive in the short term. The problem is that group rates increase every five years as you age, while individual term premiums stay flat for the full policy term. A healthy person in their 30s or 40s who locks in an individual 20-year term policy will typically pay less in total over that period than someone staying in an age-banded group plan, and they’ll own a portable policy throughout.

What happens to my life insurance if I get laid off?

Your group coverage ends, usually within 30 days. If you’re healthy, applying for individual term insurance immediately after a layoff is the right move, your health status today determines your rates. If you wait and a health issue develops during a period of unemployment, securing affordable individual coverage later becomes significantly harder. This is the core reason financial planners recommend not relying exclusively on employer group coverage.

Should I buy supplemental life insurance through work or shop independently?

If you’re in good health and under 50, shopping independently for an individual term policy will usually produce better long-term value than stacking up voluntary supplemental group coverage. Individual term locks in your rate; voluntary group resets every five years. The exception is if your health would result in a rated or declined individual application, in that case, the group plan’s no-exam access may be worth prioritizing. Comparing top individual term carriers before committing to voluntary supplemental enrollment is time well spent.

Sources

- U.S. Bureau of Labor Statistics, Employee Benefits in the United States, March 2025

- Forbes Advisor, Life Insurance Statistics 2024 (citing LIMRA)

- IRS, Publication 15-B: Employer’s Tax Guide to Fringe Benefits (Group Term Life Insurance)

- Insurance Information Institute, How Much Life Insurance Do I Need?

- National Association of Insurance Commissioners, Life Insurance Buyer’s Guide